Personal Wealth Management / Market Volatility

Counsel for the Mid-Spring Selloff

Volatility is part and parcel of bull markets.

Volatility can strike any time, without warning, for any or no reason—and it is striking now, with back-to-back S&P 500 drops worse than -1.0% unsettling investors after a banner Q1. Headlines cite the latest Middle East tensions and fading prospects for Fed rate cuts, and those may be affecting sentiment to a degree. But markets have a long history of moving on from such things quicker than most anticipate. Staying cool isn’t always easy, but we think it is the right move today.

Whenever volatility flares with scary stories accompanying it, a good tool is finding historical context and parallels. No, history doesn’t repeat perfectly. And no, there is no good evidence Mark Twain actually coined the observation that it often rhymes. But it is true that there is precious little that is truly unprecedented for stocks, and seeing how markets dealt with these things in the past can offer comfort and support confidence in stocks’ resilience—as well as give you a loose framework for assessing probabilities.

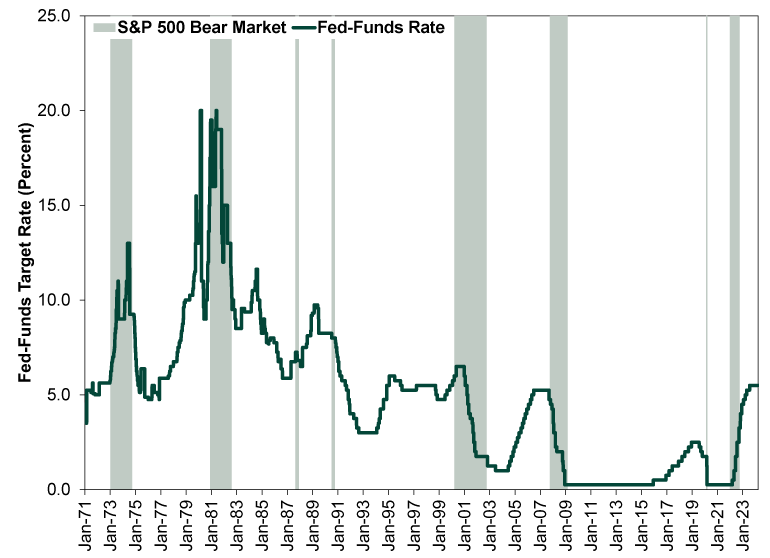

Consider rates and the higher-for-longer talk. Exhibit 1 re-runs a chart we showed you last week: The fed-funds target rate and S&P 500 bear markets. Then, we made the simple point that while rates are high relative to the 2010s, that low-rate period is an aberration. Relative to the full history, rates are pretty normal. The long-term average fed-funds rate since 1971 is 4.92%.[i] Today’s target range of 5.25% - 5.5% is pretty darned close. Oh and it is bang on the median since 1971, 5.25%.[ii]

Exhibit 1: An Antidote to Interest Rate Recency Bias, Revisited

Source: FactSet, as of 4/1/2024. Fed-funds target rate, 1/8/1971 – 3/28/2024. Series switches to the upper bound of the fed-funds target range in December 2008, when the Fed’s methodology changed.

But look closely at the non-shaded periods. Rates were much higher than now throughout the 1980s bull market. That was a really, really good time for the US economy and stocks. Even though mortgage rates, consumer loans and all the rest were more expensive. The go-go 1990s were a certified boom despite rates being in the same neighborhood they are now. Did that prevent massive investment in Information Technology and all things Internet and Silicon Valley? Did it render a moribund economy? Prevent what was then history’s longest bull market? No, no and no.

On both occasions, society knew perfectly well how to function with money being more expensive. That knowledge may have been buried in the country’s subconscious after the 2010s, but such things don’t go away. We know this because the economy is currently growing fine with today’s interest rates. Consumers did a lot of the heavy lifting while businesses battened down the hatches in anticipation of a recession that never came in 2022 and 2023, but there is mounting evidence that business investment is picking up. High rates aren’t starving the economy of capital. People may have a hard time fathoming this, but markets are generally quite good at seeing through the noise eventually—even if the noise knocks sentiment in the short term.

As for the other big headline concern causing some jitters, we know the escalating conflict between Israel and Iran is a sensitive subject for many, not least because of the human factors whenever missiles fly—and the fear that regional armed conflict can easily go global. Yet, sadly, we have a long, long history of conflict in the Middle East both raging and having only an isolated, local impact. Israel’s conflict with Iran-backed Hezbollah in Lebanon happened during the heart of the 2002 – 2007 bull market. 1967’s Six-Day War, which pitted Israel against three of the region’s major powers (Syria, Jordan and Egypt), failed to derail a nascent bull market. The Iran-Iraq war raged for most of the 1980s’ bull market. Often the run-up to and outbreak of conflict can cause volatility as uncertainty spikes, and perhaps we are seeing that to a degree now. But it is usually short-lived.

Now, as we wrote of the Middle East war earlier, the human tragedy is large but the economic effects are small. That remains true today even after Israel and Iran’s moves. Many will accept this but worry the spread will go even wider. While this is possible, that is almost always the fear when regional conflicts break out—see Ukraine in 2022. The risk here is extrapolation—investors projecting broader and broader conflict out of fear. Don’t let emotions steer your portfolio decisions, especially when they don’t hinge on widely watched factors.

Generally speaking, bear markets don’t start when everyone is on high alert for them and warning that every seeming negative could have a big impact. Those fears get priced in, adjusting expectations downward and making it easier for reality to surprise to the upside. Mind you, none of this precludes a correction—a sharp, sentiment-fueled drop of -10% to -20%. Those are always possible, and perhaps one is underway. But corrections usually end as suddenly as they begin. And since they fall on sentiment, always wild and unpredictable, trying to time and skirt them is usually an exercise in futility. Most often, people risk selling after stocks fall and buying back in after they recover.

So again, stay cool. Volatility is uncomfortable but normal. Enduring it is the toll stocks charge for their beautiful long-term returns. Fun? No. Rewarding in the end? Usually.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today