Personal Wealth Management / Financial Planning

Why We Think Fixed Interest Still Make Sense in a Low-Yield World

Fixed interest can still fulfill its role in an investment portfolio, in our view.

Around the developed world, from sovereign debt to corporate, fixed interest security yields are historically low.[i] That has many financial commentators we follow asking: Why hold them at all? In our view, fixed interest’s primary purpose is to dampen portfolio volatility to mitigate swings for those needing to draw cash flow. Yes, yields today are miniscule, but we think fixed interest securities’ ability to cushion against short-term volatility endures—and makes a compelling case for them, should your goals, needs and risk tolerance make smaller swings optimal.

On 4 August, 10-year gilt yields dropped to a record-low 0.07%, and they have hovered below 0.3% since.[ii] Meanwhile, corporate fixed interest yields have also fallen to record-low levels.[iii] Both are well below their averages over the past decade (2.0% for 10-year UK gilts, 3.7% for corporates), a period when we observed many commentators also complaining about yields being too low.[iv] Yet even then, investors could take on a bit more credit risk, buy corporate debt securities with still-low default probabilities and earn positive returns even after accounting for inflation.[v] Not hugely so, but still positive. Now, some commentators say this refuge is dwindling.

Yet we don’t think record-low interest rates mean fixed interest securities play no role in portfolios today for those who need cash flow. Our research shows they tend to fluctuate less than equities in the short term—a vitally important point for these investors to weigh, in our view. If your long-term financial goals require a relatively high rate of cash flow—and after taking into account your other needs, risk tolerance and time horizon (the length of time your assets need to be invested to meet your needs)—we think a blend of equities and fixed interest can be very beneficial. Though portfolio income—interest or dividends—can help fund withdrawals, making equity sales is frequently a more reliable means of providing for cash flow needs. With this in mind, the combination of price movement and income—total return—is what matters most, in our view.

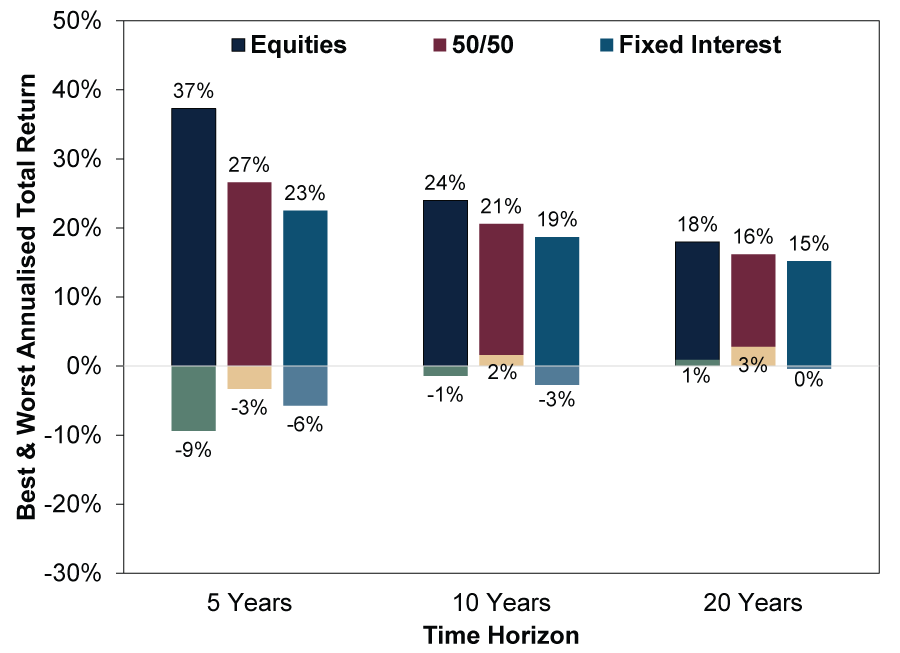

Because equities’ short-term returns can vary greatly, our research shows regular withdrawals at relatively high rates from an all-equity portfolio could risk unwanted portfolio depletion if you hit a stretch of subpar equity market returns or down years. Including fixed interest—regardless of their yield—helps mitigate this risk, in our view. UK gilts’ standard deviation (a measure of volatility that represents the degrees of fluctuations in historical returns) over rolling five-year periods since 1925 shows this stabilising effect. Ten-year gilts’ standard deviation is 5.5%, which means over any five-year timeframe, including the most extreme within the last century, their annualised total return was usually within plus or minus 5.5 percentage points of their 6.3% average.[vi] (Exhibit 1)

Exhibit 1: Fixed Interest Can Dampen Volatility in the Short Term

Source: Global Financial Data, Inc., as of 15/12/2020. Developed World Return Index and UK 10-Year Government Bond Total Return Index, annualised total returns over rolling 5-, 10- and 20-year periods, December 1925 – October 2020.

In contrast, equities’ standard deviation over rolling five-year periods is higher: 8.0%.[vii] Though equities’ annualised total return is higher—10.3%— the greater variability around that implies more short-term volatility.[viii] So while fixed interest security prices can fall a bit, it has happened less often, and by smaller magnitudes, than shares, based on our research. Hence, we think fixed interest’s principal role is to smooth out returns, raising the likelihood your portfolio can provide cash flow throughout your time horizon even under historically bad circumstances.

We have observed some financial analysts argue now is different, presuming record-low rates are an anomaly that must reverse quickly as the economy moves on from the pandemic. Since debt yields move inversely to prices, rising rates mean falling debt prices. This is true to an extent, but we think careful management of your fixed interest positioning can mitigate this risk, which is where managing for total return again comes in handy. Fixed interest securities come in different maturities—the period of time in which they make interest payments before the issuer repays principal. Although rates are low across the board, shorter maturity fixed interest securities still aren’t as susceptible to rising rates based on our research. If you expect rates to rise (and your reasoning isn’t widely shared, as we think markets reflect widely known information), we think you can mitigate the impact on your total return by reducing your fixed interest portfolio’s duration (how much prices move for a given change in yield). Also, shorter-term corporate debt yields a bit more than similar-maturity gilts, which we think provides some insulation from rising rates. Corporate debt securities also have other drivers beyond government interest rates. If the economy heals and that drives government rates up, rising profitability may mean corporate rates rise by a smaller amount.

Note, we aren’t saying the time to brace for major change is now. In our view, it isn’t clear big rate increases are around the corner. Interest rates are sensitive to inflation expectations, so it is worth considering what might cause inflation to surge. The UK’s consumer price index appears set to rise somewhat in early 2021 from November’s 0.3% y/y.[ix] But this is tied mostly to base effects from falling prices in March and April 2020, which skew the denominator in the year-over-year calculation. We think markets, as efficient discounters of information, are generally good at seeing through such calculation quirks. Beyond that, whether price acceleration lasts is an open question. As the economy recovers and commerce speeds up, some further rise in prices wouldn’t be shocking.

The question for fixed interest positioning is the degree to which prices rise, in our view. Thus far, we have seen few signs the Bank of England and other monetary institutions globally are letting up on their quantitative easing asset purchases. Around the world, they have been snapping up long-term sovereign debt, which helps push their prices up and keeps yields low. That flattens yield curves (graphical representations of a single issuer’s rates across the spectrum of maturities)—which a host of research shows weighs on rising prices, in our view. Then too, even if materially higher inflation is coming, it is unlikely to be overnight—enough time, in our view, to adjust how your fixed-interest allocation is invested.

Overall, fixed interest returns may not be great, but we think they can still mitigate volatility, which can be critical for meeting your anticipated funding needs depending on your specific situation.

[i] Source: FactSet, as of 16/12/2020.

[ii] Source: FactSet, as of 15/12/2020. 10-year UK government gilt yield, 4/8/2020.

[iii] Ibid, as of 15/12/2020. Statement based on yield to maturity as measured by Bloomberg Barclays Sterling Aggregate Non-Gilts – Corporate Index, 14/12/2020.

[iv] Ibid. 10-year gilt and Bloomberg Barclays Sterling Aggregate Non-Gilts – Corporate Index yield average, 31/12/2009 – 31/12/2019.

[v] Source: FactSet, as of 16/12/2020. Statement based on average annual yield of Bloomberg Barclays Sterling Aggregate Non-Gilts – Corporate Index compared to average annual percent change in UK consumer prices, 2009 – 2019.

[vi] Source: Global Financial Data, Inc., as of 15/12/2020. 10-Year UK Government Bond Index annualized total returns, rolling 5-year periods, December 1925 – November 2020.

[vii] Ibid. GFD Developed World Return Index annualized total returns, rolling 5-year periods, December 1925 – October 2020.

[viii] Ibid.

[ix] Source: FactSet, as of 16/12/2020. UK CPI, year-over-year percent change, November 2020.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics France’s Budget Finally Forced Forward2026-02-12

-

Macro Insights Q4 2025 Global Markets Review & Outlook2026-02-10

-

Market Analysis Don’t Sweat the Rate Hike Down Under2026-02-10

-

In The News Dour economists are missing these major growth signals2026-01-27

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today