Personal Wealth Management / Market Analysis

An End-of-May Check-in on the Global Economy

Whilst revised German Q1 GDP growth showed contraction, the latest flash PMIs suggest growth persists in most major developed economies.

Thursday morning, Germany released revised Q1 gross domestic product (GDP, a government-produced measure of economic output), which flipped a flat quarterly read to contraction—the second-straight quarterly dip.[i] Headlines we follow seized upon this as a revision to recession (a protracted, broad decline in economic activity), which we guess is to be expected. However, those data are quite old and unsurprising, in our view. Moreover, earlier this week S&P Global released their May flash purchasing managers’ indexes (PMIs), suggesting most major developed nations continued growing into Q2.[ii] May’s readings didn’t yield much that is altogether new, but we think they offer more evidence the global economy has been faring better than the consensus views we read at the beginning of the year.

PMIs are monthly business surveys, in which readings above 50 imply expansion. They have their limits—e.g., they indicate only how widespread growth or contraction is, not the magnitude—but we think they are amongst the most timely gauges of recent business activity. Germany is a good example, in our view. Q1 composite PMI readings (which combine manufacturing and services) read 49.9, 50.7 and 52.6 in the quarter’s three months.[iii] Based on our research, those mixed, narrowly contractionary and expansionary readings are consistent with the mild contraction in Q1 GDP.

May’s flash readings, which reflect approximately 85% – 90% of total responses, had some notable takeaways: Japan, for instance, reported the strongest rise in private sector activity in nearly a decade.[iv] The country’s services PMI registered its best-ever reading, with record expansions in total new business, exports and outstanding business—with many respondents crediting the resumption of domestic and international tourism as COVID-related disruptions waned.[v] The strong report may foment further investor optimism towards the Land of the Rising Sun, though we think it is easy to overstate the country’s prospects.

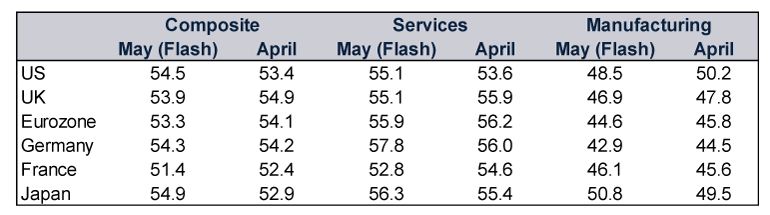

Broadly speaking, though, May’s preliminary PMIs didn’t deviate much from April’s readings. (Exhibit 1)

Exhibit 1: The Latest PMIs

Source: FactSet and S&P Global, as of 25/5/2023.

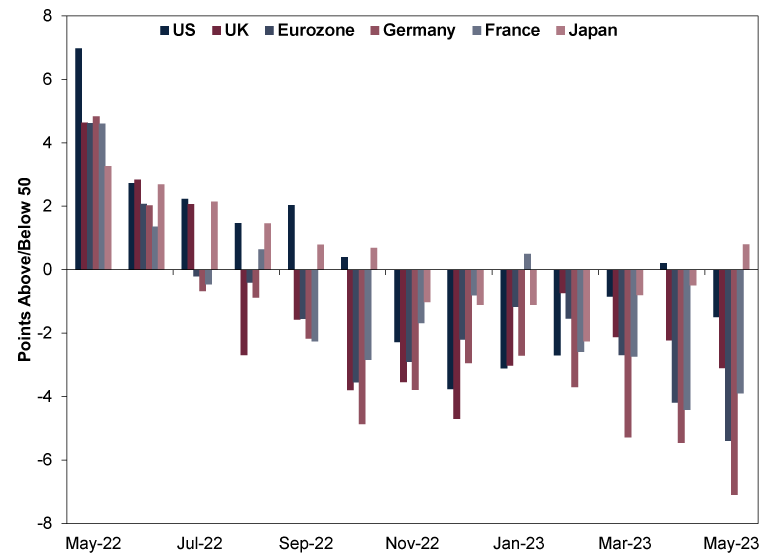

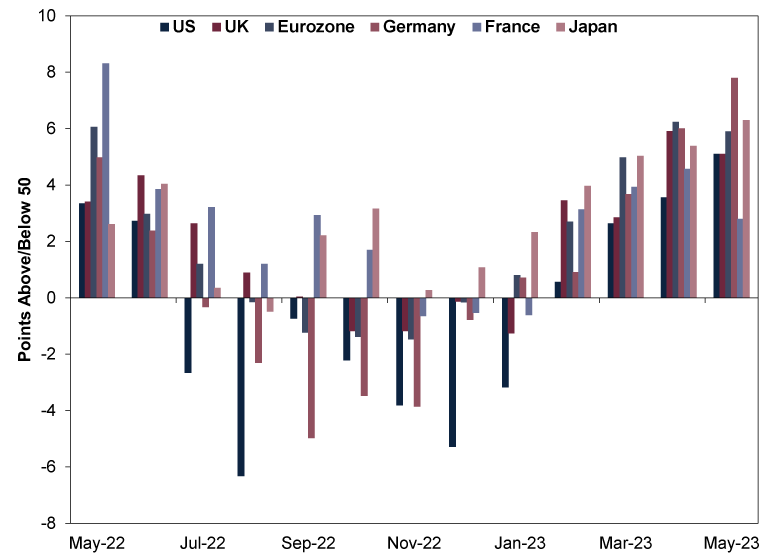

May’s numbers did add to the ongoing split between manufacturing and services. Since last summer, manufacturing and services PMIs for major developed economies signalled contraction during the back half of 2022. But though manufacturing has remained in contraction this year, services has returned to expansion. (Exhibits 3 – 4)

Exhibit 2: Whilst Manufacturing Has Contracted…

Source: FactSet, as of 25/5/2023.

Exhibit 3: … Services Has Returned to Growth

Source: FactSet, as of 25/5/2023.

Services comprise the lion’s share of GDP in major developed economies, and we think ongoing services growth has more than offset manufacturing weakness in most nations.[vi] Consider: With the exception of Germany (-1.3%), Q1 GDP grew on an annualised basis in America (1.3%), the UK (0.5%), the eurozone (0.3%), France (0.7%) and Japan (1.6%).[vii]

We think PMIs suggest growth is overall persisting, and based on our research, they suggest Germany’s dip may reverse in Q2. Now, surveys won’t provide the detail output measures (e.g., GDP, industrial production and retail sales) can, but we think the latter are even more backward-looking given their lag time. For example, Eurostat released March eurozone industrial production (which fell -4.1% m/m) a week and a half ago—which is nearly two months after S&P Global announced a sub-50 manufacturing PMI for the eurozone.[viii]

That doesn’t mean PMIs are more useful than output gauges, in our view, as both have benefits and drawbacks when assessing the economy. But for all their lack of new information and the limited takes on the future, these gauges again suggest the deep, global recession commentators we follow have long expected—and keep shifting further into the future—still likely isn’t here.[ix] Perhaps that can help people realise those worst-case scenarios aren’t coming to pass—allowing them to move on and focus on a better-than-appreciated reality.

[i] Source: Destatis, as of 25/5/2023.

[ii] Source: S&P Global, as of 23/5/2023.

[iii] Source: FactSet, as of 25/5/2023.

[iv] Source: S&P Global, as of 23/5/2023.

[v] Ibid.

[vi] Source: The World Bank, as of 26/5/2023. Statement based on the value added of services sector as a percentage of GDP for the eurozone, Germany, France, the United Kingdom, the United States and Japan. All as of 2021 except for Japan (2020).

[vii] Source: FactSet, as of 25/5/2023. An annualised growth rate refers to the rate GDP would grow over an entire year if the quarter-on-quarter growth rate persisted all four quarters.

[viii] Source: Eurostat and FactSet, as of 25/5/2023.

[ix] “Eurozone Economy Avoids Recession ‘By a Whisker,’” Larry Elliott, The Guardian, 28/4/2023.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-14

-

Politics Can Germany Engineer Faster Growth at Last?2026-07-08

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-02

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today