Personal Wealth Management / Market Analysis

Sector Check-In: Global Energy Shares

Global Energy returns have cooled off lately.

Global equities have kept clocking new highs through the summer, but one sector is notably absent from the party: Energy, which also happened to be the best-performing sector in 2021’s first half.[i] Amongst financial commentators we follow, that hot start fanned widespread expectations that vaccines, reopening, resurgent travel and a new Roaring Twenties mirroring the 1920s’ global economic upswing. Many commentators we follow predicted this would stoke vast demand for fuel, making oil-related shares surefire winners for a long while. Yet now Energy has returned to earth somewhat.[ii] We don’t think dismal times are likely in store for the sector, but its recent travails show the danger in extrapolating hot performance forward.

Energy’s 34.1% return through mid-June far outpaced the MSCI World Index’s 9.6%.[iii] Propelling this move, in our view: oil prices, which our research indicates are Energy’s main driver. Brent crude oil climbed from about $50 (£37) a barrel at 2021’s start to over $75 (£57) in July.[iv] Throughout that stretch, commentators we follow claimed countries’ reopening from COVID lockdowns and rebounding travel would send demand soaring. In their view, coupled with American shale drillers’ and OPEC’s seemingly newfound production discipline, limited supply would supposedly keep oil prices elevated.

This all sounded a bit overstated to us. Yes, easing lockdown restrictions likely raises demand, but in our view, probably only back to a pre-pandemic normal. After an initial pop, we didn’t think extrapolating accelerating growth forevermore appeared wise. Then, too, in markets, economic theory holds that higher prices invite greater production. Maybe at a lag, but with the Middle East’s abundant proven reserves and America’s ready supply of drilled but uncompleted wells, global production seemed quite likely to rise before too long.[v] This in turn seemed likely to keep a lid on oil prices—and Energy shares, as our research shows oil producers’ earnings are more sensitive to oil prices than production volumes.

That now seems to be playing out. In August, Brent crude oil sunk toward $65 (£48) before bouncing somewhat.[vi] Meanwhile, Energy’s year-to-date return has shrunk to 22.3%—its lead over the MSCI World Index’s 16.8% substantially diminished.[vii] Many commentators we follow attribute this to COVID’s Delta variant inspiring new restrictions, which we think probably is hitting sentiment somewhat. But in our view, the world isn’t close to spring 2020’s nearly complete global shutdown of economic activity. So-called zero COVID nations like Australia and New Zealand thus far appear to be the exception, not the rule. More broadly, we think markets have simply priced in the reopening pop—plus commentators’ pronouncements—and are looking beyond it to the likely slower-growth reality ahead along with a more balanced oil supply and demand landscape.

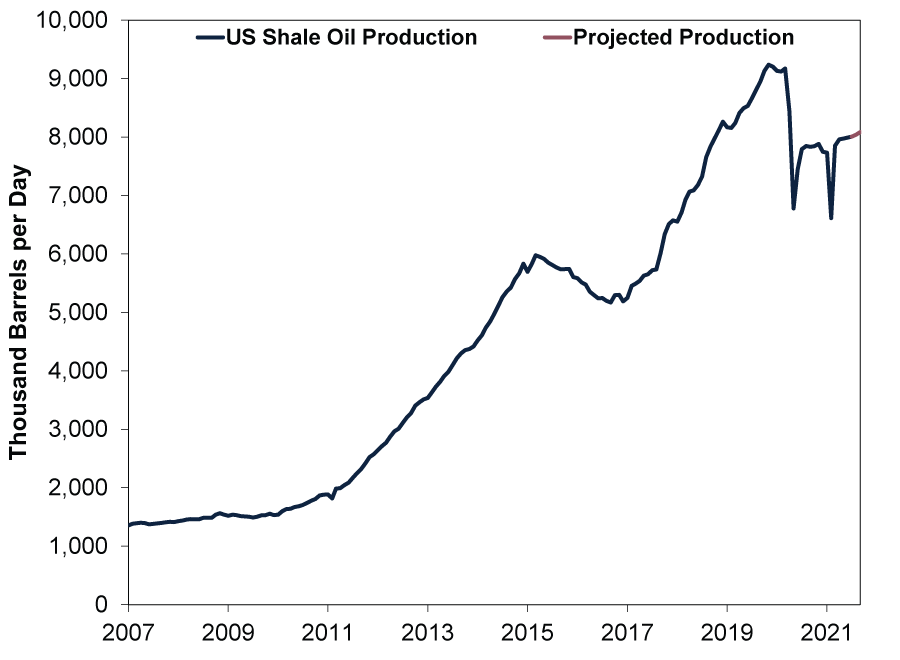

Now, we don’t think it is wise to extrapolate Energy shares’ recent drop forward, either. Some of its magnitude also looks sentiment-driven, in our view. Yet we think there are some fundamental shifts at work, too: Chiefly, global supply appears to be rising to meet post-lockdown demand. For example, US shale supply is ramping up. (Exhibit 1) After two brief dips in May 2020 (lockdown-related) and February 2021 (weather-related), shale production was off as much as -28% from its November 2019 peak. As of July, it is still down -13% from there, but industry projections see it climbing higher in the coming months.

Exhibit 1: US Shale Oil Output Ramping Back Up

Source: EIA, as of 16/8/2021. US shale oil output, January 2007 – July 2021, projected production, August 2021 – September 2021.

Shale oil drillers—the bulk of America’s current world-leading 11.4 million barrels per day (bpd) production—have demonstrated the ability to produce over 9 million bpd.[viii] We don’t think there is any reason they can’t get there again as long as it is economical to do so. Moreover, it isn’t just the US that can readily boost daily oil production by millions of barrels, according to oil industry research. Russia and Saudi Arabia, the world’s number two and three producers, respectively, have self-imposed quotas for a reason—they have ample spare capacity, based on their production history.

The question occupying commentators we follow now seems to be whether demand will be there. Delta-variant breakouts may delay reopening in some places, but in our view, the world economy has experienced erratic lockdowns for over a year—thus far, the vast majority of economic data indicate they aren’t stopping overall recovery.[ix] COVID restrictions in China, Japan, Australia and New Zealand are well-known, with their surprise power over markets seemingly sapped.[x] Though sentiment swings can drive periodic volatility in oil, we think markets mostly see through these fits and starts.

Over the 3 – 30 month stretch we think markets focus on, we forecast global economic activity likely returning toward pre-pandemic trends, including oil supply and demand. Our research shows oil producers aren’t capacity constrained, and as supply chain kinks elsewhere resolve, demand appears likely to grow modestly. For the US and China, the world’s largest economies, GDP already exceeds pre-lockdown levels.[xi] In America’s case, except for areas like travel and recreation, pent-up demand has already been unleashed and is petering out as normal habits return, based on the latest economic indicators.[xii] We think the reopening rebound is mostly behind them and suspect the rest of the world is likely to follow that general trajectory.

In the environment we think is likely, oil prices probably continue hovering around current levels—much like they did pre-pandemic. Based on our research, that has proven profitable enough for Energy, particularly for the higher-quality firms in the sector with lower drilling costs and less debt to service. But we don’t think a return to the heady days of early-2021 robust leadership is likely. Perhaps more sentiment adjustment—and volatility—is in store, but in our view, longer-term Energy expectations seem broadly back in line with a balanced global oil supply-demand outlook.

[i] Source: FactSet, as of 26/8/2021. Statement based on MSCI World Energy and MSCI World returns with net dividends, 31/12/2020 – 25/8/2021.

[ii] Ibid.

[iii] Ibid. MSCI World Energy and MSCI World returns with net dividends, 31/12/2020 – 15/6/2021.

[iv] Ibid. Brent crude oil price, 31/12/2020 – 31/12/2021. Converted to GBP at 25 August exchange rates.

[v] Source: US Energy Information Administration and Organisation of Petroleum Exporting Countries, as of 26/8/2021.

[vi] Ibid. Brent crude oil price, 31/7/2021 – 25/8/2021.

[vii] Ibid. MSCI World Energy and MSCI World returns with net dividends, 31/12/2020 – 25/8/2021.

[viii] Source: US Energy Information Administration, as of 18/1/2021. Weekly US field production of crude oil, thousand barrels per day, 13/8/2021.

[ix] Source: IMF, as of 27/7/2021. Statement based on world GDP, 2019 – 2021.

[x] “Delta Blow Knocks Wind out of Asia’s Economic Recovery,” Daniel Leussink and Gaurav Dogra, Reuters, 24/8/2021.

[xi] Source: FactSet, as of 26/8/2021. Statement based on US and China GDP, Q4 2019 – Q2 2021.

[xii] Ibid. Statement based on US personal consumption expenditures, Q4 2019 – Q2 2021.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-18

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-18

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today