Personal Wealth Management / Interesting Market History

Central Banks’ ‘Independence’ Illusion

Seeing through the debate over central bank reforms.

Inflation wasn’t the only hot topic hovering over last week’s annual central bankers’ summer retreat holiday gathering in Jackson Hole, Wyoming. With the event happening days before the results of the UK’s Conservative Party leadership are set to be announced—and with frontrunner Liz Truss having pledged to review the Bank of England’s (BoE) mandate and perhaps even its autonomy—central bank independence seemed to occupy many pundits’ minds. There have been several long think pieces on this topic, all arguing independence is sacrosanct and must be protected against all threats. That is a fine enough argument in theory, I guess, but central banks aren’t as independent as we all have been led to believe—nor has the present system always delivered great policy. I am not advocating for policy changes or anything, but this debate seems more of a distraction than a market or economic driver.

Truss isn’t the only frontline politician considering shaking things up. Australia has just launched a formal review of the Reserve Bank of Australia’s (RBA) performance after it seemed to dither over hiking rates as inflation accelerated, leading RBA Governor Philip Lowe to call his bank’s forecasts “embarrassing.” Current BoE Governor Andrew Bailey has issued a similarly scathing self-assessment. Some US congresspeople argue the Fed is straying too far from its remit by focusing on sociological concerns, and there is chatter about new legislation to curb it. One candidate in Canada’s Conservative Party leadership race has pledged to fire Bank of Canada (BoC) Governor Tiff Macklem if he becomes prime minister.

It is axiomatic in the finance world that independent central banks are holy and anything less than full autonomy would run the risk of the Fed et al turning into the Central Bank of the Republic of Turkey (CBRT), which largely does President Recep Tayyip Erdogan’s bidding. Erdogan subscribes to the unorthodox view that high interest rates cause high inflation and has routinely installed governors who will comply and cut rates, then fire them once they start showing some independent thought. The result, predictably, is the Turkish consumer price index (CPI) inflation rate of 79.6% y/y in July 2022, a debased currency and plunging foreign exchange reserves.[i] This is an extreme example, but most observers argue that if central banks lose independence, governments will force them to cut interest rates at politically opportune times—regardless of what economic conditions warrant—and therefore risk creating big economic problems.

There is some history of this happening. Before 1978’s Humphrey-Hawkins Act established the Fed’s dual mandate (targeting price stability and maximum employment), it was not uncommon for presidents to pressure Fed heads into cutting rates or keeping them artificially low. Perhaps the most famous example is former President Richard Nixon, whose infamous tapes capture him pressuring then-Fed head Arthur Burns to keep rates low during the early 1970s’ inflation.[ii] Earlier, during and after World War II, the Fed became a tool to implement the Treasury’s interest rate caps. The economy and markets didn’t react kindly on either occasion, and in Burns’ case, it was a contributing factor to the crushing inflation later that decade—and the draconian rate hikes needed to tame it.

Yet if you look at the entirety of history, rather than extreme examples, it isn’t clear that there is a ton of difference between independent central banks and those controlled by finance ministries—at least in developed nations with strong institutions. The BoE didn’t have operational independence over monetary policy decisions until May 1997. When then-Prime Minister Clem Attlee nationalized it in 1946, it gave the Treasury influence over monetary policy and even enabled the government to issue specific directions to the bank. While the BoE’s historical presentations insist this was never formally used, stories of Chancellors of the Exchequer calling BoE staffers to 11 Downing Street to discuss interest rates are legion. Former BoE Governor Mervyn King, who served many years as the bank’s chief economist before taking the reins, recounted significant meddling in a Financial Times column: “After a satisfactory reception of a Budget, for instance, governments would ‘reward themselves’ with a rate cut. Elections influenced the nature and timing of decisions on interest rates. After 1992, and the introduction of the inflation target, a more systematic element was introduced with the monthly meetings between chancellor and governor, and their advisers. Even then, politics were never far away. One chancellor I recall said at the outset of such a meeting: ‘I want to make it clear that interest rates are not going to change but now I have to make it clear I would like to hear the arguments.’”[iii]

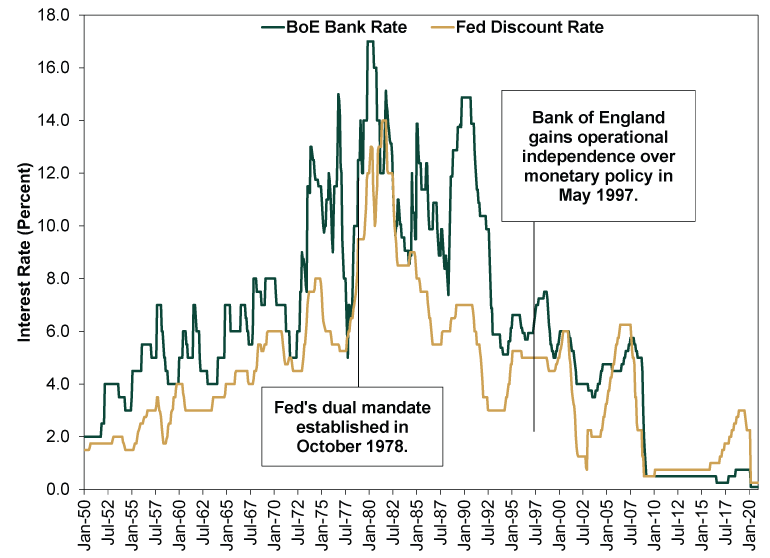

So, unofficial political meddling. And yet, as Exhibit 1 shows, it isn’t so apparent when you compare the BoE’s policy rate to the Fed’s discount rate, which is the best policy rate proxy with a long, continuous public history. Since 1950, they have tracked quite closely in direction, though not magnitude. The BoE’s rate cuts were often steeper, but so were its rate hikes. It was frequently more aggressive about raising rates than the officially independent Fed. If anything, rate hikes got less aggressive after independence, not more so.

Exhibit 1: Guess Which Central Bank Was Independent

Source: FactSet and St. Louis Federal Reserve, as of 8/26/2022. Bank of England Bank Rate and Federal Reserve Discount Rate, January 1950 – December 2020.

Why does politicized monetary policy bear so much resemblance to independent decisions? A theory: Central bank independence is mostly imaginary. No, we don’t have good evidence of heads of government strong-arming their central bank chiefs. But for one, politicians set important parts of central banks’ mandates. Two, central bank governorships are political appointments, and many are accountable to legislatures. Once confirmed, simple human nature dictates that central bank chiefs want to be reappointed (or at the very least not fired), giving them incentive not to rock the boat too much. Then too, their goals—keeping inflation low and the economy growing—often coincide with politicians’ hopes, giving them common cause. Dedicated inflation targeting was supposed to fix this, adding more objective accountability, but it has largely failed. First central banks habitually undershot the target for years. Now they are laughably high of the mark.

Central bank independence often goes out the window in a crisis. In 2008, Fed transcripts show it and the Treasury were in cahoots over how to address every big financial institution on the brink of failure. Their decision to let Lehman Brothers fail after bailing out Bear Stearns in an identical situation six months prior triggered panic and chaos, contributing to one of stocks’ worst autumns on record. In 2020, the COVID response was similarly coordinated by both institutions, with the Fed creating direct lending programs championed by politicians—programs that seemed just a bit outside of its remit. Central banks elsewhere similarly coordinated policy with politicians. Academics can debate endlessly about the relative wisdom and success of all of this, but it was all a shotgun wedding of politics and monetary policy.

The late, great Nobel laureate Milton Friedman once quipped that the real way to fix monetary policy would be to replace all the human central bankers with a computer program that would ensure the broad money supply grows by a stable, predictable amount every month. A logical, elegant solution, if not a complete fantasy given the impossibility of precisely defining and measuring money. But failing that, no matter how independent central bankers are, there will always be errors. And politics. At the end of the day, central bankers are human. They are subject to human failings like pride, incompetence and guessing wrong.

As for the politicians, if they want to change a central bank’s mandate, well, that is just swapping one flavor of political influence for another. It won’t automatically make policy better or worse. It doesn’t automatically make policy errors any more or less likely. Nor will adding more oversight and accountability. Mind you, the review processes could create uncertainty, and that can weigh on sentiment and stocks, but extrapolating huge long-run economic consequences seems like a bridge too far.

[i] Source: FactSet, as of 8/26/2022.

[ii] “How Richard Nixon Pressured Arthur Burns: Evidence From the Nixon Tapes,” Burton A. Abrams, Journal of Economic Perspectives, Volume 20, Number 4, Fall 2006, pp 177 – 188.

[iii] “How the Bank of England Was Set Free,” Mervyn King, Financial Times, 5/5/1997.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — August 3 - August 72026-08-11

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today