Personal Wealth Management / Economics

$100+ Oil Isn’t a Tipping Point

Why surging fuel costs can hurt your pocketbook, but not the economy.

With the tragic events unfolding in Ukraine right now, financial market and budget impacts may seem small in comparison. Nevertheless, the conflict and the international community’s response have spurred oil prices to climb, and with them, gasoline prices—a real financial concern to many Americans as oil sits above $100 and some outlets forecast the national average gas price will soon hit $5 per gallon. As we wrote a few weeks ago, oil’s latest spike seems mostly sentiment-driven, and longer-term supply and demand drivers still suggest prices should stabilize sooner rather than later, even with uncertainty surrounding Russian oil supply roiling markets. However, some pundits speculate elevated oil prices will tip the economy into recession. While oil’s record prices did coincide with 2008 – 2009’s recession, coincidence isn’t causality. Oil’s hitting any level has no direct bearing on broader economic activity. Oil’s rise and recent surge don’t automatically foretell weaker growth.

The US economy doesn’t have a set relationship with oil prices. When oil spent much of 2011 – 2014 above $100, no recession ensued. Conversely, while high oil coincided with recession in 2008 – 2009, the issue then was mark-to-market accounting rules’ incinerating bank capital unnecessarily and the government’s haphazard, panic-sowing response—not oil. Counterintuitively, falling oil prices created a US economic headwind in the last decade. When oil prices collapsed in 2014, it caused US producers to cut back. One of the largest GDP detractors over the next two years was oilfield machinery investment. In 2015’s second half, it caused GDP’s sharp slowdown. Higher oil prices have the opposite effect on GDP, incentivizing more investment.

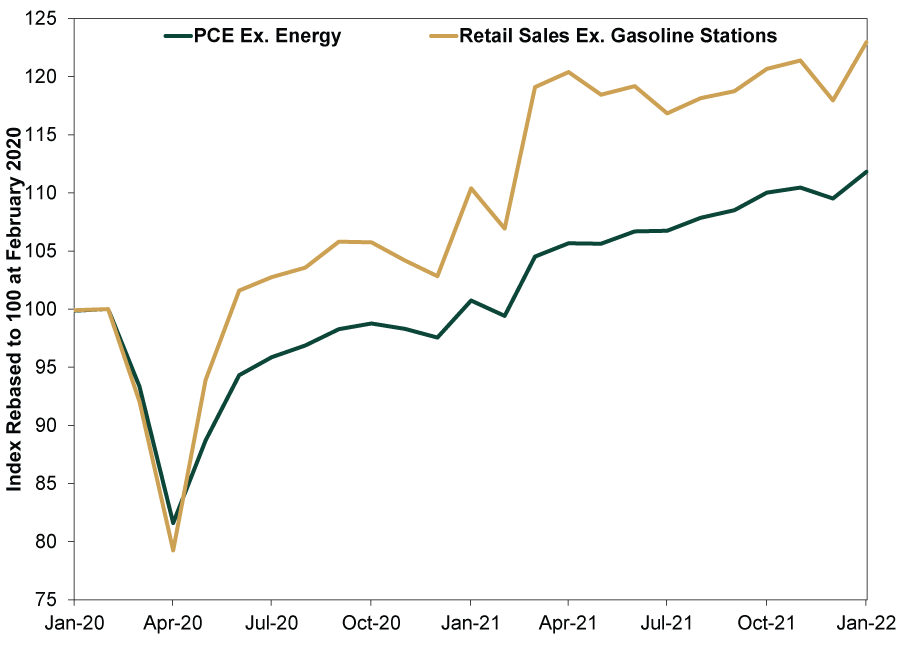

Second, the popular reason why oil allegedly dictates the economy’s direction is flawed. High oil prices hit households in the pocketbook, diverting consumer spending from more fun destinations—but from an overall economic perspective, fuel costs still count as spending. That means they contribute positively to GDP. Not that GDP is the be-all, end-all, but it shows casting high oil prices as an automatic economic negative isn’t accurate. High gasoline prices create winners and losers within consumer spending and can shift activity, but non-fuel spending is pretty resilient. Exhibit 1 shows personal consumption expenditures (PCE) excluding energy and retail sales excluding gasoline stations (a narrower measure focused on goods). They hit record highs in January, even with oil’s climb to $89 that month from $48 per barrel starting 2021.[i]

Exhibit 1: Higher Oil Isn’t Bothering Consumer Spending

Source: Federal Reserve Bank of St. Louis, as of 3/14/2022. PCE excluding energy and retail sales excluding gasoline stations, January 2020 – January 2022.

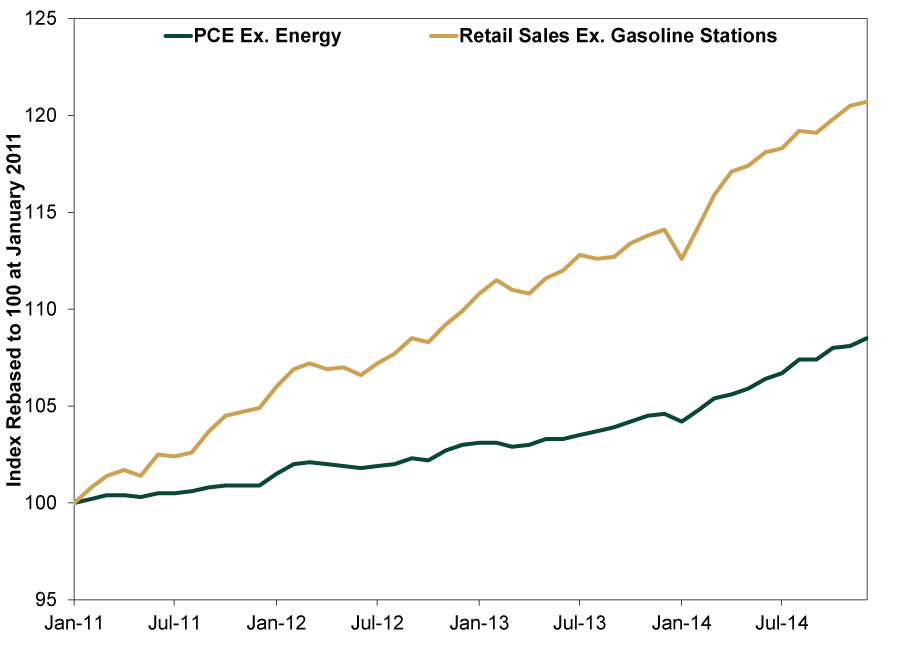

Exhibit 2 shows how these series behaved the last time oil prices rose above $100 per barrel. On February 1, 2011, WTI crude hit $100.40 and stayed mostly above that until oil’s collapse in September 2014, rising as high as $128.14 on March 13, 2012.[ii] Consumer spending excluding energy and non-gas retail sales hardly skipped a beat.

Exhibit 2: It Didn’t When Oil Was Last Over $100

Source: Federal Reserve Bank of St. Louis, as of 3/14/2022. PCE excluding energy and retail sales excluding gasoline stations, January 2011 – December 2014.

This looks only at consumption—what about higher costs for producers? Oil (crude and refined products) comprised only 9% of producer prices in December, up from December 2020’s 7%, but the same level as December 2019, before COVID crushed oil prices.[iii] Oil isn’t to be discounted, but it is equally mistaken to overrate the effect.

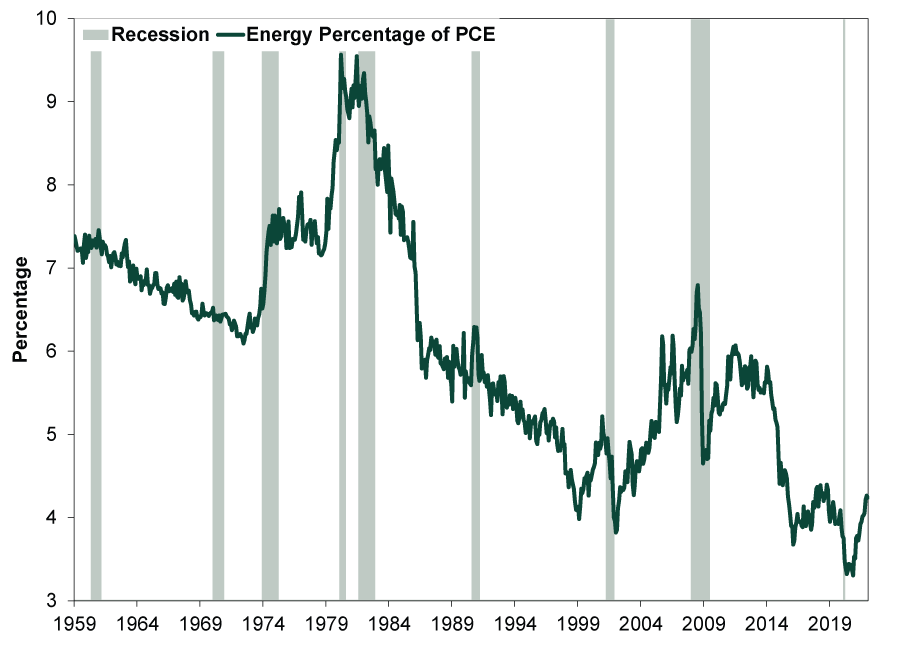

Third, a big reason why oil isn’t hampering growth: The economy is less energy-dependent than it was in decades past. While rising fuel costs aren’t great, energy’s share of consumer spending—which is over two-thirds of GDP—has fallen. (Exhibit 3) In January, energy consumption amounted to 4% of PCE. This is up a percentage point from 2020’s lockdown lows, but it is basically hovering around pre-COVID levels presently. It is still well below 2011 – 2014 levels, when oil last traded around current prices, so maybe it rises further still. But again, oil prices didn’t drive an economic contraction then. It is also still around half late-1970s’ and early-1980s’ levels many pundits invoke when arguing oil will drive a recession.

Exhibit 3: Energy Consumption Still a Teeny Part of Consumer Spending

Source: Federal Reserve Bank of St. Louis, as of 3/14/2022. Energy PCE as a percentage of PCE, January 1959 – January 2022.

As Fisher Investments’ founder and Executive Chairman Ken Fisher wrote recently, developments in Europe—which is the swing factor pertaining to oil supply—are worth watching. But, as he noted, they aren’t worth overrating, either. There is little reason to think oil hovering near where it was during an expansion eight-ish years ago is automatically troubling today.

[i] Source: FactSet, as of 3/14/2022. WTI crude oil price per barrel, 12/31/2020 – 1/31/2022.

[ii] Ibid. WTI crude oil price per barrel, 2/1/2011 – 9/4/2014.

[iii] Source: US Bureau of Labor Statistics, as of 2/25/2022. Relative importance of commodities included in the Producer Price Index, all levels, December 2019 – December 2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today