Personal Wealth Management / Market Analysis

What to Make of This Big Table of Currency Swings, Stocks and Inflation

Currencies’ relationship with stocks and inflation isn’t what financial commentators make it out to be.

Amongst the many alleged negatives that financial news we cover attributes recent volatility to, one has seemingly gained primacy of late globally: the strong dollar.[i] Some experts warn it is a negative for the US itself. As the dollar appreciates against overseas currencies, commentators suggest it hits US-based multinationals’ overseas revenues once they are converted back to dollars (never mind that as other currencies decrease in value compared to the dollar, any parts and labour American multinationals source in those currencies become relatively less expensive, and most international earnings don’t get repatriated and converted to dollars). Other observers focus on non-US stocks, warning their weaker currencies are a headwind. Commentators suggest, for example, as the pound depreciates against the dollar it is causing the UK to import even faster inflation (broadly rising prices across the economy) because imported goods will cost more. Add in actual currency market intervention in Japan plus talk of the same in South Korea and China, and currency chaos seems to be top of investors’ minds.[ii] In our view, this is more a sign of sentiment than an actual negative for stocks, as we will show.

If you re-read the prior paragraph carefully, you may notice a weird inconsistency: financial commentators’ warnings about the US directly contradict their warnings about the UK, Europe and Asia. If the strong dollar is supposedly bad for the US, then that implies a weaker dollar would be better for UK and others. Yet we are also told a weaker currency is a massive headwind in the UK, Europe and Asia, implying they would benefit from the stronger currency that is supposedly a massive risk for the US. Absent some mythically perfect exchange rate, which we have never seen theorised ever, we see no way to make it make sense.

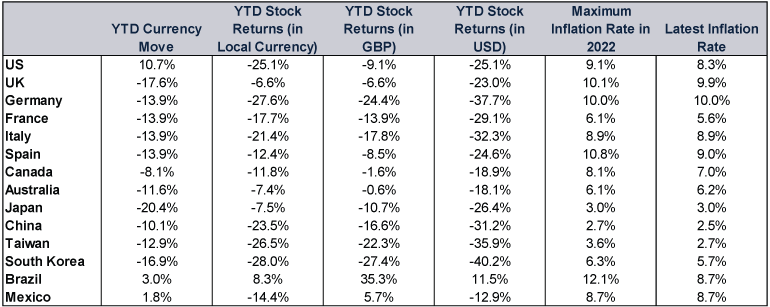

If theoretical arguments aren’t your thing, then consider Exhibit 1. It shows a smattering of major developed and Emerging Markets’ currency moves year to date, along with their year-to-date stock returns in their home currencies, US dollars and British pounds, their highest inflation rate in 2022 thus far and their most recent inflation reading. As you will see, there isn’t much data to support today’s prevailing currency-swing warnings from commentators we follow. The US, which has the largest currency appreciation, is in a bear market (typically defined as a prolonged downturn due to fundamental causes) in dollars. Brazil, which has the second-best currency of this bunch, has positive year-to-date returns in its home currency. Yet Mexico, whose currency is also up this year, is down double digits in pesos. As for the eurozone’s four largest economies, Germany is down over twice as much as Spain in euros, and the corresponding inflation rates are all over the map. The UK has the second-weakest currency but its stocks are down just single-digits in pounds, albeit with double-digit inflation. Yet Japan, where the yen is down more than -20% on the dollar, has the second-lowest inflation rate.

Exhibit 1: A World of Currency Moves, Stock Returns and Inflation

Source: FactSet, as of 4/10/2022.[iii]

About the only consistency here is the mathematical one: In nations whose currencies have strengthened against the dollar, returns denominated in dollars are a tad higher than in their local currencies, whilst the opposite is true for nations whose currencies have weakened relative to the greenback—which is why returns in GBP are significantly higher across the board. This is the silver lining of currency math for UK investors: If you are a British investor investing in US companies, you get the company’s return in dollars plus the dollar’s appreciation relative to the pound. So, when the pound weakens, the US company’s return will always be higher in pounds. But currency moves are cyclical, and the dollar won’t strengthen this way forever. Eventually, due to changes in interest rates and investor sentiment, it will cool or weaken, at which point currencies like the pound or euro will likely increase in value and international investors’ returns on US stocks will be weaker than returns in dollars. We point this out mostly to prepare you for a time when a stronger pound makes international investing look less attractive—over time, we think all of these moves even out, making reacting to them an error.

As for the supposed linkages between currencies and returns or currencies and inflation? We don’t think they pass the test. If there was a strong relationship on either front, it would be a powerful forecasting tool, everyone would use it, and there would be no need for this article. In our view, maxims like this are simply right just often enough to maintain their reputation but nowhere near often enough to be worth much in trying to figure out where stocks will go looking forward. Said another way, our historical research of currency swings and market activity shows sometimes currencies and returns move in the same direction, and sometimes they don’t. According to our observations of market history, sometimes currency weakness comes with bad inflation, and sometimes other factors can offset the pressure on import prices. In our experience, every situation is different and depends on the variables at hand.

In our view, it can be helpful to keep an eye on potential currency market interventions if you are wary of their potential unintended consequences and general record of creating winners and losers. But we don’t think presuming strong or weak currencies are inherently terrible or wonderful for stocks will work out well repeatedly.

[i] Source: FactSet, as of 6/10/2022. Statement based on MSCI World Index return with net dividends, in GBP, 3/10/2022 – 4/10/2022.

[ii] “Japan Spent Record of Nearly US$20b on Intervention to Support the Yen,” Staff, Reuters, 30/9/2022. Accessed through The Business Times. “Factbox – What South Korea Has Done and Could do to Defend Won,” Staff, Reuters, 30/9/2022. Accessed through U.S. News. “China digs Deep Into Bag of Yuan Tricks to Resist Dollar Steamroller,” Staff, Reuters, 3/10/2022. Accessed through Yahoo! Finance.

[iii] Data cited are the nominal trade-weighted US dollar index (broad currency basket) and the spot exchange rates of the US dollar per British pound, euro, Canadian dollar, Australian dollar, Japanese yen, Chinese yuan, Taiwanese dollar, South Korean won, Brazilian real and Mexican peso, 31/12/2021 – 30/9/2022. MSCI USA, Germany, France, Italy, Spain, Canada, Australia, Japan, China, Taiwan, South Korea, Brazil and Mexico index returns with net dividends and MSCI UK IMI index total return in the aforementioned local currencies, GBP and USD, 31/12/2021 – 30/9/2022. Headline year-over-year consumer price inflation rates for the US (June and August), UK (July and August), Germany (September), France (July and September), Italy (September), Spain (July and September), Canada (June and August), Australia (Q2), Japan (August), China (July and August), Taiwan (June and August), South Korea (July and August), Brazil (April and August) and Mexico (August).

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-18

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-18

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today