Personal Wealth Management / Economics

Another Multi-Decade Inflation High

Falling uncertainty, not inflation, is likely key to returns from here.

Editors’ Note: Inflation has become a hot political topic, and we aren’t commenting on it from that standpoint. We are looking at the investment-related implications only.

9.1%. That is the latest multi-decade high the US’s Consumer Price Index (CPI) year-over-year inflation rate hit in June.[i] When headlines weren’t stewing over what the acceleration from May’s 8.6% means for the Fed’s decision making at its next meeting in two weeks, they were looking for some signs—any signs—that the pain will soon end.[ii] We understand the impulse: The more prices rise, the more it creates hardship for many and forces people to forego things. Inflation has also sent political rancor to the boiling point, which is never pleasant. But from an investing standpoint, pinpointing inflation’s peak isn’t necessary. Stocks don’t need prices to ease—inflation is just one of seven or eight (at least) items weighing on sentiment right now. The key to recovery isn’t fundamental improvement, but gradually easing uncertainty on a multitude of fronts.

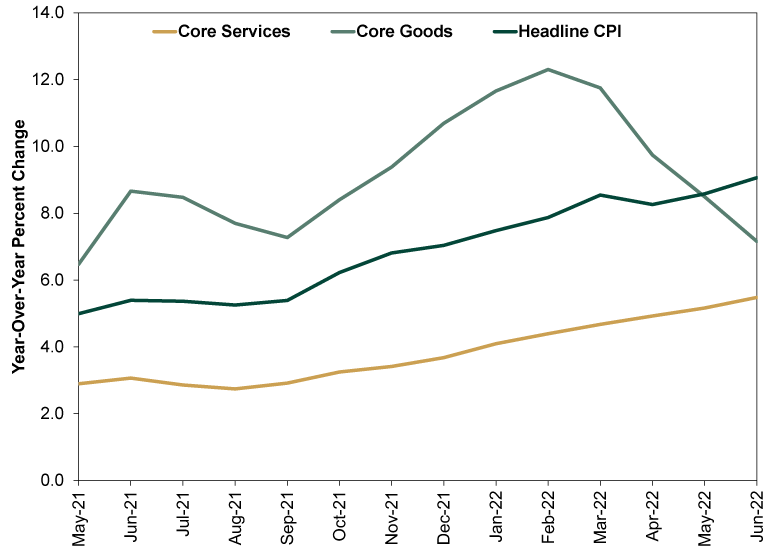

The main source of uncertainty underlying inflation right now is the main contributor: energy prices. Those rose 34.6% y/y, which included a 48.7% rise in gas prices.[iii] (Ugh.) That led to a sharp divergence between headline and core inflation, which excludes food and energy prices—not because they are meaningless (they aren’t), but because they are quite volatile and can occasionally mask underlying trends. Core CPI actually ticked a wee bit slower, from 6.0% y/y in May to 5.9%. That doesn’t mean inflation is for sure slowing from here, but it does cut against the notion that all prices are accelerating rapidly.

Perhaps equally encouraging, core goods prices (meaning, goods excluding energy and food) continued decelerating. We bring this up because energy prices aren’t the only place where oil prices can affect broader consumer prices. Oil is a feedstock for a number of consumer products—pretty much anything including plastic or other petrochemical derivatives, such as shoe soles, will have oil as an input. Early-year metals spikes flowed through to consumer products similarly. Combined, these are big reasons core goods inflation spiked to 12.3% y/y in February. But it is down significantly since, reflecting easing commodity prices across the board. Core services prices have accelerated a bit, likely tied to higher operating costs, labor shortages and the general supply and demand imbalance caused by lockdowns and reopenings. If you have attempted to travel by air this summer, you know exactly what we are talking about. But the more these dislocations even out, the more prices should stabilize.

Exhibit 1: A Deeper Look at Core Inflation

Source: FactSet, as of 7/13/2022.

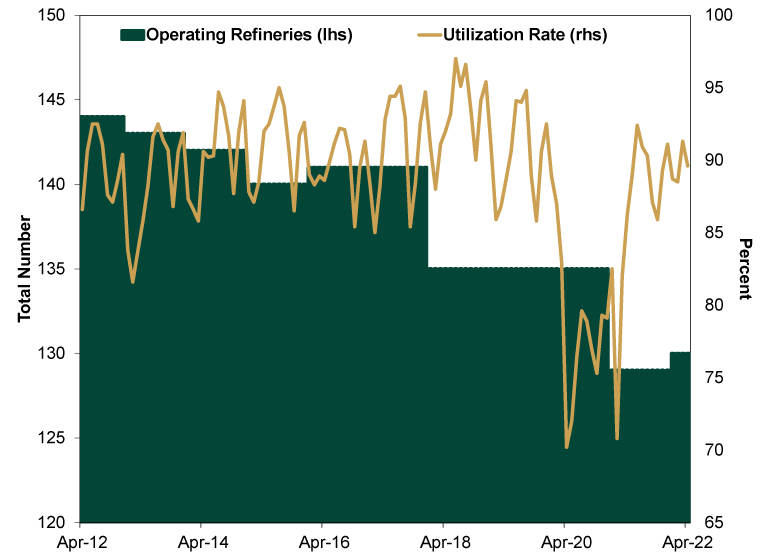

Of course, we also realize that it is the aforementioned oil and gas prices that are giving people the most angst today, and understandably so. On a month-over-month basis, gas prices jumped 11.2% in June, piling onto May’s 4.1% rise.[iv] There is a lot—and we mean a lot—of chatter about why gas prices are still jumping, given crude oil is now down below $100 per barrel—well off March’s high. The answer, unfortunately, doesn’t point to quick relief: US refining capacity is down, so even with the remaining refineries running more or less at pre-pandemic capacity, supply is tight. (Exhibit 2) Gas prices move on supply and demand for gasoline, so limited supply—coupled with resurgent demand in the first real summer of travel after lockdowns—is causing severe pain at the pump.

Exhibit 2: Gasoline Refining Capacity Is Constrained

Source: US Energy Information Administration, as of 7/13/2022.

Now, with that said, we could yet see lower oil prices flow through to gas prices. Contrary to popular belief, the crude oil spot price doesn’t determine what refineries pay. Most of these deliveries are locked down well in advance based on futures contracts—agreements to deliver oil in the future at a pre-arranged price. Depending on when a given contract was signed, refiners could still be paying well over $100 per barrel. But futures prices for delivery later this year are down across the board, which—in theory—should mean refiners’ input costs are slated to drop. This, at least in theory, should bring some relief.

Beyond oil, two factors could drive gas prices back down: rising supply or falling demand. The former is an exceedingly tall order, and we wouldn’t count on it. Refiners could crank up output a wee bit, presuming labor shortages and deferred maintenance aren’t insurmountable obstacles, but the infrastructure is old. Restarting mothballed refineries could work in theory, but many have been slated for demolition. Those that are for sale have attracted no buyers, and the longer they remain idle, the harder and costlier a restart becomes. As for building new facilities, the US hasn’t added a new major refinery since 1976, and changing that now seems next to impossible. Oil and gas companies are unlikely to take the risk—and shoulder huge up-front costs—at a time when gasoline-fired internal combustion engines are out of favor politically around the world. (We aren’t weighing in on the merits of that, just stating it as a fact that could dissuade a very long-term investment.) So, demand will likely be the swing factor. As high prices motivate people to cut consumption, we should eventually see some relief. This may not be the most satisfying solution, but it is how markets work.

Another thing markets do when prices are high and perceived shortages create opportunity: Spur innovation. That is happening today in the fuel world, with a number of startups globally working on synthetic fuel. We aren’t talking about ethanol—we are talking about really cool new technology allowing producers to create fuel from CO2, creating a one-to-one replacement that could power internal combustion engines. Sportscar manufacturers have quietly invested in this technology for a while, seeing it as key to preserving their cars’ after-market value, and high gasoline prices have spurred a wave of new investment this year. It won’t be an immediate substitution for gasoline—and it won’t offer immediate relief at the pump—but it is a fascinating development that could bring transport costs down over time and make oil prices much less of a factor.

In the meantime, though, we think inflation is less of a factor for markets than fear of it. Fear that it will stay this high indefinitely. And that fear is combined with a number of intersecting fears, including interest rates, supply chains and China’s intermittent lockdowns, not to mention the all-encompassing recession chatter. It has created a massive cloud of uncertainty. The more clarity investors get on these fronts, provided things don’t get massively worse from here, the more it should help stocks get over today’s jitters, map out the likely future, and move on. If signs of stabilization in core prices help that, great. If the relief in oil and other commodity prices help too, then also great. But when considering inflation and stocks, we suggest putting your focus there—the potential for falling uncertainty over the foreseeable future—and not inflation’s near-term ups and downs.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today