Personal Wealth Management / Market Analysis

An Update on Chinese Property Developers

China’s property developers continue seeing stress in credit markets, but the impact still seems limited.

Editors’ note: MarketMinder doesn’t make any individual security recommendations. Companies mentioned here are only for illustrative purposes to highlight a broader theme.

Evergrande’s missed bond payment a few weeks ago struck fear into the financial world. Since then it has missed a couple more and given few indications it plans on paying international bondholders. A few other Chinese property developers—mostly small, distressed ones—have followed suit, to varying degrees. Yet the chaos most expected and worried could spill globally seems absent. This doesn’t shock us—as we wrote recently, China’s financial system is largely still isolated from the world’s. But also, there are signs China’s government is acting to mitigate the local effect, and the process is playing out in an orderly fashion. In our view, this underscores why we didn’t and don’t believe Evergrande is a financial crisis catalyst—neither locally in China nor globally.

Evergrande has now missed a combined $279 million in offshore coupon payments since late September, which will officially constitutes a default if they remain unpaid after a 30-day grace period expires on Saturday. Meanwhile, more credit events are popping up. To date, seven small, distressed developers including Fantasia Holdings, China Properties Group and Xinyuan Real Estate have either missed payments to offshore creditors or compromised with them, replacing existing debt with new bonds. Yet all these transactions are in the millions of dollars—far too small to cause fundamental troubles in China’s economy, much less the world’s.

Some estimate China’s real estate market has amassed $5 trillion in debt, which has doubled since 2016.[i] This debt, however, doesn’t all come due at once—it is staged over a sequence of years. About half of it, the plurality, is bank loans—not bonds, which amount to about 10% of developers’ outstanding debt.[ii] With China’s financial system largely still closed off from the world’s, the chances of this hitting Western banks is minimal. Furthermore, China’s government has a lengthy history of recapitalizing banks if it really, really needed to. We see little reason to think that is necessary now, but it is worth noting past trends, given the government’s emphasis on social stability.

Already, it appears China’s government is acting in other, more limited ways to prevent major domestic fallout. Authorities are adopting measures to isolate Evergrande and other problem areas, while providing liquidity backstops to ensure credit keeps flowing to the property sector generally.

First, for property developers with the ability to pay, the People’s Bank of China (PBOC) is firmly hinting that not doing so isn’t a great option and encouraging them to cough up funds.[iii] By not bailing out problem institutions, the PBOC is seemingly signaling it is serious about reform and seeking to establish more market discipline in the sector and requiring companies to take actions in the market to try and stay afloat.[iv] So, for example, a Chinese state-owned asset manager recently bought out Evergrande’s stake in a struggling bank to limit contagion, but authorities have thus far given no indication they will help property developers directly.[v]

Second, the PBOC and other Chinese banking regulators are taking steps to support the property market’s current soft patch. This includes relaxing mortgage restrictions and injecting more than $100 billion into the financial system, which has helped cut overnight borrowing rates and head off broader market hiccups.[vi]

Third, local authorities are introducing support measures to ease credit. Some local governments including Harbin, northeastern Heilongjiang’s provincial capital, have allowed property developers to access presale funds held in government escrow accounts to pay suppliers and complete unfinished, pre-sold projects. It is also subsidizing new home purchases for qualified residents.[vii] Then too, just as the developed world typically handles defaults, China is taking a more market-oriented approach. Property developers’ debt workout talks have begun. Reports indicate Evergrande’s CEO has met with creditors and investment banks over possible asset sales and debt restructuring.

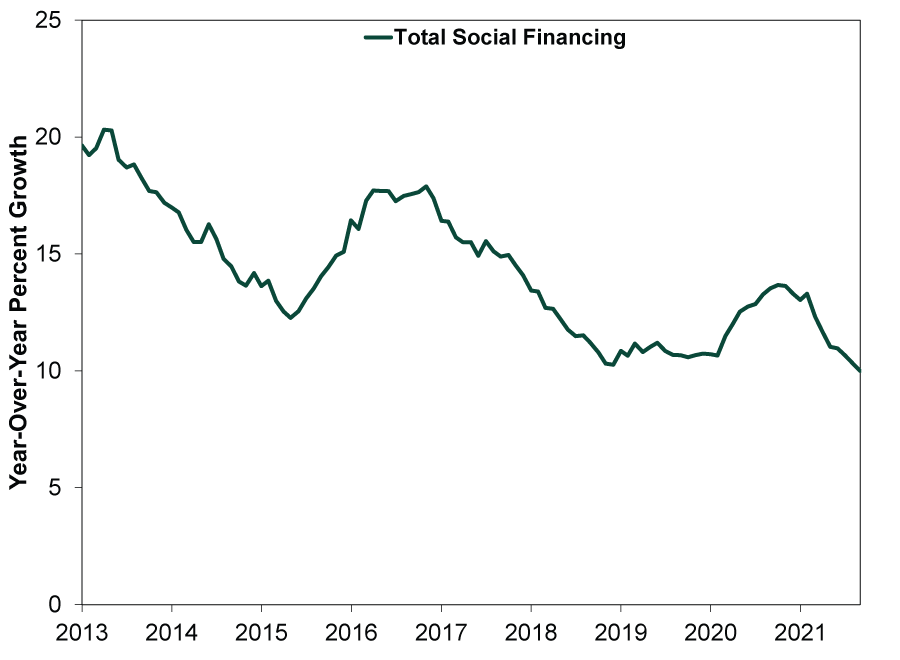

This doesn’t mean everything is grand, but a calamity doesn’t seem likely. It looks more like China is letting the air out of a frothy pocket of its economy where speculation has reigned in recent years. With the slowdown in the sector and overall focus on deleveraging, China’s total social financing growth rate—its broadest measure of credit—is hitting new lows. (Exhibit 1) Yet the central bank’s shifting focus to “promoting healthy property markets” suggests a more sanguine outlook.

Exhibit 1: China’s Total Social Financing

Source: FactSet, as of 10/14/2021. Aggregate Social Financing, January 2013 – September 2021.

All this looks engineered and intentional, not uncontrolled and uncontainable as many now fear—and all appears to be in line with the Chinese government’s stated aim to maintain social stability above all else. If Evergrande’s default process is orderly and encourages more market-oriented discipline, it would be a better outcome than most currently expect—a pretty bullish surprise for Chinese markets.

[i] “Beyond Evergrande, China’s Property Market Faces a $5 Trillion Reckoning,” Quentin Webb and Stella Yifan Xie, The Wall Street Journal, 10/10/2021.

[ii] Ibid.

[iii] “China’s Warning to Evergrande Was Aimed at Fantasia, Too,” Shuli Ren, Bloomberg, 10/17/2021.

[iv] “China Won’t Save Evergrande for Many Good Reasons,” Shuli Ren, Bloomberg, 10/15/2021.

[v] “Evergrande to Sell $1.5 Billion Stake in Chinese Bank, as It Faces Another Bond Interest Payment,” Weizhen Tan, CNBC, 9/28/2021.

[vi] “China Eases Mortgages for Rest of Year on Evergrande Contagion Worries,” Staff, Bloomberg, 10/15/2021.

[vii] “China’s Harbin Lends Hand to Property Firms; Morgan Stanley Upgrades Sector View,” Staff, Reuters, 10/11/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today