Personal Wealth Management / Economics

China’s ‘Reopening’ in Perspective

Don’t overestimate the global economic impact for good or ill.

So China and Hong Kong are easing some COVID restrictions. Sort of. And predictably, pundits’ reactions are mixed. Some warn China’s economy has been shut down for too long to achieve a rapid bounce as Western nations did when ending lockdowns for the last time. Plus, others warn that low immunity and vaccination rates mean COVID could ripple through the country, offseting the allegedly modest economic benefits that a reopening might otherwise bring. Others tout the economic potential but warn it will drive inflation back up, presuming weak demand in China is the sole reason commodity prices moderated after spiking in February and March. Our advice to both camps: Hold your horses. The steps announced thus far are quite modest, and while we see some potential economic positives, rip-roaring growth seems unlikely given the other issues China is presently dealing with. It should still contribute nicely to global growth, and these measures ought to aid sentiment some. But we don’t see a huge demand surge capable of lifting the rest of the world—or global inflation.

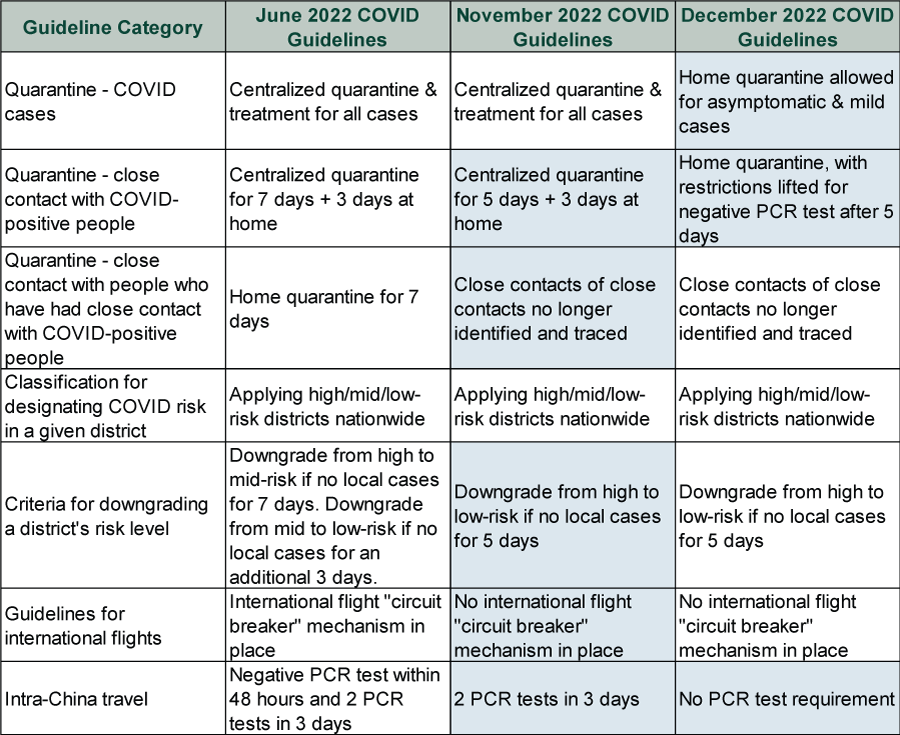

Crucially, China did not exit its Zero-COVID program Wednesday, when officials announced the latest spate of relaxations. The virus remains a Category A infectious disease, keeping lockdowns on the table. However, testing and quarantine requirements have eased for residents and international travelers, and use of the COVID pass is getting scaled back, which should enable more retail foot traffic. Exhibit 1 rounds up the major changes.

Exhibit 1: A Summary of Easing COVID Guidelines

Source: Government announcements. Shaded areas represent easing from prior guidelines. Hat Tip: Austin Fraser.

On paper, these changes seem positive for economic growth. If seen through without backsliding in the event COVID infections spike, they should help boost consumption and economic activity in general. They should also help factories stay online, easing supply chain hiccups for the world and supporting China’s industrial output. But there are a lot of ifs here. Should COVID rip through the populace this winter and hospitalization and death rates spike, the political calculus could shift back from reopening to protection. All of this defies prediction, as none of the variables involved are market functions.

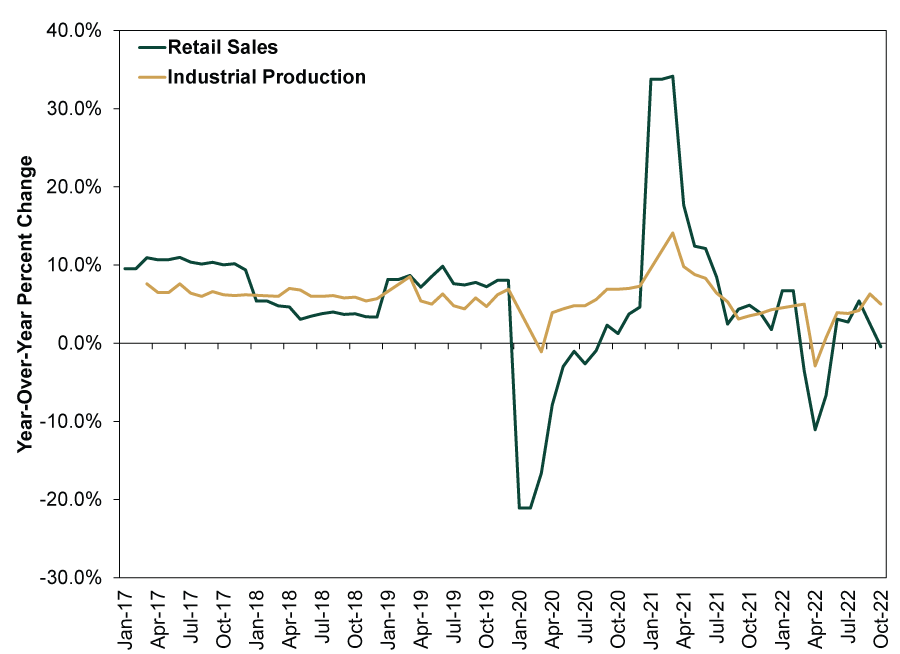

But for argument’s sake, let us presume this easing sticks and China formally exits Zero-COVID next year, following the highly likely winter waves and Lunar New Year travel season. That is the current consensus expectation. Experience in the US and Europe suggests this would bring an initial surge in demand that supply can’t keep up with, creating dislocations. That probably means improved growth in retail sales, industrial production and other widely watched metrics, but with a ceiling from supply constraints. However, a surge seems unlikely, if only because China hasn’t been fully locked down for a while—we have already seen the initial reopening boom. Rather, the country has endured a Whack-a-Mole of regional restrictions. Hence data lately have muddled through. Easing restrictions probably helps reduce economic volatility, but the big moves are likely behind us.

Exhibit 2: China Already Had Its Lockdown Bust and Reopening Boom

Source: FactSet, as of 12/8/2022.

Then too, COVID restrictions aren’t China’s only economic headwind. There is also the ongoing matter of China’s property sector, which the government is still trying to sort out. While we think people have long overestimated real estate as an economic driver there, property sales’ continued sluggishness likely will weigh on investment in the near term. Don’t get us wrong: A huge property crash remains unlikely. The government continues sending targeted support to solvent-but-illiquid property developers, supporting construction and offering relief to homebuyers whose under-construction units are woefully delayed. All of this should help prevent the worst case scenarios that Western observers have warned of for more than two years now. But there is a big difference between not crashing and soaring, and sluggish property growth probably does counterbalance reopening somewhat.

This is crucial because construction is the source of much of China’s commodity demand. If developers are working through building backlogs and not launching new projects left and right, it probably prevents the massive demand surge for copper, steel and other industrial metals some worry will reignite commodity prices and boost inflation. Meanwhile, supply—the primary downward force on prices this summer and autumn—remains higher than many anticipated in the wake of Russia’s Ukraine invasion. Easing political tensions in copper-heavy Peru, where leftist Pedro Castillo is now out as president following an attempted power grab widely described as a would-be coup, should also ease one of this year’s major copper supply concerns. Meanwhile, on the energy front, China remains a big buyer of Russian crude oil, keeping supply from the Americas, Middle East and North Africa available for buyers in Europe and elsewhere. Perhaps increased Chinese demand brings global consumption closer to supply—which has outrun demand in recent months—but that points to oil prices hovering in their current range, not soaring. That is doubly true considering Chinese oil demand isn’t wildly below the longer-run average, likely tied partly to its filling its strategic reserves and partly, again, to the fact the country wasn’t uniformly under COVID countermeasures.[i]

Mostly, we see China’s reopening as an example of what we call the Pessimism of Disbelief—headlines’ tendency to couch good news as bad late in a bear market (and early in the ensuing bull market, if the rally since October 12 indeed turns out to be the start of a new cycle). Even a gradual return to normal life there would be a positive economically, helping everyone work through COVID dislocations and helping output grow more steadily. Modest growth, which seems likeliest, would be better than the dismal scenarios many have penciled in. Yet headlines seem bent on finding the cloud in the silver lining and hyping the negatives to the masses. In our view, that creates a big gap between expectations and reality, building a nice wall of worry for a new bull market to climb—whenever one gets underway, if it isn’t already.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today