Personal Wealth Management / Market Analysis

The Low-Down on Q1’s US GDP Downtick

A look beneath the surface at US Q1 gross domestic product and economic developments since.

Editors’ Note: MarketMinder Europe doesn’t make individual security recommendations. Any stock mentioned herein is merely incidental to the broader topic we aim to highlight.

Thursday morning, the US Bureau of Economic Analysis (BEA) released the advance estimate of US Q1 2022 gross domestic product (GDP, a government-produced measure of economic activity), which contracted -1.4% annualised.[i] Coming against expectations of 1.1% growth and amidst widespread recession fears amongst financial commentators we follow, this result likely surprises many and may add to what we perceive to be widespread recession worries.[ii] Yet under the surface, we find little here surprising—or troubling for stocks. Let us show you.

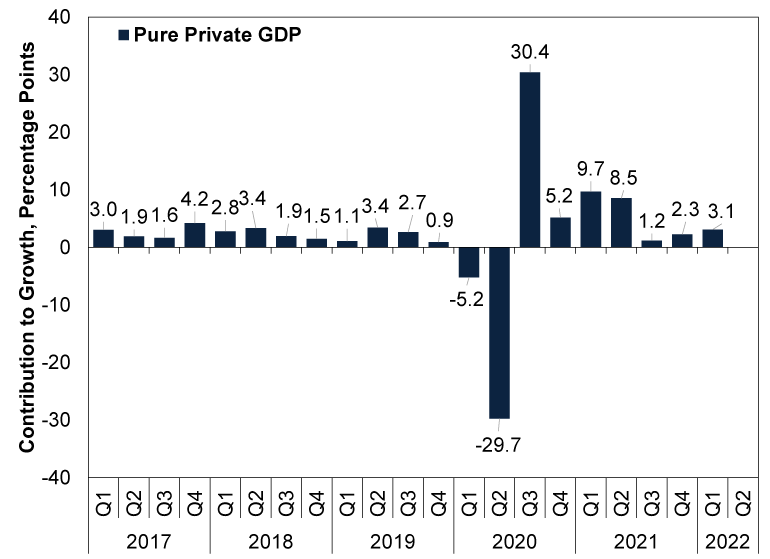

First, consider the details. The purely private-sector GDP components—consumer spending and investment in non-residential structures, equipment, intellectual property and housing—rose and accelerated from Q4 2021, when headline GDP grew 6.9% annualised. (Exhibit 1)

Exhibit 1: Contributions to Growth From Pure Private-Sector Components

Source: BEA, as of 28/4/2022. Q1 2017 – Q1 2022.

How did these broad categories, which total 86.7% of US GDP, accelerate whilst headline growth contracted?[iii] Vast business investment in inventories, which added more than five percentage points to headline growth in Q4 2021, skewed that quarter’s GDP growth rate higher.[iv] We think that was likely firms ploughing capital into rebuilding inventories and in anticipation of continued supply chain issues. In Q1 2022, that fell off a cliff, with inventory change subtracting -0.84 point, meaning there was more than a six percentage point swing from this one tiny category of the US economy.[v] A reversal in inventory changes’ contribution shouldn’t surprise—nor is a decline in inventory change necessarily bad, in our view. We think it may actually help quell one rather realistic economic concern we have monitored lately: That firms would over-invest in inventory, only to see demand falter and leave them with excess, driving down pricing. That rather traditional recession recipe doesn’t seem to be materialising in the data after Q1’s release, in our view. Rather, we think it looks like strong demand ran down stockpiles a bit.

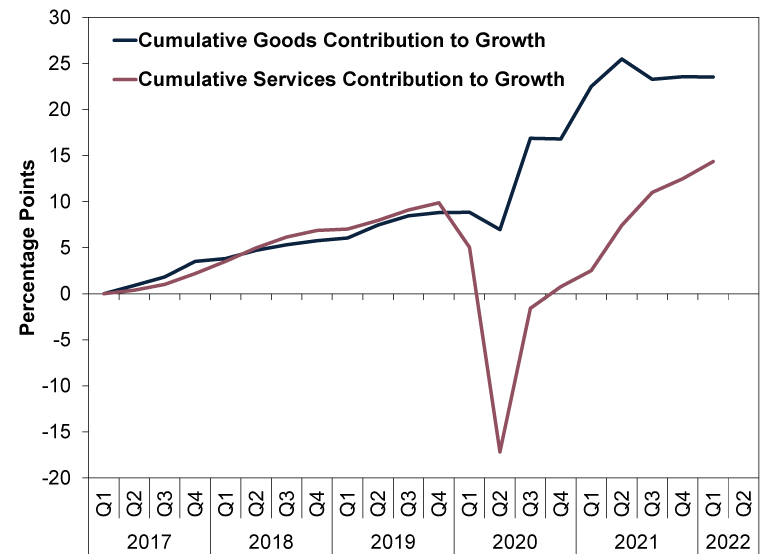

Beyond inventories, government spending also fell -2.7% annualised, detracting -0.48 point from headline growth, largely because some pandemic-related relief spending dried up.[vi] But this, too, shouldn’t shock many observers, in our view: Such measures were always going to end and, like inventory change, one can debate whether a bigger or smaller contribution from government consumption is economically good or bad. And, the other unsurprising piece to us: Whilst consumer spending overall grew 2.7% annualised, adding 1.83 points to headline growth, goods spending was flat whilst services boomed 4.1% higher.[vii] Note that these figures are inflation-adjusted—not boosted artificially by high prices.

This pattern, which we have long thought likely tied to lifting COVID restrictions and pent-up demand for things like travel, echoes corporate executives’ commentary and data from corporate earnings conference calls. In the last two days, payment technology firms Visa and Mastercard both reported resurgent overseas transaction volumes, suggesting travel is making a comeback.[viii] In its filing Tuesday, Google’s parent company, Alphabet, reported search volumes related to travel are also up.[ix]

You can see this goods-versus-services flip flop in Exhibit 2, which plots the cumulative contribution to growth from services and goods spending over the past five years. As shown, services spending—even now almost twice as large as goods spending—absolutely tanked in the pandemic whilst goods consumption soared after a brief blip.[x] We think this likely pulled some goods demand forward, which may explain the slow growth now, whilst services spending advances.

Exhibit 2: Services Versus Goods Spending

Source: BEA, as of 28/4/2022. Cumulative contributions to growth, Q1 2017 – Q1 2022.

Lastly, imports vastly outweighed exports.[xi] Imports are subtracted from headline GDP, a means used by the BEA and other national statistical bodies to offset their inclusion in other categories, like spending, and thereby give a better read of one nation’s economic activity.

Beyond this, we think it may also be worth noting that US Q1 GDP data have a more than 40-year history of downward skew tied to issues with seasonal adjustment—issues that have grown rather than shrunk in recent years.[xii] (Seasonal adjustment is an economic modelling approach that aims to smooth out repeat, calendar-related impacts on growth, like the typical holiday-related spending surge in Q4, following by a crash in Q1.) This is a well-documented phenomenon in the economics community, which the BEA has attempted to identify and fix more than once.[xiii] Now, perhaps they have fixed the adjustment, but we doubt it. Our review of economic data over the past two years shows pandemic-related skew has wreaked havoc on seasonal adjustment factors used in an array of series from new claims for unemployment insurance to GDP and more. We don’t think this fully erases the contraction, of course. But we think it should be a cautionary tale for those drawing huge, forward-looking conclusions from it.

That said, Q1 ended 29 days ago, so one may wonder what the economy’s state is since. We don’t have many formal data points to rely on just yet, beyond preliminary purchasing managers’ indexes—surveys tallying the breadth of growth across the economy—which point to fairly healthy US economic activity.[xiv] These gauges don’t tell you anything about the magnitude of growth, though—just its breadth. But we think less-traditional measures of activity reveal some signs of expansion continuing. Take, for example, these:

- Restaurant reservation service OpenTable’s data show seated diners at US restaurants spent most of this month hovering around April 2019 levels, continuing a recovery to pre-pandemic levels of activity.[xv]

- Through April’s first 27 days, America’s Transportation Security Administration reports 57,025,545 passengers have passed through security at America’s airports—53.4% above the comparable period last year and just -9.6% below 2019 levels.[xvi]

- In the week of April 17 – 23, US hotel occupancy was at 65.8%, down just -4.2% from 2019’s pre-pandemic period. That is despite average daily hotel rates rising 15.4% over this span.[xvii]

- Goods shipping via train is a little soft, according to the American Association of Railroads, averaging -4.8% y/y in April’s four weekly reports to date.[xviii] But we think that seemingly echoes the services-versus-goods split above all else.

- Meanwhile, in the Energy sector, April 22’s oil services firm Baker Hughes’ tally of US rigs actively drilling for oil and gas rose 59% y/y.[xix]

Now, take these data with a grain of salt. We think they are limited, they aren’t seasonally adjusted and base effects (year-over-year calculations skewed by outlying results 12 months ago) could skew them. But they don’t really suggest to us economic activity has fallen off a cliff this month. We would suggest that the preponderance of the evidence suggests Q1 GDP’s small contraction isn’t a harbinger of bigger trouble ahead. We think that is doubly true when you consider the US Leading Economic Index, a composite of 10 mostly forward-looking indicators that has fallen for months before nearly every US postwar recession, rose 0.3% m/m in March and 0.6% in February, extending an uptrend.[xx] That suggests to us a recession isn’t likely in the offing now.

It wouldn’t surprise us if Q1’s contraction served a different purpose: Allowing bearish financial commentators to see their warnings as having come true—and move on. In our experience, that is rather typical correction behaviour, and it can be key to sentiment morphing. Only time will tell if that holds now, but we suspect it may partly explain why stocks surged after the data dropped.[xxi]

[i] Source: BEA, as of 28/4/2022. The annualised growth rate is the rate at which GDP would grow or contract over a full year if the quarter-on-quarter growth rate persisted all four quarters.

[ii] Source: FactSet, as of 28/4/2022. Consensus broker estimates for Q1 2022 US GDP growth.

[iii] See note i.

[iv] Ibid.

[v] Ibid.

[vi] Ibid. Statement regarding government assistance based on commentary in BEA press release, “Gross Domestic Product, First Quarter 2022 (Advance Estimate), 28/4/2022.

[vii] Ibid.

[viii] Source: FactSet, company filings, as of 28/4/2022.

[ix] Ibid.

[x] Source: BEA, as of 28/4/2022.

[xi] Ibid.

[xii] “Assessing Residual Seasonality in the U.S. National Income and Product Account Aggregates,” Baoline Chen, Tucker S. McElroy and Osbert C. Pang, BEA Working Paper Series, January 2021.

[xiii] “Why Is the Economy Always So Weak in the First Quarter? Nobody Really Knows,” Steve Liesman, CNBC, 22/4/2015.

[xiv] Statement based on S&P Global’s Flash US Composite PMI for April.

[xv] Source: OpenTable, as of 28/4/2022. Seated diners from online, phone and walk-in reservations, April 2022 levels are year-over-three-year growth rates to illustrate the change since pre-pandemic rates.

[xvi] Source: TSA, as of 28/4/2022.

[xvii] Source: STR, as of 28/4/2022.

[xviii] Source: FactSet, as of 28/4/2022.

[xix] Ibid.

[xx] Source: The Conference Board, as of 28/4/2022.

[xxi] Source: FactSet, as of 28/4/2022. Statement based on the S&P 500 price index, which rose 2.5% in USD on 28/4/2022. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-02

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

-

Market Analysis Reviewing America’s Q1 Earnings and What Q2 Expectations Say2026-06-23

-

Politics Revolving Door Turns, Uncertainty Starts Falling2026-06-23

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today