Personal Wealth Management / Economics

US Q1 GDP Better Than Commentators We Follow Appreciate

We find strong private sector demand belies the headline slowdown.

Although US gross domestic product (GDP, governments’ measure of economic output) rose 1.1% annualised in Q1, it missed consensus expectations for around 2%.[i] Commentators we follow widely proclaim this slowdown is—at long last—a prelude to the recession (broad-based decline in economic activity) they have forecast for quarter after quarter now. But we find a look under the bonnet reveals underappreciated private sector resilience—the very fuel that we think has propelled global stocks in their recovery.[ii] Whilst these data are all backward looking, we think it shows sentiment surrounding economic growth remains excessively dire, which we find is often the case as bull markets (prolonged periods of rising equity prices) begin.

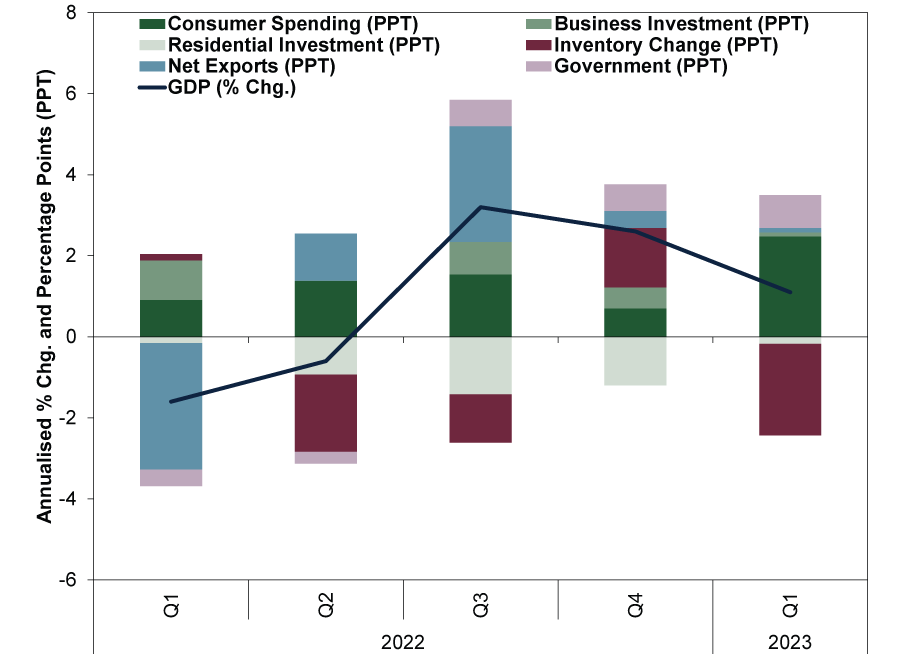

Overall GDP growth rates frequently obscure moving parts below the surface—movement that we find can tell you much more about the economy than the headline number alone. Hence, we think it helps to look at GDP’s underlying components to put growth trends in context. As Exhibit 1 shows, inventory change (maroon) was the main detractor in Q1, lopping a large -2.3 percentage points (ppts) off headline GDP growth—the most since Q1 2021’s drawdown as US goods consumption surged.[iii] For some broader perspective, consider: In the 120 quarters from Q1 1990 to Q4 2019—the eve of the pandemic—inventory change detracted more than this just 4 times.[iv]

Exhibit 1: US GDP’s Combined Private Sector Demand Components Accelerated

Source: US Bureau of Economic Analysis (BEA), as of 28/4/2023. Real GDP and components, Q1 2022 – Q1 2023.

Declining inventories are open to interpretation—they aren’t automatically negative, in our view. They can fall because businesses can’t keep up with demand or because they might be anticipating less demand ahead. In our view, given widespread recession expectations, companies appear to be cutting fat this time around, getting lean and mean to weather potentially harder times ahead.

But we see an upside to this: Based on our analysis, pre-emptive stockpile reduction would mean the economy is working off excess before an overall economic contraction, sapping much of a recession’s purpose—wringing out bloat. Such advanced preparation suggests to us that if a US recession comes, it would likely be quite mild. Also note, the big inventory decline in Q2 last year caused headline US GDP to dip negative after Q1 2022’s trade-driven decline—yet recession didn’t ensue. The reason: GDP’s main private sector demand components were positive throughout.

Go back to Exhibit 1. We consider consumer spending (dark green), business investment (light green) and residential investment (mint) better measures of private-sector activity in GDP—together, they best approximate the economy’s core drivers. Inventory change, net exports (exports minus imports, blue) and government spending (purple) feed into GDP, but our research shows they tend to be less indicative of economic trends. For instance, we find more government spending isn’t always good.

As for the other components, only residential investment fell. But this isn’t a new trend. It has tanked over the past year as new home sales shrivelled with mortgage rates’ spike.[v] Note, however, even with big detractions in Q2 – Q4 2022, consumer spending and business investment (green bars) offset it, though barely in Q4. In Q1, residential investment shrank for an eighth straight quarter, but with mortgage rates easing—and new home sales picking up—it sliced off only -0.2 ppt.[vi] Housing markets seem to us like they are stabilising.

Meanwhile, US consumer spending accelerated strongly in Q1 to 3.7% annualised from Q4’s 1.0%, contributing 2.5 ppts to headline GDP—the most since Q2 2021’s reopening-driven consumption surge.[vii] Notably, goods expenditures grew for the first time after declining slightly for four consecutive quarters.[viii] Services spending also continued chugging along, as it has since the last recession ended in Q2 2020—and looks likely to keep going in Q2 2023 as well.[ix]

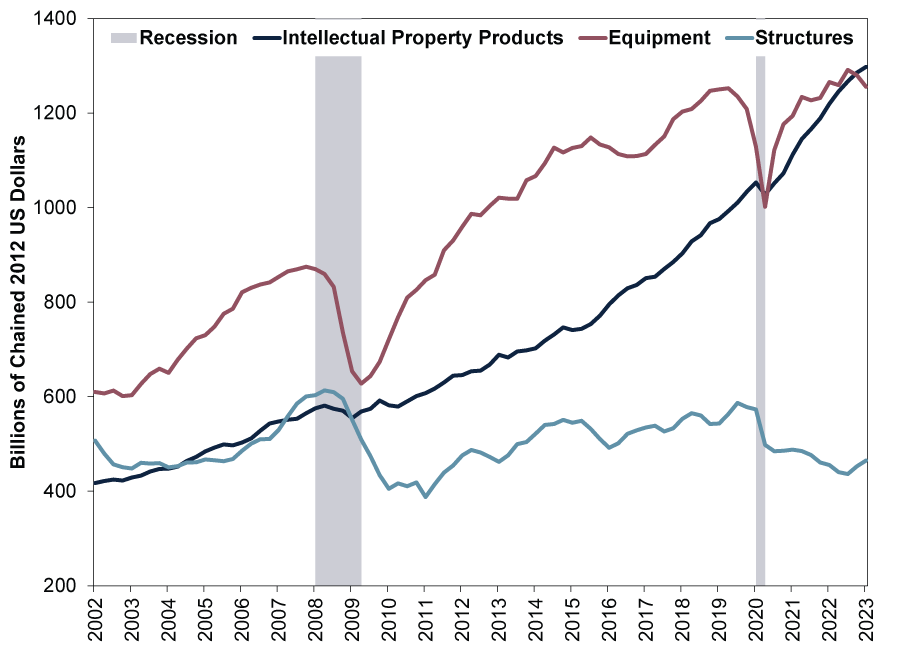

America’s Q1 business investment was more mixed. Equipment spending tumbled -7.3% annualised in Q1, worsening from Q4’s -3.5% decline.[x] This wasn’t too surprising to us, as monthly reports on capital goods orders and shipments implied a drop.[xi] Interestingly, though, equipment is no longer the US’s biggest category within business investment. Exhibit 2 shows intellectual property products—think: software, research and development, media and entertainment—overtook equipment in Q4 last year for the first time (outside 2020’s lockdown recession). They kept climbing in Q1.

Exhibit 2: Software Overtaking Hardware in America

Source: Federal Reserve Bank of St. Louis, as of 28/4/2023. Real non-residential investment in intellectual property products, equipment and structures, Q1 2002 – Q1 2023.

Whilst it is too early to tell whether a further pullback in equipment leads to a down cycle, we think intellectual property investment’s continuing rise points to a progressively bigger counterweight. It isn’t a secret digital products’ and services’ share of GDP is growing.[xii] We observe this to be a long-running trend in the economy’s evolution. People have been calling it the Information Age for decades, after all.[xiii] Intellectual property investment’s ascendance is just one manifestation of that, in our view.

All of this is, of course, backward-looking. It doesn’t preclude a recession in the future, even if it means the US wasn’t in one last quarter—despite dour projections from commentators we follow. But even if we do get GDP contractions ahead, it is worth remembering a simple point, in our view: Markets look forward. We think they pre-price widely known risks and forecasts. Those commentators’ ubiquitous recession forecasts that seem to continually shift six months forward when GDP data undercut them suggest to us that, if we get one any time soon, it isn’t likely to shock stocks.

[i] Source: FactSet, as of 28/4/2023. US GDP and FactSet consensus estimate, Q1 2023. Annualised growth is one quarter’s growth if repeated for a year.

[ii] Source: FactSet, as of 28/4/2023. Statement based on MSCI World Index returns with net dividends, 16/6/2022 – 28/4/2023.

[iii] Source: FactSet, as of 28/4/2023. Statement based on US personal consumption expenditures and inventory change, Q1 2021.

[iv] Source: US Bureau of Economic Analysis, as of 28/4/2023. It has done so twice since the pandemic, which speaks to the vast disruptions lockdowns wrought on supply chains.

[v] Source: FactSet, as of 28/4/2023. Statement based on US residential investment, Q1 2022 – Q1 2023, US new home sales, January 2022 – March 2023, and US 30-year fixed mortgage rates 1/1/2022 – 31/3/2023.

[vi] Ibid.

[vii] Source: FactSet, as of 28/4/2023. Statement based on US personal consumption expenditures, Q2 2021 – Q1 2023.

[viii] Source: FactSet, as of 28/4/2023. Statement based on US goods personal consumption expenditures, Q1 2022 – Q1 2023.

[ix] Source: FactSet, as of 28/4/2023. Statement based on US services personal consumption expenditures, Q2 2020 – Q1 2023.

[x] Source: FactSet, as of 28/4/2023. US non-residential fixed investment, Q2 2020 – Q1 2023.

[xi] Source: Federal Reserve Bank of St. Louis, as of 28/4/2023. Statement based on US durable goods orders, January 2023 – March 2023.

[xii] Source: Federal Reserve Bank of St. Louis, as of 28/4/2023. Statement based on non-residential investment in intellectual property products versus equipment, Q1 2002 – Q1 2023.

[xiii] “How Claude Shannon Invented the Future,” David Tse, Quanta Magazine, 22/12/2020.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights The Danger of Chasing Investor Flows2026-08-05

-

Market Analysis A Market-Orientated Perspective on the EU’s Low Summertime Gas Storage Levels2026-08-03

-

Economics On Fires and GDP2026-07-31

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today