Personal Wealth Management / Market Analysis

Consumers Spend, Pessimism Permeates

The latest US economic data are solid, but doubts still abound.

After a strong January, global stocks stalled in February. Against that backdrop, the US Bureau of Economic Analysis (BEA) reported last Friday that January consumer spending grew at its briskest monthly pace in nearly two years. However, prices also picked up after several months of declines, stoking concerns that stubbornly elevated inflation will require further Fed rate hikes—which will weigh on growth. In our view, the ongoing gloom over solid economic data illustrates the prevalent skepticism present today—a common quality in market recoveries.

On the spending front, real (i.e., inflation-adjusted) personal consumption expenditures (PCE) rose 1.1% m/m, rebounding after two months of declines.[i] Looking under the hood, most measures were strong. Excluding volatile food and energy prices, real “core” PCE fared better (1.5% m/m), and spending picked up in services (0.6%) and goods (2.2%), with the latter breaking a two-month negative streak.[ii]

As spending jumped, prices ticked higher. The headline PCE price index rose 5.4% y/y from December’s 5.3% while the core (excluding food and energy) measure climbed to 4.7% from last month’s 4.6%.[iii] However, headline and core prices each jumped 0.6% m/m, both exceeding expectations—and grabbing eyeballs.[iv] This was headline prices’ first month-over-month acceleration since October and their fastest rate since June’s 1.0%.[v] Goods and services prices also rose 0.6% m/m.[vi]

The PCE report largely echoed January’s retail sales and Consumer Price Index data, but headlines’ rather dreary reactions offered some insight. Economists found myriad reasons to dismiss the strong spending numbers, including warmer weather, a low base from lackluster winter holiday spending, seasonal data adjustments, the boost to Social Security income and state minimum wage increases. All seem plausible, but we find it interesting that stronger-than-expected data generate plenty of excuses while a disappointing result typically doesn’t receive as much scrutiny. Take seasonal adjustment chatter. Some experts think the difficulty in ironing out seasonal fluctuations flattered January numbers, setting up a weaker February. We have seen this rationale applied to other recent datasets, including jobs. Now, statistics agencies’ calculations aren’t perfect, but we see it as a sign of sentiment that seasonal adjustment gets heaps of attention when it flatters the data—and not so much when potential skew is on the downside.

The inflation discussion also tilted pessimistic. Headline and core PCE prices had been trending downward since mid-2022, but we have seen any monthly uptick in prices treated as evidence inflation will sap consumers’ spending power. Moreover, stubbornly higher prices (as tracked by the PCE headline price index, the Fed’s preferred measure) allegedly mean the central bank will hike interest rates for longer than anticipated—risking hamstringing growth in its effort to tamp down inflation.

We acknowledge some January factors may have supported spending. For example, Social Security recipients started receiving a larger monthly benefit this year due to an annual inflation adjustment. While having more disposable income supports spending, this isn’t a one-time boost. Rather, it gives people more purchasing power from here compared to last year, which should incrementally support spending across the board throughout 2023.

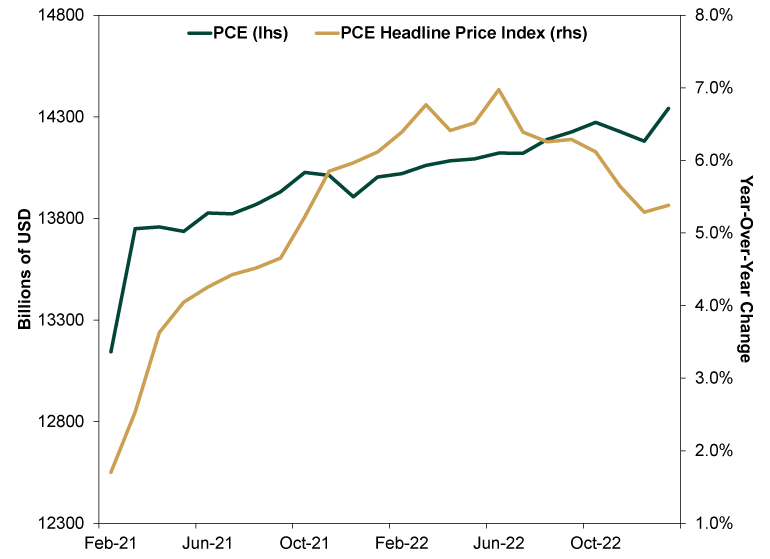

The myopic focus on monthly PCE results also overlooks consumer spending’s general resilience. Prices began rising in early 2021, yet a small late-year dip notwithstanding, spending mostly rose over the past two years—despite inflation reaching 40-year highs in 2022. (Exhibit 1)

Exhibit 1: Resilient Consumer Spending

Source: FactSet, as of 2/28/2023.

Considering January’s PCE numbers came out at the end of a tough week for global stocks, we understand the impulse to connect data with market movement. Since stocks are forward-looking, their recent struggles despite some strong economic data implies trouble looms, right? But in our view, reacting to any short-term data—whether economic or market—is a mistake. Stocks can rise or fall for any or no reason in the short term. Over the longer term, fundamentals outweigh sentiment-driven swings. Similarly, economic data can fluctuate in the short term, but one data point (good or bad) isn’t all-telling. What matters more is the overall trend—and the latest PCE data suggest consumer spending has remained resilient despite elevated inflation. We think stocks, as leading economic indicators, began pre-pricing this reality months ago.

Looking ahead, we still think this year will be good for global markets. Expectations remain low, as surveys suggest economists still expect recession. Resilient data have made them delay their anticipated recession start dates, not change their forecasts outright. In our view, it likely won’t take a whole lot for reality to exceed expectations. That said, market recoveries aren’t smooth, upward ascents, as dips and soft patches are commonplace. Now is a time for discipline—in our view, patience will reward long-term investors.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, US Q2 GDP, Eurozone Inflation

2026-07-27

2026-07-27 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 20 - July 242026-07-27

-

Politics Potential Implications of the Latest Sanctions2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today