Personal Wealth Management / Market Analysis

Today’s Dour Consumer Moods Don’t Necessarily Foretell Their Future Actions

Consumer sentiment surveys aren’t a roadmap of things to come, in our view.

America’s University of Michigan (U-Mich) released the preliminary May results for its widely watched consumer sentiment survey last week. Perhaps unsurprisingly, given the rampant handwringing in financial publications we follow over the country’s West Coast regional banks and the simmering standoff in America’s Congress over raising the country’s statutory debt limit, the index fell to a six-month low.[i] But today’s downbeat consumers don’t necessarily foreshadow things to come, in our view, as the U-Mich survey’s history illustrates.

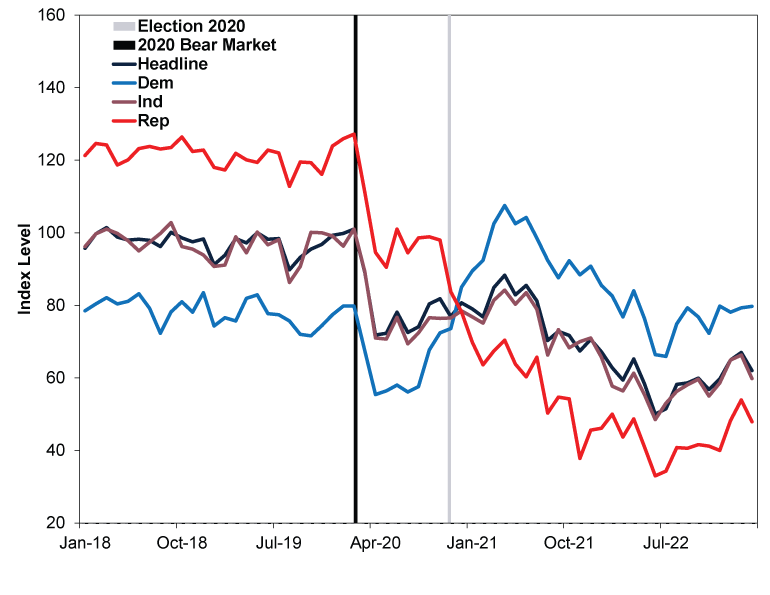

The U-Mich consumer sentiment index fell to 57.5 from April’s 63.5, below expectations and the weakest reading since last November.[ii] Survey readings have been broadly dour since February 2020, which we think is likely tied to the first COVID restrictions starting to take effect in developed nations and the global bear market.[iii] Responses have also persistently exhibited a noticeable partisan divide—highlighting politics’ effect on people’s moods, in our view. For example, those who identified as Republican have consistently responded more negatively than those who identified as Democratic since November 2020, when Democratic candidate Joe Biden won the presidential election. (Exhibit 1) But regardless of party affiliation, U-Mich’s gauge has yet to return to pre-pandemic levels.

Exhibit 1: U-Mich Consumer Sentiment Index Since 2018

Source: FactSet and the University of Michigan’s “Survey of Consumers,” as of 16/5/2023. Consumer Sentiment Index Level, headline and by political party, monthly, January 2018 – March 2023. March 2023 is the latest available for Consumer Index Level by political party.

The May survey also noted issues from prolonged recession to debt ceiling fallout weighing on respondents.[iv] Prices remain on people’s minds, too, as long-run (i.e., five-year) annual inflation rate expectations hit 3.2%, the highest since 2011.[v] We aren’t surprised these topics colour respondents’ outlooks. Like Brits and those on the Continent, Americans have been grappling with challenging conditions for the past couple years, from elevated inflation (rising prices across the economy) and tragic geopolitical developments to financial sector troubles and seemingly nonstop political bickering. But from an investing perspective, we think it is critical to remember people’s views of the future aren’t predictive.

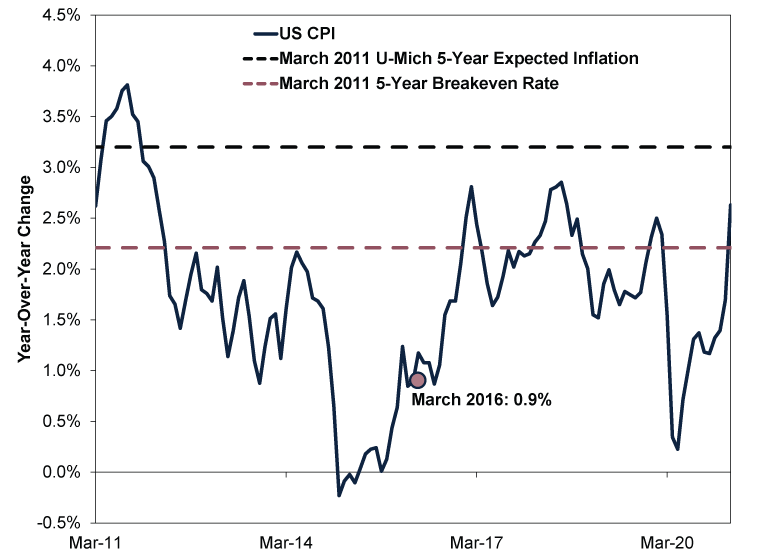

One way to see this: those long-run inflation expectations. Go back to March 2011, when US consumers’ inflation expectations were as high as today’s.[vi] Then, rising petrol prices were U-Mich survey respondents’ biggest gripe.[vii] US retail petrol prices had been climbing from December 2008’s relative low of $1.75 a gallon, but price growth began accelerating in late 2010—climbing from $2.76 a gallon in September 2010 to $3.62 a gallon in March 2011.[viii] That jump fuelled (sorry) fears that petrol would get back to mid-2008 highs and stay there, based on financial headlines we monitored at the time, rendering the earlier drop a short, recession-related aberration. With March 2011’s headline inflation up to 2.6% y/y, U-Mich respondents’ five-year inflation outlook ticked up from February’s 2.9% to March’s 3.2%.[ix]

Those expectations perhaps looked prescient in the short term as inflation broke through the 3.0% threshold the next month and remained there for the rest of the year (peaking in September at 3.8%).[x] Petrol prices also hit a relative high of $3.96 a gallon in May and stayed in the $3-range for the next three years.[xi] But consumer price growth ended up slowing over the next several years—and there was even a short bout of deflation in early 2015. (Exhibit 2) Five years from March 2011, the Consumer Price Index (CPI) inflation rate was just 0.9% y/y. Interestingly, in March 2011 a market-based measure of inflation expectations called the five-year breakeven inflation rate—which is based on nominal Treasury bond yields and inflation-linked Treasury bond yields—was 2.2%, a full percentage point lower than U-Mich survey respondents’ prediction.[xii] Though 5-year Treasury investors’ outlook was closer to reality than consumers’, it was still well wide of the mark—a reminder, in our view, that the distant future is unknowable and inflation expectations aren’t predictive. We think they are, at best, coincident.

Exhibit 2: US CPI vs. Expectations

Source: FactSet and St. Louis Federal Reserve, as of 16/5/2023. US CPI (year-over-year change), March 2011 – March 2021, 5-year expected inflation from University of Michigan’s “Survey of Consumers” for March 2011 and 5-year breakeven inflation rate as of 31 March 2011.

Although we don’t think the U-Mich survey has many forward-looking takeaways, its findings are consistent with other sentiment gauges in America and abroad. For example, US IPO (initial public offering) activity is at a post-pandemic low.[xiii] Based on our research, surges in IPOs may signal optimism turning into euphoria as businesses go public to take advantage of hot demand. We saw those conditions in the late 1990s and early 2000 and, to a lesser extent, in early 2021 (e.g., special-purpose acquisition company debuts, or SPACs, which are holding companies created for the purpose of merging with a startup and taking it public). Likewise, our analysis has found that a dearth of activity can indicate low demand—perhaps signalling pessimism’s prevalence. Elsewhere, Bank of America’s global fund manager survey found sentiment worsened in early May, with 65% of those polled anticipating further economic weakness.[xiv] On the Continent, Germany’s ZEW Indicator of Economic Sentiment fell back into negative territory for the first time since December 2022.[xv] No one sentiment metric is all-telling, according to our research, but when taken in aggregate, today’s measures suggest a majority are feeling down about the economy.

For investors, we think the key question to ask is how these expectations align with economic reality. We see lots of signs the US and many other developed economies are muddling along. There are weak spots, but tepid growth is a far cry from recession—which policymakers in the UK and EU have recognised recently. In our view, the wall of worry bull markets (prolonged periods of rising equity prices) climb is high, and we see more and more signs that is the situation today.

[i] Source: FactSet, as of 16/5/2023. The debt ceiling is the statutory limit on the amount of US federal debt the country can have at any given time.

[ii] Ibid.

[iii] Ibid. MSCI World Index returns with net dividends, in GBP, 20/2/2020 – 16/3/2020. A bear market is a prolonged, fundamentally driven broad equity market decline of -20% or worse.

[iv] Source: University of Michigan, as of 12/5/2023. “Surveys of Consumers,” preliminary results for May 2023. Recession is a protracted, economy-wide decline in economic activity.

[v] Ibid.

[vi] See note i.

[vii] “Consumer Sentiment Declines Sharply in March,” Bill McBride, Calculated Risk, 11/3/2011.

[viii] Source: US Energy Information Administration, as of 16/5/2023. US Retail Gasoline Prices (All Grades, All Formulations), monthly.

[ix] See note i. Statement based on the US Consumer Price Index (CPI), year-over-year change, March 2011, and University of Michigan 5-Year Inflation Expectations, February – March 2011. CPI is a government-produced measure that tracks prices across the economy.

[x] Ibid. Statement based on US CPI, year-over-year change, March 2011 – December 2011.

[xi] See note viii.

[xii] Source: St. Louis Federal Reserve, as of 19/5/2023. Statement based on 5-year breakeven rate on 31/3/2011.

[xiii] “Level of IPO Filings Reveal Dour Investor Sentiment,” Thomas K. Brown, Bankstocks.com, 11/5/2023. IPOs are formerly private companies that list and sell shares to investors on public stock markets.

[xiv] “Investors Most Pessimistic So Far This Year, BofA Survey Shows,” Ksenia Galouchko, Bloomberg, 16/6/2023. Accessed via Yahoo! Finance.

[xv] “Expectations Decline Sharply,” ZEW, as of 16/5/2023.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

-

Market Analysis February’s Growthy Data—and the Iran War’s Souring Sentiment2026-03-06

-

Market Analysis Putting the Latest Private Credit Implosion in Perspective2026-03-06

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today