Personal Wealth Management / Market Analysis

What to Make of Falling Home Prices

Housing prices have been falling in major economies—what does it mean for investors?

Housing markets in several major economies have had a rough year as financial headlines we monitor recounted, and some have speculated about potential spillover effects to other parts of the economy. However, we don’t think falling home prices necessarily spell trouble for the global economy or stocks. Let us run through a global look at the data—and explain why we don’t see this as a big concern from a macroeconomic point of view.

Starting in the US, existing home sales fell -0.7% m/m in January—their 12th straight monthly contraction—to an annualised pace of 4 million, the weakest since October 2010.[i] Homes have also been sitting on the market for longer—33 days on average in January 2023 compared to 19 days a year earlier.[ii] This comes despite inventory that, whilst up 15.3% y/y in January, was still historically low at 980,000 homes for sale.[iii] Price rises have slowed on a year-over-year basis, and they are likely falling as of late, too, with the comparison to prices 12 months ago obscuring more recent declines.[iv]

The trend is similar in other developed nations. In the UK, house sales fell -3.0% m/m in January, the worst start to a year since 2015.[v] Homes there are also spending more time on the market, with one in seven going six months before being sold, the highest proportion since February 2015.[vi] Canadian January home sales slipped -3.0% m/m, and prices were down an 11th straight month, according to the Canadian Real Estate Association.[vii] In Australia, new home sales fell by -4.6% m/m in December, and property data firm CoreLogic found that, in volume terms, unit sales rose in just 2 of 25 regional markets in the 12 months to last November.[viii] On the Continent, Sweden has been one of the hardest-hit housing markets globally, and we have seen economists argue the tough times will continue.[ix]

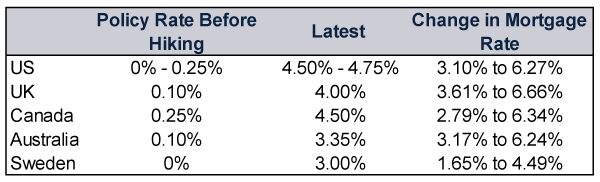

Based on our research, real estate is very economically sensitive to interest rate changes, so as monetary policy officials have hiked rates over the past year, mortgage rates have climbed, too. (Exhibit 1) In our view, borrowing becoming more expensive has cooled demand, and prices have fallen correspondingly.

Exhibit 1: Monetary Policy Institution Hikes, Rising Mortgage Rates

Source: FactSet, US Federal Reserve (Fed), Bank of England, Bank of Canada, Reserve Bank of Australia and the Riksbank, as of 23/2/2023. The Bank of England began raising its policy rate in December 2021; the Fed and Bank of Canada in March 2022; and the Reserve Bank of Australia and Riksbank in May 2022. Mortgage rates are end of month and refer to the 30-year fixed rate mortgage (US); weighted average interest rate, standard variable mortgage (UK); 1-year conventional mortgage rate (Canada); 3-year fixed housing loan (Australia); and 5-year mortgage rate (Sweden), December 2021 – January 2023.

Whilst we think rising interest rates have contributed to real estate’s struggles, our research indicates domestic issues have a large impact on the housing market, too, which is worthwhile to keep in mind when considering housing’s supply and demand drivers. For example, the pandemic drove housing booms in certain regions: See New South Wales and Queensland in Australia, as some left cities for a lifestyle change (similar to what happened in Cornwall).[x] But as COVID restrictions relaxed and life returned to pre-pandemic norms, we have observed housing demand in these areas has tapered off—as have prices.

Longer-running, local nuances have also played a role in dampening prices. For example, according to our research, there is a higher prevalence of variable-rate loans (in which the interest rate charged on an outstanding balance changes as market rates change) in Sweden, Canada and the UK. That leaves households more vulnerable to interest-rate changes, and higher rates can weigh on demand. In Sweden in particular, rising rates mean higher payments for many households since most mortgage rates are fixed for two years or less—and around 40% reset in three months or less.[xi] In the UK, buy-to-let investors have faced higher taxes and new regulatory burdens as well as higher mortgage costs, prompting many to sell—contributing to higher housing supply and pushing prices down.[xii]

That said, for all the weakness in the data—and though residential real estate gets a lot of attention—its contribution to broader economic output in developed nations isn’t huge, according to our analysis. Consider construction (which housing is but a part of). On a gross value added basis, construction comprises just 4.1% of US total output and 6.0% in the UK.[xiii] So despite recent data weakness—e.g., the UK’s construction purchasing managers’ index (PMI) registered 48.4 in January, indicating contraction—the broader economic effect is likely limited.[xiv] Another way to see this: In the US, residential investment contracted at double-digit annualised clips over the past three quarters: -17.8%, -27.1% and -25.9%, respectively.[xv] Q4’s plunge detracted -1.24 percentage points from headline gross domestic product (GDP).[xvi] Yet US GDP has grown over that stretch, including last quarter’s 2.7% annualised growth.[xvii]

In our view, the housing market isn’t a swing factor in developed, services-dominant economies, so its struggles aren’t likely to derail growth. From a stock market perspective, the real estate sector, comprised mostly of real estate investment trusts (REITs), doesn’t have a huge footprint, either: just 2.7% of the MSCI World.[xviii] We don’t dismiss those impacted by housing’s recent soft patch. But when considering the economic factors that matter most to global markets, we suggest keeping residential real estate’s impact in perspective—especially since regional and local developments play an outsized role on supply and demand, in our opinion.

[i] “US Sales of Previously Owned Homes Decline for a 12th Month,” Reade Pickert, Bloomberg, 21/2/2023. Accessed via Yahoo! News. An annualised rate refers to the rate home sales would rise over an entire year if the monthly growth rate persisted all 12 months of the year.

[ii] Ibid.

[iii] Ibid and “Home Sales Sank in January for the 12th Straight Month,” Anna Bahney, CNN, 21/2/2023.

[iv] The base effect is a mathematical phenomenon in which a lower denominator can result in a larger quotient (and vice versa).

[v] “Half the Homes on the Market Are Taking Months to Sell,” Alexa Phillips, The Telegraph, 21/2/2023. Accessed via MSN.

[vi] Ibid.

[vii] “Home Price Drop Hits 15% in Canada as Rates Squeeze Buyers,” Ari Alstedter, Bloomberg, 15/2/2023. Accessed via Yahoo! Finance.

[viii] “Soaring Property Prices in Australia’s Most Sought-After Regional Areas Come Tumbling Down,” Peter Hannam, The Guardian, 14/2/2023.

[ix] “Sweden Is Facing its ‘Day of Reckoning’ as House Prices Plummet,” Hannah Ward-Glenton, CNBC, 11/1/2023.

[x] See note vii and “UK Enjoys Property Sales Boom Amid Covid-19 Pandemic,” Phillip Inman, The Guardian, 9/3/2021.

[xi] “What’s Causing the Swedish Housing Market Plunge,” Niclas Rolander, Bloomberg, 4/1/2023. Accessed via Money Lowdown.

[xii] “‘Lots of Us Are Very Anxious’: Why Britain’s Buy-to-Let Landlords Are Selling,” Sarah Marsh, The Guardian, 24/1/2023.

[xiii] Source: The Bureau of Economic Analysis and Office for National Statistics, as of 22/2/2023. Gross value added (GVA) is a government-produced metric of economic output.

[xiv] Source: S&P Global, as of 23/2/2023. A PMI is a monthly business survey that tracks general economic conditions. Readings above 50 imply expansion whilst below 50 suggest contraction.

[xv] Source: BEA, as of 23/2/2023

[xvi] Ibid. GDP is a government-produced metric of economic output.

[xvii] Ibid.

[xviii] Source: FactSet, as of 21/2/2023. Real estate investment trusts (REITs) are investment vehicles through which individuals can invest in the property market without having to directly buy and manage a physical property.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

-

Market Analysis February’s Growthy Data—and the Iran War’s Souring Sentiment2026-03-06

-

Market Analysis Putting the Latest Private Credit Implosion in Perspective2026-03-06

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today