Personal Wealth Management / Market Analysis

More Signs Recession Isn’t Certain

April’s flash PMIs run counter to the recession narrative.

Q1 gross domestic product (GDP, a government-produced measure of economic output) results for major economies have started trickling out: Eurozone GDP rose 0.1% q/q, and the currency bloc’s four-largest economies didn’t report contraction in Q1.[i] Financial publications we follow noted the Continent has thus far managed to avoid recession (a period of contracting economic output), and some more recent indicators suggest growth continued in April: Namely, S&P Global’s flash purchasing managers’ indexes (PMIs), which hit the wires last Friday. They add further evidence this year’s economic reality is better than projected—the central force behind global stocks’ rally since last June’s low, in our view.[ii]

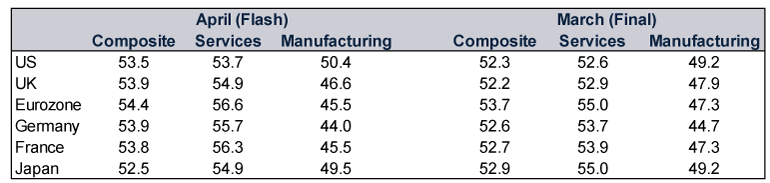

April’s flash PMIs for major developed economies showed overall growth in April, though they were mixed on a sector basis. PMIs are monthly business surveys where readings above 50 imply expansion whilst below 50 imply contraction. Whilst services all topped 50 this month, manufacturing was mostly under that mark. (Exhibit 1) These are just surveys, and they measure growth’s breadth rather than its magnitude, but they are consistent with recent trends.

Exhibit 1: A Look at the Latest PMIs

Source: FactSet and S&P Global, as of 26/4/2023.

Local developments weighed on activity in some countries—for example, French manufacturers reported strikes protesting the government’s pension reforms hurt demand.[iii] But that split between services and manufacturing is consistent with other indicators we have reviewed, and the positive composite reading (which aggregates services and manufacturing) matches French statistics agency Insee’s assessment of the situation in its February outlook.[iv] Then, when commenting on the potential negative impact in some areas, Insee wrote, “previous episodes show that while this impact can be significant at the sectoral level (whether in sectors directly affected by the strikes or those that are partly dependent on them), it is usually quite limited at the macroeconomic level, especially as we then see catch-up effects.”[v] Plus, as the agency noted, increased remote work could further cushion the blow.[vi]

Yet the manufacturing landscape wasn’t all gloom. Factories broadly reported improvement in supply-chain constraints and costs (e.g., commodity prices) as they worked through pandemic-driven backlogs.[vii] Moreover, services—which comprise the lion’s share of GDP in developed nations—have fared better than manufacturing.[viii] Services new orders expanded, signaling growth is likely in the near future since today’s orders are tomorrow’s production.[ix]

April PMIs also imply 2023’s economic reality hasn’t been dire as previously forecast based on our review of financial headlines. Take the UK and Germany, where we have seen many economists argue recession is inevitable, due largely to those economies’ exposure to natural gas prices, which soared last year.[x] As we pointed out recently, UK GDP hasn’t been great, but it also hasn’t plummeted, and we don’t think a downturn is a given. German GDP was flat in Q1, with underlying details set to be released near May’s end. Whilst Germany has thus far avoided two consecutive quarterly contractions—fulfilling one common definition of recession—that outcome occurring is a far cry from forecasts that circulated last summer. Then, we read projections of a big downturn in Europe’s largest economy beginning in the winter.[xi] Even late last year, many economic commentators we follow warned German activity would crater and the eurozone would fall with it. Though the country’s industrial sector has struggled, services have held up, as PMIs demonstrate. In our view, data globally have been mixed but aren’t cratering—pouring cold water on the notion recession is certain.

Despite evidence the biggest developed economies are holding up better than many anticipated, the financial coverage we have seen suggests sentiment remains dour—e.g., yeah, services PMIs are faring well, but growth is now lopsided. In our view, dour interpretations of positive data are a classic sign the pessimism of disbelief is alive and well. Take a popular reaction to the flash services PMIs we have observed: Yeah, economic activity is more resilient than thought, but that may reignite inflationary pressures, forcing monetary policy institutions to hike interest rates for longer than anticipated—an alleged negative for the economy.

But at this point, we think rate hikes have seemingly lost their shock factor—as our analysis of market data shows. Since the US Federal Reserve first hiked rates by 25 basis points on 16 March 2022, American stocks are down -1.8%.[xii] But since the Fed launched some larger hikes of 75 basis points from June through November—and continued to hike through March this year—US stocks have risen 9.8%.[xiii] It is a similar story in the UK and eurozone. Since the Bank of England became the first major monetary policy institution to lift its benchmark rate in December 2021, UK stocks are up 16.2%.[xiv] Ditto for the Continent: After the ECB joined the rate hike party in mid-July last year, German and French stocks have climbed 22.1% and 24.4%, respectively—in line with broader eurozone markets (21.5%).[xv] In our view, this is a reminder that stocks don’t have pre-set reactions to monetary policymakers’ moves.

Now, since PMIs don’t measure growth’s magnitude, output measures (e.g., GDP, industrial production, consumer spending) could contract even as PMIs imply economic activity broadened. But those messages aren’t in conflict, in our view. Rather, we think they are a reminder of the importance of understanding what different economic measures show and don’t show. Our review of the latest data suggest economies are muddling along—and when compared to expectations of recession, even tepid growth can exceed expectations, a hallmark characteristic of a new bull market (a period of generally rising equity prices).

[i] Source: FactSet and the World Bank, as of 28/7/2023. Statement based on 2021 German GDP, 2021 French GDP, 2021 Italian GDP and 2021 Spanish GDP (in constant 2015 USD).

[ii] Source: FactSet, as of 27/4/2023. MSCI World Index returns with net dividends in GBP, 16/6/2022 – 26/4/2023.

[iii] Source: S&P Global, as of 21/4/2023.

[iv] “Economic Outlook, 7 February 2023,” Insee, 2/10/2023

[v] Ibid.

[vi] Ibid.

[vii] See note ii.

[viii] Source: S&P Global and World Bank, as of 27/4/2023. Statement based on services as a percentage of GDP (as of 2021) for the UK, Germany, France, eurozone, and the US.

[ix] See note ii.

[x] “Triple Whammy for European Gas Supplies Sends Prices Soaring,” Anna Cooban, CNN, 16/6/2022.

[xi] Source: The World Bank, as of 27/4/2023. Statement based on 2021 German GDP (in constant 2015 USD).

[xii] Source: FactSet, as of 27/4/2023. MSCI USA Index returns with net dividends, in GBP, 16/3/2022 – 26/4/2023.

[xiii] Ibid. MSCI USA Index returns with net dividends, in GBP, 16/6/2022 – 264/4/2023.

[xiv] Ibid. MSCI United Kingdom Index returns with net dividends, 16/12/2021 – 26/44/2023.

[xv] Ibid. MSCI EMU Index, MSCI Germany Index and MSCI France Index returns with net dividends, in GBP, 21/7/2022 – 26/4/2023.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights The Danger of Chasing Investor Flows2026-08-05

-

Market Analysis A Market-Orientated Perspective on the EU’s Low Summertime Gas Storage Levels2026-08-03

-

Economics On Fires and GDP2026-07-31

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today