Personal Wealth Management / Market Analysis

Our Take on China's Weak April Data

Whilst the magnitude of the economic contraction surprised economic forecasters, lockdowns’ taking a toll was a foregone conclusion, in our view.

China’s National Bureau of Statistics (NBS) released the rest of its April economic data overnight Sunday, and as you may have surmised given Shanghai and other major economic centres remain under heavy COVID restrictions, the results weren’t pretty.[i] In a press release titled “General Trend of High-Quality Development Remained Unchanged Despite the Increased Downward Pressure on Economy,” the NBS revealed retail sales’ contraction deepened, services output fell hard, industrial production flipped negative and fixed asset investment (public and private investment in construction, machinery, equipment and real estate development) slowed.[ii] The release’s commentary highlighted strength in information technology-related services as a silver lining, but we think it is better for investors to just look the weakness in the eye.[iii] In our view, stocks don’t move on what just happened, but rather what happens over the next 3 – 30 months, and we see a strong case for Chinese economic growth to resume in relatively short order, which we think is likely to help ease global economic uncertainty.

For nearly two months now, economic analysts we follow globally have tried to assess the economic damage from this spring’s lockdowns. But it hasn’t been easy. China’s regional officials haven’t provided much transparency on their local COVID policies, and trying to figure out which cities are under restrictions has seemingly required observers to put their finest detective hats on. Even in areas where the lockdowns are widely known, the economic impact hasn’t been entirely clear, in part due to companies’ boasting about factory and office bubbles—arrangements for workers to live at their place of business in order to keep production up.[iv] Whilst that generated some positive sentiment amongst commentators we follow at the outset, it soon became clear these bubbles couldn’t maintain production if lorries couldn’t deliver components.[v] So consensus expectations weren’t great, but the results turned out to be even worse. The consensus expected industrial production to slow to 0.4% y/y growth from March’s 5.0%.[vi] Instead, it fell -2.9%.[vii] Retail sales fell a whopping -11.1% y/y, much worse than the expected -6.1% slide and March’s -3.5%.[viii] The Index of Services Production fell -6.1% y/y.[ix]

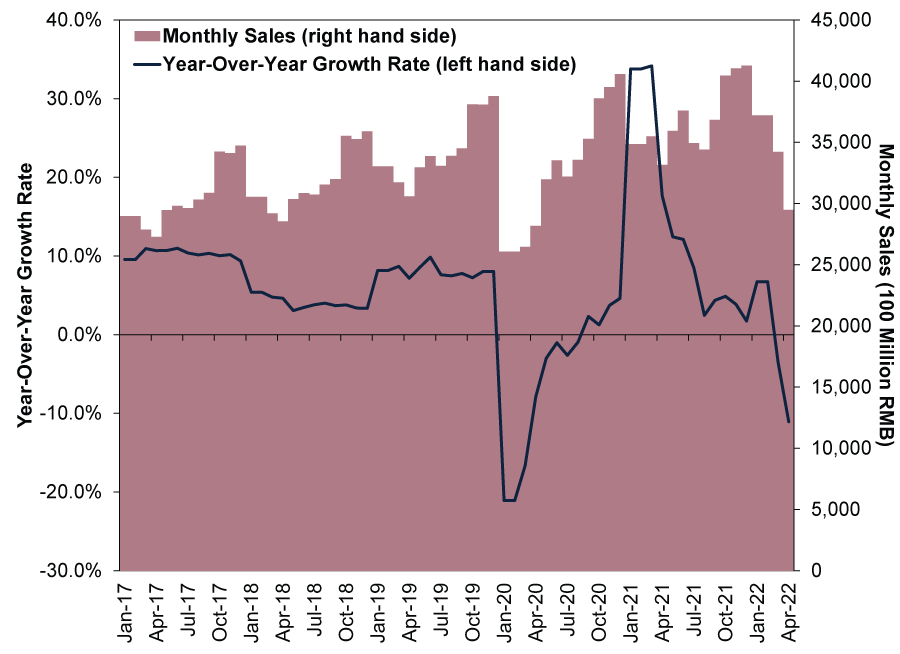

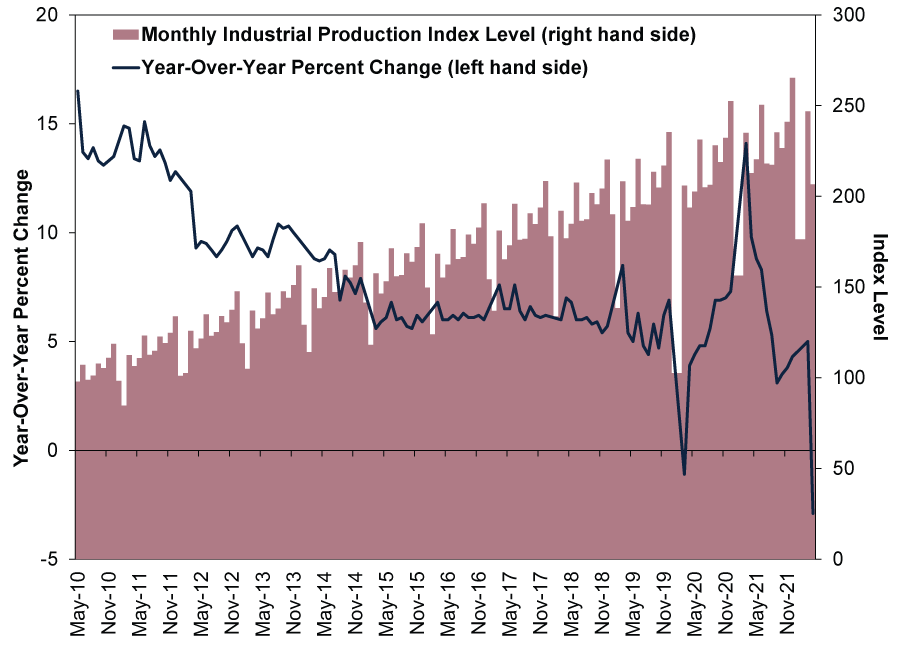

So, not good. But also, we at least now have more numbers—more data backing and illuminating what the world seemed to know intuitively. As we wrote after March’s data release, every bit of hard information theoretically helps reduce uncertainty. That is still true of the April release, in our view. April was the first full month with COVID restrictions in place this year—March was only a partial look, as Shenzhen’s lockdown reportedly began in the middle of that month, with Shanghai following toward the end.[x] Now we think the picture is more complete, helping us compare today to 2020’s lockdowns. As Exhibit 1 shows, retail sales to date have endured a milder decline this time, which we think speaks to people’s ability to adapt as well as lockdowns’ modestly more limited geographic reach. Industrial production’s decline now is deeper in percentage terms, as Exhibit 2 shows, but the level of output remained over twice as high as the average level in January and February 2020, when the first national lockdown occurred. Now, there are some seasonal factors affecting the latter comparison, as China doesn’t seasonally adjust these data, but April 2022’s level is also above April 2020’s, which was inflated by reopening.

Exhibit 1: Retail Sales

Source: FactSet, as of 16/5/2022.

Exhibit 2: Industrial Production

Source: FactSet, as of 16/5/2022.

Something else you may have noticed about these charts: Those early-2020 contractions preceded huge rebounds. We think Chinese data are likely to chart a similar course this time around, whenever reopening occurs (Shanghai officials say reopening there will begin on 1 June, but as always, we would take these things with a grain of salt until they actually happen).[xi] Yes, we have heard many commentators argue this time is different because China’s economy isn’t responding to all the stimulus that government and monetary officials are trying to throw at it. But fiscal and monetary assistance can’t really take effect in areas that aren’t open, which is another factor we saw pretty clearly two years ago. Monetary easing can’t boost consumption if people aren’t allowed outside and grocery delivery purchases are tightly controlled.[xii] We think accelerated infrastructure buildouts will probably also have to wait to bear fruit. It won’t surprise us if further stimulus gets greenlit later this summer, as the Chinese Communist Party gears up for this autumn’s National Party Congress, where Xi Jinping seeks to be reappointed as party leader and Chinese President, cementing his rule for life. Chinese officials have long demonstrated that they view economic stability as key to social stability, and we think social stability will likely make it a lot easier for Xi to keep his rivals at bay.

We don’t think stocks are likely to wait for confirmation, though. In our view, Chinese lockdowns’ negative impact on investor sentiment contributed mightily to global stocks’ renewed downturn in April and early May, helping stocks pre-price (or pre-emptively incorporate into share prices) the economic damage that is now manifesting in the data.[xiii] If the world’s experience in 2020 is a reliable guide, then we suspect Chinese weakness’s ability to surprise investors is likely to be largely spent, which theoretically helps clear global markets to start pricing China’s recovery before it shows in the data. That doesn’t preclude further volatility, as China isn’t the only scare story that appears to be souring sentiment this spring, of course, but we think it is likely to at least give global investors one less negative to chew over.[i] “General Trend of High-Quality Development Remained Unchanged Despite the Increased Downward Pressure on Economy,” National Bureau of Statistics of China, 16/5/2022, and “‘It’s Probably Worse Than Wuhan’: Experts Warn China’s COVID-19 Lockdowns Will Once Again Cripple Global Supply Chains,” Will Daniel, Fortune, 19/4/2022. Accessed through Yahoo! Finance.

[ii] “General Trend of High-Quality Development Remained Unchanged Despite the Increased Downward Pressure on Economy,” National Bureau of Statistics of China, 16/5/2022.

[iii] Ibid.

[iv] “China’s Factories Opt for Isolation Bubbles to Beat COVID Curbs and Keep Running,” Josh Horwitz and Martin Quin Pollard, Reuters, 17/3/2022.

[v] “‘It’s Probably Worse Than Wuhan’: Experts Warn China’s COVID-19 Lockdowns Will Once Again Cripple Global Supply Chains,” Will Daniel, Fortune, 19/4/2022. Accessed through Yahoo! Finance.

[vi] Source: FactSet, as of 16/5/2022.

[vii] Ibid.

[viii] Ibid.

[ix] Ibid.

[x] “China Covid Spike: Shenzhen Shuts Production, Shanghai Closes Schools,” Evelyn Cheng, CNBC, 14/3/2022, and “Shanghai Covid: China Announces Largest City-Wide Lockdown,” Staff, BBC News, 27/3/2022.

[xi] “Shanghai to End Covid Lockdown and Return to Normal Life in June Amid Economic Slowdown,” Staff, The Guardian, 16/5/2022.

[xii] “China’s Covid Lockdowns Are Hitting More Than Just Shanghai and Beijing,” Evelyn Cheng, CNBC, 5/5/2022.

[xiii] Source: FactSet, as of 17/5/2022. Statement based on MSCI World Index return with net dividends in GBP, 1/4/2022 – 16/5/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics This Week in Gridlock: Europe Edition2026-03-27

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-18

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-18

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today