Personal Wealth Management / Market Analysis

What to Make of Recent Wintertime Blues

The latest sentiment measures confirm moods are down—what does that mean for markets?

Based on the financial headlines we monitor, it seems 2023 can’t come soon enough for investors. Global stocks are down this month, and based on the latest sentiment gauges we have reviewed, wintertime blues are prevalent.[i] Down moods are understandable, but we think investors benefit from remembering feelings alone don’t predict the economy or stocks.

The recent spate of sentiment surveys in the US and Europe showed some minor improvements, but the picture still appears dour overall. Bank of America’s December fund manager survey found a majority of investors (68%) think recession (a broad, economy-wide decline in activity) is likely in the next 12 months, easing a bit from November’s 77%.[ii] A recent Bankrate poll noted about two-thirds of surveyed US adults don’t think their personal finances are likely to improve in 2023, with about 3 in 10 Americans anticipating their situation will worsen.[iii]

In the UK, research firm GfK reported its consumer-confidence barometer improved to -42 in December from November’s -44.[iv] Yet this was the 8th straight monthly reading of -40 or worse—a first since GfK’s records begin almost 50 years ago—as some slight improvement in their view of next year’s general economic situation didn’t prevent consumers from feeling down about their personal finances.[v] The Ifo institute announced German business morale was better than expected in December, with the gauge measuring feelings about the future rising to 83.2 from November’s 80.2, and though economists acknowledged the probability of recession fell a bit, a downturn is still the baseline forecast.[vi]

Now, we think sentiment measures are useful as coincident indicators (meaning they show respondents’ feelings in the moment), but our research has found they don’t reveal future activity. In our experience, human emotions are fickle, and moods can change based on a multitude of reasons, from reading something on social media to experiencing a personal, real-life event (e.g., receiving a pay raise or lack thereof). For an illustrative hypothetical example, consider someone who reads an article about weaker-than-expected Black Friday retail sales right before taking a December survey. That news could dampen her mood, so she responds she is less optimistic about the economy in the coming months. But what if the next day she visits her favourite retail shop, serendipitously finds a deal on a big-ticket item on her wish list and ends up purchasing it? This is only a hypothetical, but our research shows consumer sentiment doesn’t indicate much about consumer spending.

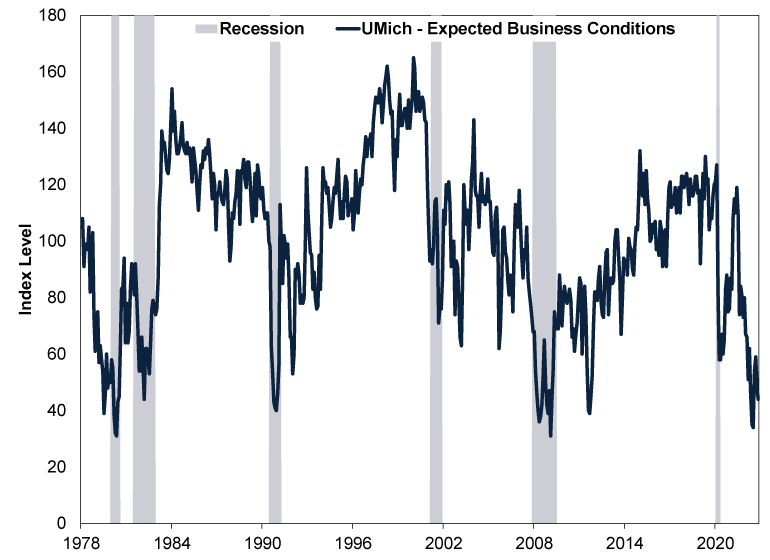

Taking this concept more broadly, we have found feelings about the future don’t tell you much about upcoming economic growth. Take the widely watched, US-focussed University of Michigan Consumer Sentiment survey, which asks myriad questions—including one about expected business conditions in the next 12 months. As Exhibit 1 shows, extreme lows usually occur during recessions—not before—and there are plenty of big declines during economic expansions.

Exhibit 1: Expected Business Conditions Aren’t Predictive, US Edition

Source: FactSet, as of 19/12/2022. University of Michigan Survey of Consumers – Business Conditions Expected During the Next Year, monthly, January 1978 – November 2022. Recession dating based on the National Bureau of Economic Research’s US business cycle dates.

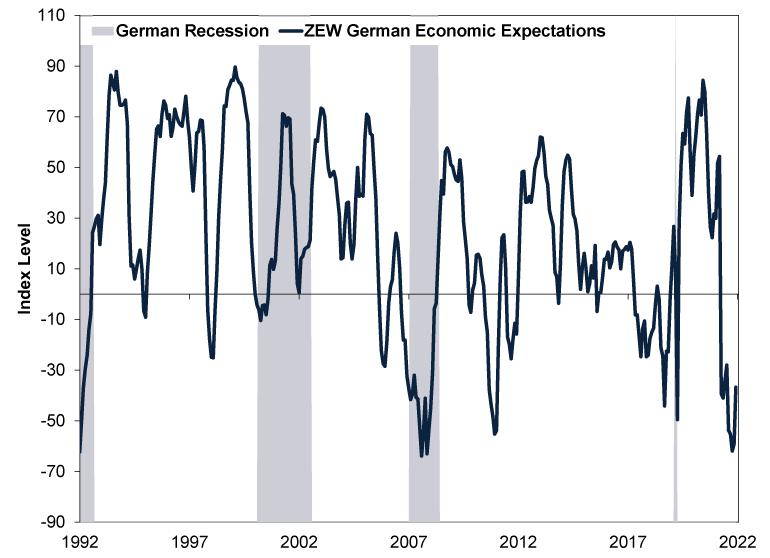

This isn’t just a US phenomenon—see Germany, Europe’s largest economy.[vii] In the ZEW economic sentiment index, negative readings indicate a majority of surveyed analysts have a pessimistic view of the German economy over the next six months. As Exhibit 2 shows, yes, there are times when pessimistic expectations seemed to align with the start of recession. But there are also times when views were negative and Germany didn’t enter recession, including the past decade.

Exhibit 2: Expected Business Conditions Aren’t Predictive, German Edition

Source: FactSet, as of 19/12/2022. ZEW Financial Market Survey – Economic Expectations, December 1992 – November 2022. German recession dating based on business cycles determined by the German Council of Economic Experts.

We don’t think it is a shock people are moody now amidst grim forecasts, feared energy shortages and deteriorating economic data. But in our view, sentiment surveys just reflect all of this widely known information—they don’t say much new or what will happen next. What actually happens over the next 3 – 30 months and how that squares with these dour expectations is what will move stocks, in our view.

[i] Source: FactSet, as of 21/12/2022. Statement based on MSCI World Index returns with net dividends in GBP, 30/11/2022 – 20/12/2022.

[ii] “BofA Survey Says Investors Are Less Gloomy on Growth Over China,” Sagarika Jaisinghani, Bloomberg, 13/12/2022. Accessed via Yahoo! Finance.

[iii] “Survey: 66% of Americans Don’t See Their Finances Improving in 2023,” Sarah Foster, Bankrate.com, 18/12/2022. Accessed via MSN.

[iv] “UK Consumer Confidence Edges Up But Still Close to Record Low,” Staff, Reuters, 15/12/2022. Accessed via MSN.

[v] Ibid.

[vi] “German Business Morale Approaches 2023 on High Note – Ifo,” Staff, Reuters, 19/12/2022. Accessed via Nasdaq.com.

[vii] Source: World Bank, as of 21/12/2022. Statement based on German gross domestic product (GDP) in constant 2015 USD. GDP is a government-produced measure of economic output.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Q1 2026 Global Markets Review & Outlook2026-05-12

-

Macro Insights Why Global Small Cap2026-05-07

-

Market Analysis What to Think of Another Aussie Rate Hike2026-05-05

-

Market Analysis Europe’s Resilient Q1 GDP2026-05-01

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today