Personal Wealth Management / Economics

A Look at the Range of Forecasts Markets Are Anticipating

A wide range of forecasts helps markets digest COVID-19’s economic impact.

On Tuesday, the IMF released its latest World Economic Outlook, which forecasts global growth shrinking -3.0% in 2020, its worst downturn since the Great Depression and a major flip from January’s forecast of 3.3% growth.[i] While stark, this shouldn’t shock. As commentators have documented thoroughly, the sudden halt to economic activity from business closures and social distancing is unprecedented—and likely severe. With data from March rolling in, we are getting a look at just how severe. US retail sales’ -8.7% month-over-month drop was the biggest on record, and industrial production’s -5.4% slide was the worst since 1946.[ii] But these numbers are an incomplete look, considering they encompass only about two weeks of the present lockdowns. Plus, they—and most other figures coming out—are likely imperfect. As some have noted, business closures and outages are complicating economic data collection. However, while the actual data we have are very spotty, there is a huge array of forecasts—which markets see and adjust to. That is partly how they anticipate future conditions. Here is a look at the numbers economists expect—and why whatever end of this spectrum reality lines up with likely matters less than the duration.

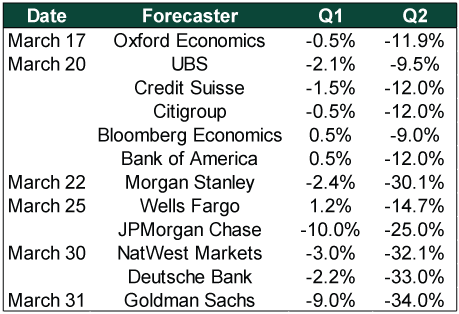

For the US, there is a wide range of economic forecasts. Exhibit 1 shows major financial institutions’ forecasts in the order they released them. For the most part, their Q1 and Q2 GDP estimates go from bad to astonishingly ugly. They also generally worsened toward month end, as COVID-19 caseloads increased and state lockdowns spread.

Exhibit 1: Forecasters’ Q1 and Q2 GDP Estimates

Source: “Economists See U.S. Facing Worst-Ever Quarterly Contraction,” Reade Pickert, Bloomberg, 3/31/2020. Forecasts are for seasonally adjusted annualized GDP growth rates.

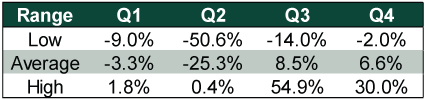

Broadly speaking, as Exhibit 2 shows, economists surveyed by The Wall Street Journal have similar first-half expectations, followed by a rebound in the year’s second half—albeit with wide variations. The timing of lockdowns lifting will likely determine both when we get an economic recovery and how swift it is. That lifting is an unpredictable, non-market-driven event, making GDP much harder for analysts to pin down than usual. That likely explains the wide range in forecasts.

Exhibit 2: Economists’ 2020 Quarterly GDP Estimates

Source: The Wall Street Journal, as of 4/13/2020. Forecasts are for seasonally adjusted annualized GDP growth rates, Q1 2020 – Q4 2020.

While the numbers are huge, note, they aren’t saying GDP will actually fall by a quarter or more in Q2. The Bureau of Economic Analysis reports annualized US GDP growth rates, and that is what analysts are projecting. Annualizing growth rates extrapolates one quarter’s growth rate over an entire year. A hypothetical -26.2% annualized decline is the drop GDP would record if the quarter’s -6.0% quarter-over-quarter growth rate repeated for four quarters (accounting for compounding). For GDP to really fall at that rate over an entire year, closures would likely have to last a year, with intensifying effects on output. That seems like an increasingly unlikely outcome, considering states on the west and east coasts are already forming committees to explore reopening, following Europe’s lead.

The IMF’s forecast for America echoes private economists’ projections. There isn’t a quarterly breakdown, but the IMF expects US GDP to fall -5.9% this year and then rise 4.7% in 2021.[iii] This baseline scenario assumes the pandemic fades and containment measures wind down in the second half. A longer pandemic—and extended closures—could double the economic downside and delay recovery, according to the IMF’s models.

While there is no question these magnitudes are gigantic, the drop’s size is less significant than its duration, as that will determine whether a short-term rebound will help even out full-year results or if a longer downturn is in store. Even with record monthly declines in economic activity, if their duration is short, the resumption in activity can generate big leaps in growth, especially off a low base. This outcome has strong potential if businesses can pick up where they left off after lockdowns end—the supply will be there to meet demand lockdowns temporarily turned off. However, an enduring lockdown would threaten the supply side more. Furloughed workers and temporarily closed stores and offices can pick up more quickly than those who have permanently lost jobs or dissolved their businesses.

Stocks generally look around 3 to 30 months ahead, discounting widely known information, including economic forecasts. Global stocks peaked on February 12. Italy reported its first case on February 20. Lockdowns began there on March 9 and spread throughout continental Europe by March 22. In the US, California was the first state to lock down on March 19, and South Carolina the latest on April 7, with eight states remaining with no (or partial) stay-at-home orders. The first lockdown-affected economic data didn’t roll in until March 24. By then, global stocks had fallen -34.0% from the high through March 23.[iv] Stocks didn’t wait for official clarity—they formed expectations on how bad reality could get in real time.

What happens in Q2 probably matters less for stocks than what happens past it, further into that 3 – 30-month range. Awful results may hit sentiment in the short term, but those near-term hits usually even out as stocks shift focus to the longer term. Stocks have been hyper-focused on the shorter term, in our view, incorporating the many paths the economy could take from here, which makes the likelihood of some major negative surprise in the near term rather low. But as uncertainty falls, possibilities narrow and likely outcomes become clearer, their focus should shift toward the longer term. That is where we think investors should focus now, too.

Ultimately, what matters most likely isn’t how deep GDP plunges in Q1 or Q2. It seems to us how quickly businesses reopen and activity returns to some semblance of normalcy matters more. That seems likely to determine the extent of positive (or negative) surprise in store for stocks over the medium to longer term.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today