Personal Wealth Management / Economics

The Overlooked Lesson From November Retail Sales

What we think retail sales reveal about potential future lockdowns’ impact.

In one of the UK’s last major economic data releases of the year, retail sales grew for a second straight month in November, rising 1.4% m/m.[i] Whilst some financial publications we follow touched on the report’s positive takeaways, we also saw some experts warn the good cheer may be short-lived due to the Omicron variant and the government’s latest containment measures. Those warnings gained momentum this week after the Confederation of British Industry’s (CBI) latest survey suggested December retail sales growth slowed.[ii] Whilst it is possible the government’s response to Omicron chills retail activity in the near term, we think investors benefit from keeping retail sales’ longer-term trend in mind—especially as speculation swirls about renewed COVID restrictions and a potential return to lockdown.

November retail sales volumes, which strip out the impact of price changes, grew amongst most categories.[iii] Though food stores sales volumes dipped mildly (-0.2% m/m), non-food stores sales (2.0% m/m) and automotive fuel sales (3.7% m/m) rose.[iv] According to the Office for National Statistics (ONS), many retailers attributed strong activity to Black Friday, the day after America’s Thanksgiving holiday when retailers traditionally offer big discounts, and holiday shopping in general.[v] This year’s November reporting period included Black Friday but not Cyber Monday (another day of discounted retail, particularly for personal electronics), though the ONS has accounted for this particular holiday-spending skew in its seasonal adjustment calculation since 2013.[vi] Whilst some coverage we follow focused on a few positive, November-specific tidbits—e.g., clothing stores sales passed their pre-pandemic levels for the first time—we think the more interesting takeaway is UK retail sales’ broad-based improvement since the start of the pandemic, despite early-2020’s deep economic contraction and multiple lockdowns.[vii] In our view, it is confirmation of what stocks were looking ahead to as they recovered from last year’s bear market (typically a long, deep decline of -20% or worse with a fundamental cause).[viii]

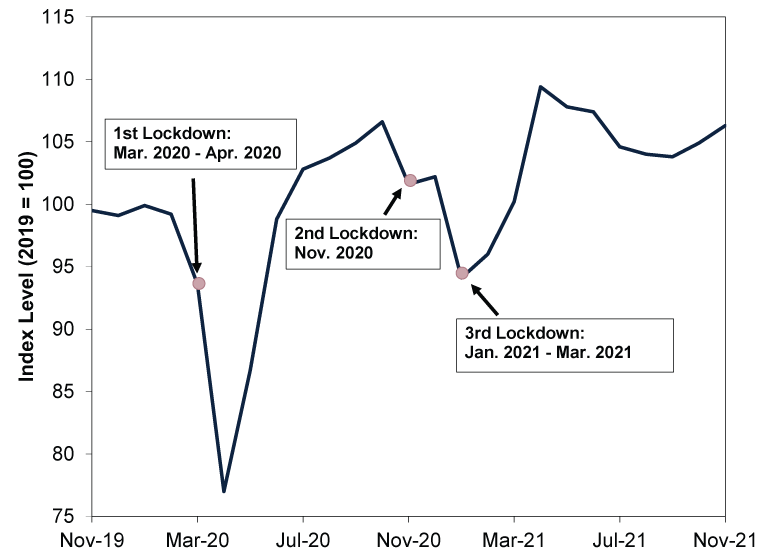

Consider: Prime Minister Boris Johnson announced the first lockdown on 23 March 2020. Correspondingly, retail sales fell -5.6% m/m in March and plunged -17.7% m/m in April (and -22.4% cumulatively from February – April).[ix] Once the government started easing lockdown measures about seven weeks later, retail sales also began recovering, rising 12.6% m/m in May and 14.0% m/m in June.[x] Taking a longer view, despite restrictions and partial lockdowns’ returning in late-2020 and lingering into the spring and summer, November retail sales volumes were 7.2% higher than February 2020, the last month of pre-pandemic data.[xi] Moreover, sales volumes at food stores and non-food stores are up 3.2% and 6.7%, respectively, over that same timeframe whilst fuel sales volumes are just -1.9% off pre-COVID levels.[xii]

Now, retail sales aren’t all-telling economic indicators, in our view, and they don’t even reflect all consumer spending. But we think their post-lockdown recovery provides a sense of what forward-looking stocks were anticipating in late March 2020. The global bear market began 20 February and ended 16 March, a week before Johnson announced the UK’s lockdown, which was the last amongst major developed nations.[xiii] In our view, stocks’ record-fast descent reflected their pricing in the damage from the global economy’s sudden shutdown.[xiv] But after digesting that fallout, we think stocks moved on and began pricing in the expected recovery as they looked ahead to reopenings and consumers and businesses adapted to a pandemic economic environment.[xv] Interestingly, stocks began recovering before official data confirmed the economic recovery was underway.[xvi] The UK reported May 2020 retail sales rose 12.0% m/m on 19 June 2020, the first positive reading after March and April’s monthly declines.[xvii] At that point, both global stocks (29.5%) and UK stocks (22.3%) were more than three months into a new bull market (a long period of generally rising stock prices).[xviii]

Considering the recent surge in Omicron cases and the UK government’s implementation of its Plan B COVID rules, we have seen analysts speculate lockdowns could return—again. That is a possibility, but despite all the speculation and leaks hinting at their return, lockdowns are political decisions that defy prediction, in our view. Johnson’s cabinet reportedly revolted against new restrictions this week.[xix] Maybe that holds, maybe it doesn’t. Yet whilst we don’t dismiss the economic damage associated with a new lockdown, the experience isn’t new to the UK. England entered a four-week lockdown in November 2020 and another this past January. On both occasions, retail sales fell, but they weren’t permanent setbacks—once restrictions eased, growth returned. (Exhibit 1) Crucially, we think UK stocks looked through it all, rising 18.2% from 30 September 2020 – 31 March 2021 despite a brief October pullback.[xx]

Exhibit 1: Lockdowns Didn’t Permanently Set Back Retail Sales

Source: ONS, as of 20/12/2021. UK retail sales volumes, November 2019 – November 2021.

Now, UK retail sales won’t necessarily follow this exact pattern if lockdowns return, but we think society and markets have seen this movie before—worth keeping in mind amidst warnings of slowing sales in December and January. Restrictions could cause retail sales to slow or contract—perhaps even sharply. But at this point, we don’t think a few renewed lockdowns will automatically wallop the global economy or stocks again, as they likely lack the scope and surprise power they packed in February and March last year, when the entire developed world shut down without notice or precedent. In our view, stocks likely recognise economic growth can snap back quickly once restrictions ease and that a handful of high-profile lockdowns aren’t the same as the global economy suddenly coming to a stop. That doesn’t preclude short-term negativity in stock markets, which our research shows can arrive for any or no reason at any time, but it does suggest to us that a repeat of early 2020 is highly unlikely right now.

[i] Source: Office for National Statistics (ONS), as of 17/12/2021.

[ii] “Retail Sales Slow After UK’s Covid Plan B Measures Announced,” Larry Elliott, The Guardian, 21/12/2021.

[iii] See note i.

[iv] Ibid.

[v] “Retail Sales, Great Britain: November 2021,” Staff, ONS, 17/12/2021.

[vi] Ibid.

[vii] Ibid.

[viii] Source: FactSet, as of 22/12/2021. MSCI World Index return with net dividends in GBP, 20/2/2020 – 31/12/2020.

[ix] See note i.

[x] Ibid.

[xi] See note v.

[xii] Ibid.

[xiii] FactSet, as of 22/12/2021. MSCI World Index return with net dividends in GBP, 20/2/2020 – 16/3/2020.

[xiv] Ibid. MSCI World Index return with net dividends in GBP, 20/2/2020 – 16/3/2020

[xv] Ibid. MSCI World Index return with net dividends in GBP, 20/2/2020 – 31/12/2020.

[xvi] Ibid. MSCI World Index return with net dividends in GBP, 16/3/2020 – 19/6/2020.

[xvii] Source: ONS, as of 19/6/2020.

[xviii] Source: FactSet, as of 22/12/2021. MSCI World Index return and MSCI United Kingdom Investable Market Index return with gross dividends in GBP, 16/3/2020 – 19/6/2020.

[xix] “Boris Johnson ‘Facing Cabinet Revolt’ Over Covid Restrictions,” Emily Atkinson, The Independent, 12/12/2021. Accessed via MSN.

[xx] Ibid. MSCI United Kingdom Investable Market Index return with gross dividends, 30/9/2020 – 31/3/2021. Brief October pullback refers to stocks’ -7.0% decline from 9/10/2020 – 30/9/2020.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-18

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-18

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today