Personal Wealth Management / Market Analysis

June’s Global Flash PMIs Still Look Ok

With more businesses reporting growth than not, we think recession still doesn’t look like a foregone conclusion.

Another month, another round of flash purchasing managers’ indexes (PMIs) giving an early read into major economies’ business activity. Though these business surveys from S&P Global mostly ticked down in June (as we will show), prompting more recessionary chatter from commentators we follow, their levels still indicate overall expansion based on the surveys’ methodology.[i] It may not be robust, but we don’t think stocks need perfection to mount a recovery from this year’s downturn—just for reality to beat dreary analyst forecasts and sour investor sentiment.[ii]

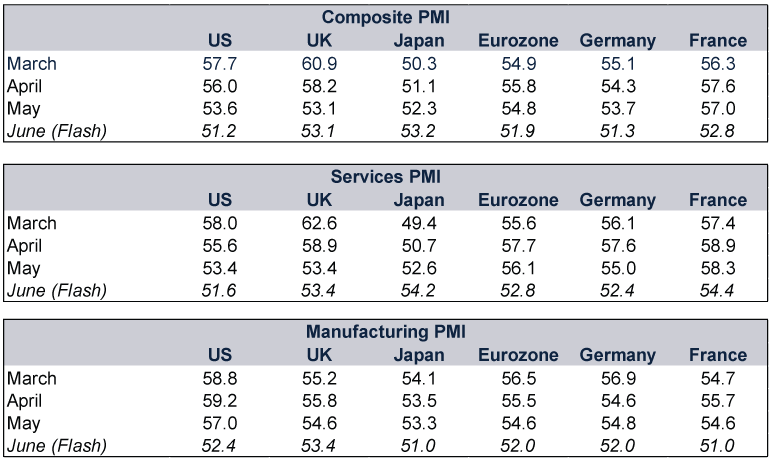

PMIs are surveys that aim to measure growth’s breadth. Readings above 50 indicate the majority of surveyed firms reported expanding business activity, hence, PMI readings over 50 signal growth and under 50 contraction—with growth (and contraction) theoretically accelerating the further readings drift from that marker. PMIs don’t say anything about how much their businesses grew (or shrank), only that they did, so we think they are a timely but loose estimate of economic activity at best. Amongst the various readings, the composite PMI combines services and manufacturing, but it is a narrower measure of their output that focusses only on production. The services and manufacturing PMIs are broader, including new orders, backlogs of unfilled orders, suppliers’ delivery times (a measure of supply chain pressures) and employment. That is why, for example, the composites for June’s US, UK and eurozone PMIs can be below each of their services and manufacturing PMIs.

Exhibit 1 shows major economies’ PMIs remain above 50—though they are down from the spring, implying deceleration (Japan excepted). The US and eurozone’s June flash composites, released with only 85% – 90% of responses in, fell to the low 50s, continuing a generally slower trend. This includes both services, which comprise the bulk of developed market economies, and manufacturing.[iii] But whilst low-50s PMIs aren’t historically robust, our research shows they generally coincide with pedestrian growth.

Exhibit 1: Major Economy PMIs

Source: FactSet and S&P Global, as of 23/6/2022. Flash PMIs are preliminary estimates based on 85% – 90% of responses.

Also note, the downward trend isn’t global—Japan’s composite PMI rose and the UK’s was flat. Japan’s lift was services-based as COVID restrictions eased there.[iv] Reopening-related boosts helped buoy UK services, too, as more workers returned to the office and patronised surrounding businesses.[v] However, Japanese and UK manufacturing weakened alongside the rest of the developed world as Chinese lockdowns hit global supply chains.[vi]

As a whole, we think the picture here appears mixed. The PMIs indicate business activity growth is less broad-based. But through mid-June at least, the pockets of strength seemingly outnumbered the pockets of weakness. Whether that translates to actual economic growth, we will see when output data roll in.

For many, this perhaps isn’t exactly consoling. As we wrote in early June for the eurozone, there are some discrepancies between soft survey data and hard sales and volume data, with some signs of contraction in the latter. In the US and UK, May retail sales fell -0.3% m/m (unadjusted for inflation) and -0.5% (inflation-adjusted), respectively.[vii] But we don’t think this is conclusive, as it may reflect a continuing shift back to services spending from goods—a return to normal, not necessarily weakness, in our view. Hard services data tend to lag, which is why we think timelier PMIs are helpful and looking at both provides a fuller picture, if only in broad brushstrokes.

For now, we are inclined to interpret PMIs as suggesting economies aren’t uniformly weak despite well-documented struggles. Yet we do think the apparent weak points are worth monitoring. Deteriorating new orders may suggest demand is faltering—but it is too early to tell, in our view. Relative services strength may be fading, but in our view, whether that is normalisation following the initial reopening boom or something worse—e.g., cost of living pressures taking a more lasting toll—remains to be seen. Meanwhile, manufacturing’s downtrend, beset by component shortages, could reverse as supply chains recover. Some businesses, particularly in the American consumer world, apparently overstocked trying to compensate amidst surging goods demand.[viii] They may just have inventory overhangs they need to work through—a more temporary hiccough than needing to get lean to correct prior excess.

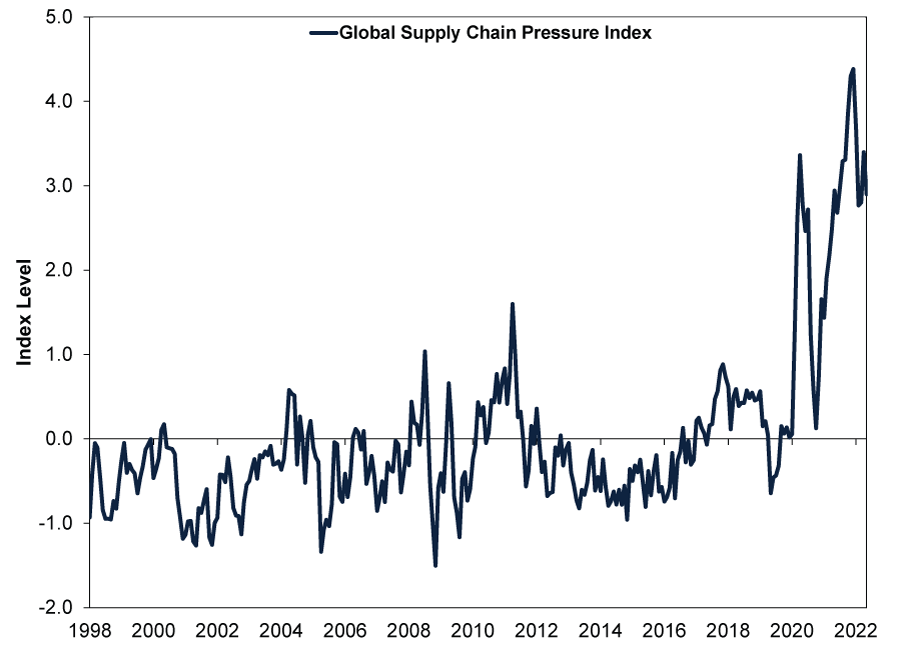

We also see some other encouraging nuggets. The PMI surveys indicate falling backorders, which could be signalling easing supply chain and price pressures. This may be occurring as headwinds from China’s choppy reopening fade. One hint: The New York Federal Reserve branch’s Global Supply Chain Pressure Index, which aggregates transportation costs, input-output prices and other measures—like PMIs’ delivery times, backlogs and inventories—to gauge the overall intensity of bottlenecks’ disruption on world trade. (Exhibit 2) Whilst it remains at lofty levels, it has started subsiding and may be past its peak.

Exhibit 2: Global Supply Chain Pressures Elevated, but Easing

Source: Federal Reserve Bank of New York, as of 18/5/2022. Global Supply Chain Pressure Index, January 1998 – May 2022.

For investors, the most salient aspect of the latest PMI releases may be their accompanying gloomy sentiment. Given the market environment, it isn’t surprising, in our view. But we still think it is notable that PMI coverage from commentators we follow widely extrapolates imminent recession—which the data don’t universally confirm, at least yet, particularly in America. Indicators are mixed. But mixed isn’t necessarily negative. Whilst recession is possible, we think the global economy’s resilience is just as remarkable given the challenges it has faced year to date. This is an underappreciated positive to us.

We think recession uncertainty has undoubtedly weighed on markets lately.[ix] But by the same token, it lowers the bar reality needs to clear to surprise stocks positively, in our view. We think increasing economic clarity in the second half—even if it just muddles through—will likely provide relief.

[i] Source: FactSet and S&P Global, as of 23/6/2022. Flash PMIs are preliminary estimates based on 85% – 90% of responses. A recession is a decline in broad economic output.

[ii] Source: FactSet, as of 27/6/2022. Statement based on MSCI World Index return with net dividends in GBP, 31/12/2021 – 24/6/2022.

[iii] Source: World Bank, as of 28/6/2022. Statement based on services, value added as a percentage of GDP, for eurozone (66.4% as of 2020), UK (72.8% as of 2020), the United States (77.3% as of 2019) and Japan (69.3% as of 2019).

[iv] “Japan to Start Reopening to Foreign Tourists From June 10,” Isabel Reynolds, Bloomberg, 26/5/2022. Accessed through Yahoo! Finance.

[v] “Thursday the New Friday as UK Returns to Office for ‘Core’ Midweek Days,” Joanna Partridge, The Guardian, 24/5/2022.

[vi] “China’s Covid Lockdowns Are Hitting More Than Just Shanghai and Beijing,” Evelyn Cheng, CNBC, 5/5/2022.

[vii] Source: FactSet, as of 24/6/2022. US and UK retail sales, May 2022.

[viii] “Target Is Ramping Up Discounts. Here’s Why,” Nathaniel Meyersohn, CNN Business, 7/6/2022.

[ix] Source: FactSet, as of 27/6/2022. Statement based on MSCI World Index return with net dividends in GBP, 31/12/2021 – 24/6/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis A Market-Orientated Perspective on the EU’s Low Summertime Gas Storage Levels2026-08-03

-

Economics On Fires and GDP2026-07-31

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Market Analysis Quick Hit: Durably Broad-Based US Growth2026-07-29

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today