Personal Wealth Management / Market Analysis

A Primer on P/Es and This Young Bull Market

Valuations aren’t all they are cracked up to be.

Are stocks worth their price? With the S&P 500 hitting new highs, valuations—price-to-earnings (P/E) ratios in particular—are returning to the headlines. The mission seems to be divining whether stocks are cheap or pricey near record index levels, all with an eye toward projecting markets’ next move. The trouble with this logic? Valuations don’t predict stocks’ direction. Cheap stocks can always get cheaper and seemingly pricey stocks pricier.

Most focus lately is on forward P/Es—based on analysts’ next 12-month earnings estimates—which we think makes more sense than using trailing 12-month earnings. Investors own stocks for their share of the future profits firms are likely to generate. You can’t buy past earnings—they are already priced in. Note here, too, that the Cyclically Adjusted P/E (CAPE) ratio, which averages the last 10 years’ earnings—and then bizarrely inflation adjusts that ‘E’ in comparison to the non-inflation-adjusted ‘P’—makes even less sense in this regard. The profits you earn from owning stock aren’t inflation-adjusted—they are regular dollars—and they aren’t averaged over 10 years.

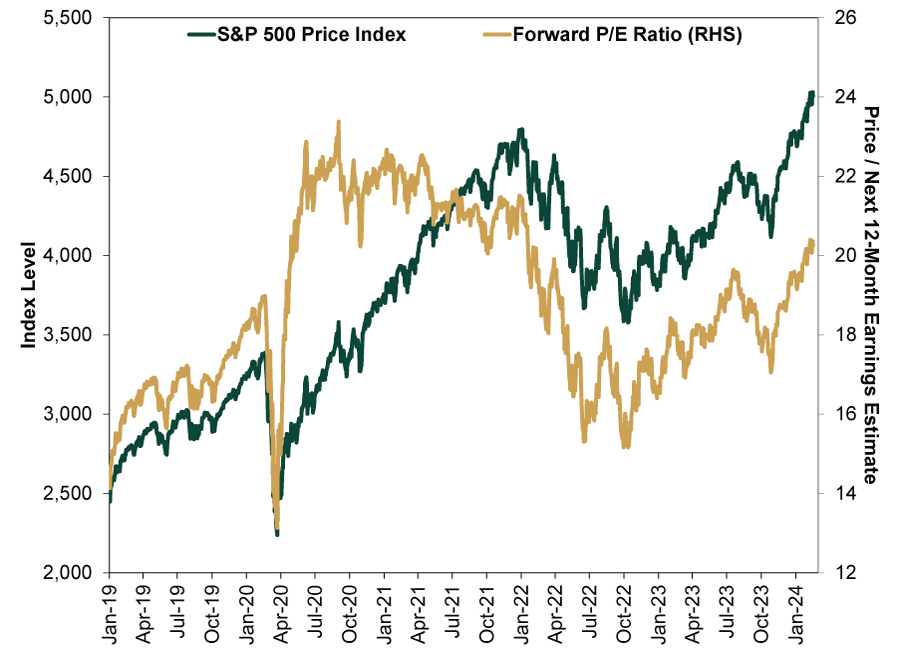

Valuations tend to hit headlines when they are high by some arbitrary standard, so it is no shock that the S&P 500’s forward P/E crossing 20 for the first time in two years roused some attention. But valuations have never predicted future returns—including allegedly forward-looking forward P/E ratios. Exhibit 1 shows one way to see this. From May 2020 to January 2022, the S&P 500’s forward P/E exceeded 20. Yet the S&P 500’s return during that time was 63.8%.[i]

Exhibit 1: No Problem Rallying With P/Es Above 20

Source: FactSet, as of 2/20/2024. S&P 500 price index and 12-month forward P/E ratio, 12/31/2018 – 2/16/2024.

There isn’t any magic valuation threshold stocks cross that tells you where they will go next. Consider the reason forward P/Es soared from 13.1 in March 2020 to 23.4 in September 2020. As Exhibit 2 shows, analysts were furiously slashing their 12-month forward earnings estimates—after stocks had already tanked, pre-pricing the actual earnings decline from COVID lockdowns. Then, stocks moved on. The S&P 500 troughed late that March and then rallied sharply before analysts reversed course and began raising their earnings estimates. The ‘P’ jumped while the ‘E’ was still struggling. That wasn’t unique to 2020 but rather normally happens in a bear market’s aftermath, which is why forward P/Es often seem elevated in bull markets’ early stages. It is simple math, not a sign stocks are actually overvalued. It just means analysts are playing catch up as they slowly fathom the new bull market.

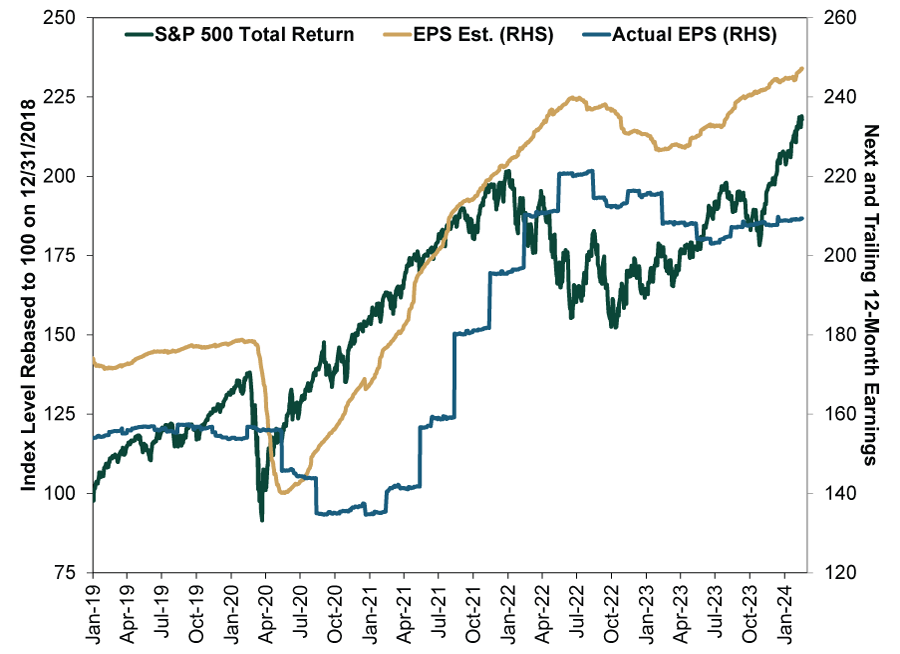

Exhibit 2: Stocks Price in Earnings Beforehand

Source: FactSet, as of 2/20/2024. S&P 500 total return, 12-month forward earnings-per-share (EPS) estimates and trailing 12-month EPS, 12/31/2018 – 2/16/2024.

The broader lesson here: Valuations say so little because stocks price in expected earnings in advance—well ahead of consensus. They are exceedingly good at this. Exhibit 2 shows 2020’s February – March bear market sensed the lockdown-induced earnings drop two months before analysts did—and five months before earnings actually troughed. Stocks didn’t wait—or care about elevated P/Es. Similarly, 2022’s bear market started seven months before analysts had an inkling that corporate profits would struggle. Then the current bull market (green line) started October 2022, four months before earnings estimates (yellow) turned up and eight months before earnings reports (blue) really registered a recovery.

It isn’t where earnings have been, but where they are going against what is priced in now—which present valuations echo. Notice trailing earnings remain below their 2022 peak, yet stocks are making new highs—already anticipating forward earnings’ ascent. Current valuations, even those based on analysts’ future earnings projections, can only reflect present thinking and market movement, not what earnings will actually do—reality. And that gap between reality and expectations is what drives stocks most.

Extreme moves in valuations can signal sharp sentiment swings, but even then, they aren’t a great timing tool, and there is no magic threshold. Because P/Es incorporate past prices—and past prices never predict—they won’t tell you where stocks are headed. Fundamentally, forward-looking markets’ longer-term direction depends on what isn’t priced. How earnings evolve over the next 3 to 30 months based on new, incoming information versus present perceptions will determine stocks’ broader path, wiggles along the way notwithstanding.

Eventually expectations will likely get too high, setting up disappointment. But we seem to be early in that progression today, with sentiment only gradually becoming less skeptical. In our view, there is much more bull market to go before earnings expectations become impossible to reach.

[i] Source: FactSet, as of 2/20/2024. S&P 500 total return, 5/4/2020 – 1/19/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today