Personal Wealth Management / Market Analysis

About That Vaccine-Driven Value Rally…

Things haven’t exactly gone as those who championed value-orientated stocks projected.

Editors’ Note: MarketMinder Europe does not make individual security recommendations. The below merely represent a broader theme we wish to highlight.

One year ago Tuesday, Pfizer and BioNTech announced that their COVID vaccine candidate had shown promising results in advanced American clinical trials, and commentators who had long championed value-orientated stocks got a proverbial shot in the arm. Our research shows value stocks normally lead early in a bull market (a long period of generally rising equity prices), but growth-orientated shares had led since stocks bottomed the prior March.[i] The vaccine announcement led many commentators we follow to argue they weren’t wrong when they argued value would lead, just early. According to their logic, value had lagged because lingering lockdowns were disproportionately harming these firms, they claimed, and vaccinations would get the party started for real. A year later, that hasn’t exactly worked out as they anticipated, as we will show.

To set the stage, growth-orientated stocks generally have higher valuation metrics like price-to-earnings ratios and focus on re-investing profits into the core business to expand over time, making their profits relatively less sensitive to economic ups and downs. Their earnings often come more from long-term technological trends than near-term economic conditions. Value-orientated shares, by contrast, tend to carry relatively lower price-to-earnings ratios and more debt, making them more sensitive to economic conditions, and they tend to return more money to shareholders via dividends and share buybacks and invest less in growth-orientated endeavours. Their economic sensitivity is at the root of forecasts for them to lead once vaccines rolled out.

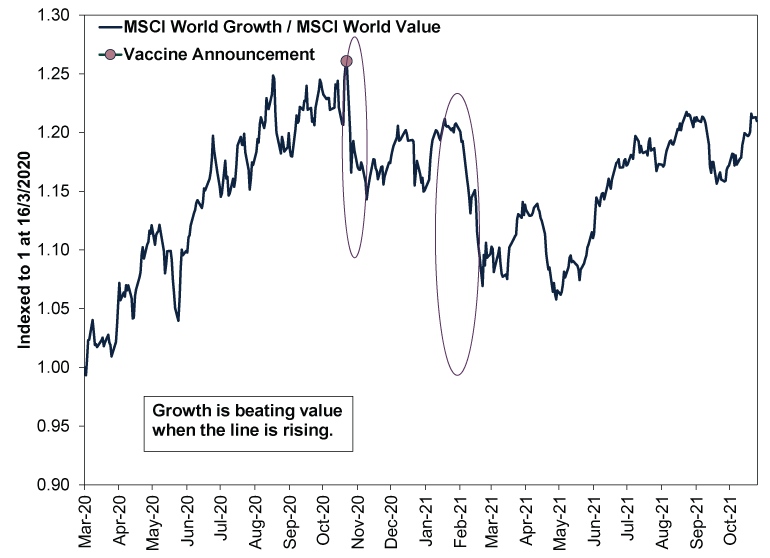

Value has led cumulatively since Pfizer’s momentous press release, as Exhibit 1 shows. But as the chart also demonstrates, the margin is small. Moreover, value’s leadership occurred in two short bursts: one last November, and one this January and February. Since value’s returns relative to growth peaked on 13 May, growth is up 24.5%.[ii] Value? Just 8.8%.[iii] Moreover, since the bull market began on 16 March 2020, growth is beating value by a whopping 33.4 percentage points—92.3% to 58.9%.[iv]

Exhibit 1: So Much for the Vaccine Value Boom

Source: FactSet, as of 10/11/2021. MSCI World Growth and Value Index returns with net dividends, 16/3/2020 – 9/11/2021. Indexed to 1 at 16/3/2020.

In our view, value’s twin runs were sentiment-fuelled—enthusiasm first over the vaccines’ existence, then their rollout. We think stocks priced those events very quickly and then moved on, as we have found to be typical of very widely discussed developments. Our research shows markets move most on surprises, and the prospect of vaccines enabling broader reopening was baked in lightning-fast, leaving a dearth of fundamental support for value leadership.

That remains the case today, in our view. Value stocks generally have lower gross profit margins, and our research shows they tend to rely on cost-cutting and catch-up growth in an economic recovery to boost earnings. (Gross profit margins, calculated by subtracting cost of goods sold from sales and dividing the result by cost of goods sold, are a quick measure of a company’s profitability before adjusting for taxes, interest on debt and other accounting items, which can cause considerable temporary skew.) The US’s economic recovery from lockdowns is complete (it is now in expansion, having surpassed the pre-downturn peak in gross domestic product, which is a government-produced estimate of economic output), and we already see indications in the data growth is returning to its pre-pandemic slow trend.[v] The UK and eurozone are also closing in on pre-pandemic levels of economic output.[vi] We think this works against value stocks. Value-orientated companies also tend to rely on bank lending or bond issuance to fund growth, making it hard to finance expansion when the spread between short-term and long-term interest rates is slim and thus pinches banks’ net interest margins (their profit margin on new loans), which is the case now.[vii]

In our view, growth stocks are much better positioned in this environment. As our recent commentary showed, they tend to have much fatter gross margins, giving them much more cash flow to plow back into the core business. They also have a big cushion to weather rising cost pressures and strong pricing power, thanks to their strong brand names, globally dominant business lines and ties to long-term technological trends. We think this puts them in the catbird seat relative to value in this time of rising shipping, labour and input costs.

Growth’s leadership probably also means we are later in this bull market than most analysts we follow presume, as growth normally leads in a bull market’s later stages.[viii] That doesn’t mean the end is anywhere close to imminent, as we see plenty of bricks left in the proverbial wall of worry bull markets are often said to climb. But it does suggest to us that value’s real time to shine probably won’t arrive until after the next bear market (normally a deep, prolonged broad marked decline of -20% or worse with an identifiable fundamental cause). In the meantime, because value stocks are so economically sensitive, we think maintaining a big overweight to them probably isn’t the most beneficial approach.

[i] Source: FactSet, as of 10/11/2021. Statement based on MSCI World Growth and MSCI World Value Index returns with net dividends.

[ii] Source: FactSet, as of 10/11/2021. MSCI World Growth Index return in GBP with net dividends, 13/5/2021 – 9/11/2021.

[iii] Ibid. MSCI World Value Index return in GBP with net dividends, 13/5/2021 –9/11/2021.

[iv] Ibid. MSCI World Growth and Value Index returns in GBP with net dividends, 16/3/2020 – 9/11/2021.

[v] Ibid. Statement based on US gross domestic product (GDP).

[vi] Ibid. Statement based on GDP in the UK and eurozone.

[vii] Ibid. Statement based on 10-year and 3-month benchmark interest rates in the US, UK, Japan, Germany, France, Spain and Italy.

[viii] See Note i.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Volatility What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-31

-

Politics This Week in Gridlock: Europe Edition2026-03-27

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today