Personal Wealth Management / Market Analysis

Why the Emergency Oil Reserve Release Isn’t a Game Changer

The US, UK and other countries’ coordinated move likely doesn’t change longer-term global oil supply much.

After weeks of signalling it was preparing to do so, the US President Joe Biden’s administration announced today it will attempt to curb petrol prices by releasing 50 million barrels of oil from America’s Strategic Petroleum Reserve (SPR), part of a coordinated release with China, Japan, South Korea, India and the UK. The UK will contribute 1.5 million barrels from its emergency reserves, India has pledged 5 million, and the other three are finalising their plans.[i] And in response to this forthcoming supply increase, global oil prices rose.[ii] Yes, a move designed to rein in oil prices seemingly had the opposite of its intended effect, illustrating emergency reserves’ complicated relationship with oil prices. Whilst moves like these can have a short-term impact—predominantly through sentiment—we think they do little to change longer-term supply and demand fundamentals.

Oil prices are set globally, on world supply and demand fundamentals. The US’s 50 million barrel contribution to the global release represents less than 0.2% of global production, based on October’s output.[iii] The full global release will likely be around 65 to 70 million barrels, according to industry researchers’ calculations, which is nowhere near enough to move the needle over any meaningful stretch.[iv] This is partly because the Organization of the Petroleum Exporting Countries (OPEC) also has a great deal of influence on global supply and is reportedly planning a counter move next week.[v] Previously, OPEC and Russia were coordinating to increase output by 400,000 barrels per day.[vi] If the cartel decides to slow or pause production increases, it would likely neutralise the coordinated supply release. In our view, markets are likely weighing the totality of the global supply landscape.

Even if OPEC sits tight, the release of emergency reserves likely has little long-term impact. It might help curb oil and petrol prices by a bit in the near term, but it likely won’t alter the longer-term supply and demand landscape. That will probably depend on private producers boosting output, which is already starting. The US, which is one of the largest global producers, has added 67 oil rigs since the beginning of September, bringing total rig count to 461 as of last week.[vii] Last week’s American industrial production report showed oil and gas well drilling rising 9.3% m/m in October, bringing the cumulative increase since July 2020’s low to 93%.[viii] The International Energy Agency (IEA) reported global oil production rose by 1.4 million barrels per day (bpd) last month and pencilled in a further 1.5 million bpd increase over the rest of this year.[ix] That is just a forecast, but it seems sensible to us based on the rise in drilling activity. As global output rises, we think it is likely to help supply and demand come back into balance, which will likely help stabilise prices.

Perhaps the emergency release helps tide drivers over until then. But the history of emergency releases’ impact on prices is spotty. Whilst this is the first time the US has tapped the SPR for the express purpose of taming prices, rather than addressing an acute supply disruption, it is the fourth emergency release on record. The others happened during the first Gulf War in 1991, the aftermath of Hurricane Katrina in September 2005, and during the Arab Spring and Libya’s civil war in June 2011.

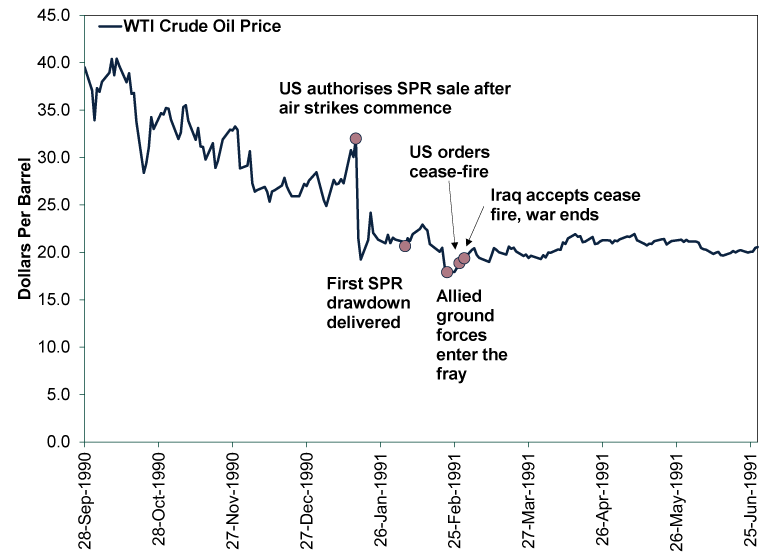

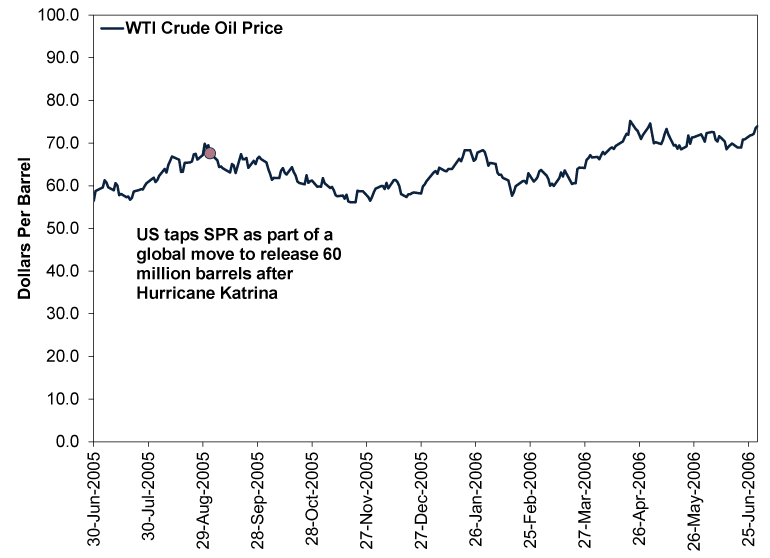

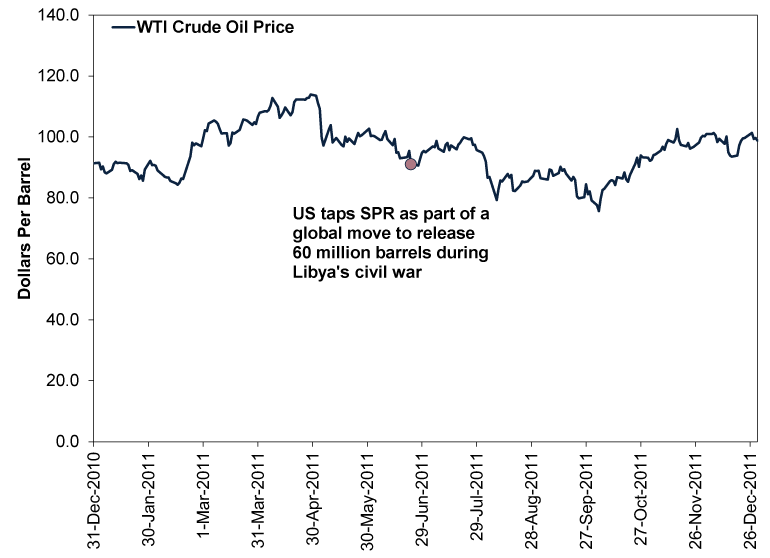

The results were overall mixed. Using US oil prices for their theoretically higher sensitivity to US reserve releases, crude oil prices did drop immediately after officials announced the SPR release in the immediate aftermath of the first US air strikes in 1991, but we think it is an open question whether oil prices’ relief stemmed from the emergency action or the increased clarity on the war’s short duration. (Exhibit 1) Our research shows oil prices, like stocks, can be volatile in the run up to a conflict before stabilising after the fighting starts. In 2005, the US’s release was part of a coordinated global move. Then, too, prices drifted lower as the release bought time for America’s Gulf Coast refineries to reopen after the storm. (Exhibit 2) But by late November, prices were rising again. Finally, in 2011, prices actually rose for a month after the global oil reserve release. (Exhibit 3) Perhaps they would have risen even more had the IEA not coordinated, but that counterfactual is unknowable, in our view.

Exhibit 1: Emergency Reserves and Oil Prices, Gulf War Edition

Source: FactSet, and US Department of Energy, as of 23/11/2021. West Texas Intermediate (WTI) Crude Oil Spot Price, 30/9/1990 – 30/6/1991. Please see the addendum at the end of this article for a longer history of WTI Crude Oil prices.

Exhibit 2: Emergency Reserves and Oil Prices, Hurricane Katrina Edition

Source: FactSet and US Department of Energy, as of 23/11/2021. WTI Crude Oil Spot Price, 30/6/2005 – 30/6/2006. Please see the addendum at the end of this article for a longer history of WTI Crude Oil prices.

Exhibit 3: Emergency Reserves and Oil Prices, Libya Civil War Edition

Source: FactSet and US Department of Energy, as of 23/11/2021. WTI Crude Oil Spot Price, 31/12/2010 – 31/12/2011. Please see the addendum at the end of this article for a longer history of WTI Crude Oil prices.

So if you are hoping for the emergency release to lighten the load on your pocketbook this autumn and winter, we suggest tempering your expectations. Maybe it shaves a few pence off the price of petrol, maybe not. But our research shows markets are extraordinarily good at solving problems like this, and we think they have already been hard at work telling producers it is time to ramp up. Increased drilling activity indicates producers are listening, and soon they appear likely to deliver a more meaningful, lasting supply increase.

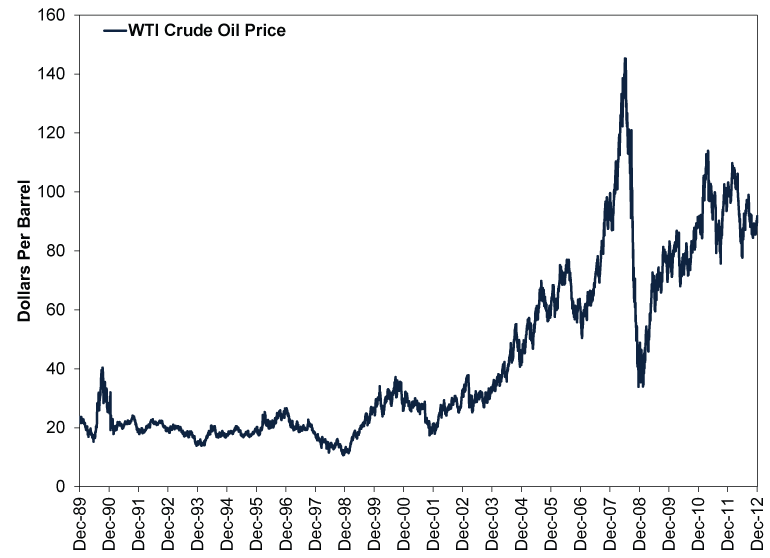

Addendum: WTI Oil Prices, 1989 – 2021

Source: FactSet, as of 24/11/2021. WTI Crude Oil Price, 31/12/1989 – 31/12/2012.

[i] “These Countries Are Joining the US in Tapping Their Emergency Oil Reserves,” Walé Azeez, CNN Business, 23/11/2021.

[ii] Source: FactSet, as of 23/11/2021. Statement based on West Texas Intermediate (WTI) and Brent Crude Oil Prices on 23/11/2021.

[iii] Source: International Energy Agency, as of 23/11/2021.

[iv] “US Joins With China, Other Nations in Tapping Oil Reserves,” Timothy Puko and Alex Leary, The Wall Street Journal, 23/11/2021. Accessed via MSN.

[v] “OPEC Considers Lowering Production to Account for Oil Reserve Releases,” Grant Smith, Salma El Wardany and Debjit Chakraborty, World Oil, 22/11/2021.

[vi] “OPEC+ Agrees to Stick to Oil Production Plan, Defying US Pressure,” Natasha Turak, CNBC, 4/11/2021.

[vii] Source: FactSet, as of 1/23/2021. Baker Hughes Rotary Rig Count, Oil, 9/3/2021 – 11/19/2021.

[viii] Source: FactSet, as of 11/16/2021.

[ix] See Note iii.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Global Bond Calamity Calls for Calm Perspective2026-05-27

-

Economics A May Global Economic Check-In2026-05-26

-

Macro Insights Macro Insights Q2 20262026-05-22

-

Politics A Market-Orientated Perspective on the UK’s Political Ructions and Q1 Economic Results2026-05-15

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today