Personal Wealth Management / Financial Planning

Delineating the US Government’s Two Inflation-Linked Investment Options

Know your I Bonds from your TIPS.

With inflation at 40-year highs, investors seem to have many questions about “inflation-protected” options. Two seem to continually come up: inflation-indexed US savings bonds (known as I Bonds) and Treasury Inflation-Protected Securities (TIPS), with many investors seemingly confusing and conflating the two. Now, we don’t think the current environment necessarily calls for either. But if you are considering these assets, it behooves you to understand the vast differences between them.

What are they?

I Bonds are US savings bonds that earn interest based on a fixed rate plus an inflation rate (based on US Consumer Price Index, or CPI).

TIPS, as the name implies, are US Treasury securities that pay a fixed coupon rate and whose principal is adjusted due to changes in CPI. If US CPI rises, TIPS’ principal value is adjusted higher; if CPI falls (i.e., deflation), principal value does, too. Thus, inflation affects both the interest payments you receive and the security’s value at redemption (or at the point you sell it). A fixed interest rate applied to a higher principal yields a higher interest payment in dollars, and the principal rises over the lifespan of the bond if CPI is positive. While principal is adjusted downward in deflationary times, it never falls below its value at issuance. Yet, as we will discuss momentarily, this doesn’t make TIPS a surefire inflation hedge.

How do they adjust for inflation?

I Bonds’ interest payments are based on a semiannual inflation rate, which resets every May and November. The rate you receive depends on when you buy the bond, but it updates every six months. Currently, the going interest rate is 9.6%, and you can buy I Bonds at that rate through October 2022.[i]

TIPS’ principal adjusts semiannually based on a formula called the Inflation Index Ratio, which the Treasury calculates based on CPI. The bond’s coupon rate then applies to that adjusted principal, giving you higher interest payments when prices have risen over the past half year.

How do interest payments work?

I Bonds’ interest accrues and compounds over the life of the bond and is paid out upon the bond’s maturity or redemption only.

TIPS pay interest semiannually.

Are these actual inflation hedges?

This question gets to the heart of the matter, and the answer is: It depends. I Bonds are a handy way to shield small portions of cash from inflation’s corrosive effects, although there are redemption restrictions to be aware of, which we will detail shortly.

TIPS, however, aren’t intended as nominal protection against inflation. Rather, they aim to guard against inflation relative to a normal Treasury bond. A normal Treasury bond pays interest to account for inflation risk—the point is to compensate for the fact that your principal would have less purchasing power at maturity than it did at the bond’s issuance. But interest rates don’t always perfectly offset inflation, so TIPS’ purpose is to add extra compensation to preserve your purchasing power over the lifespan of the bond. However, given TIPS yields are often far below nominal Treasury yields, we wouldn’t overstate their powers.

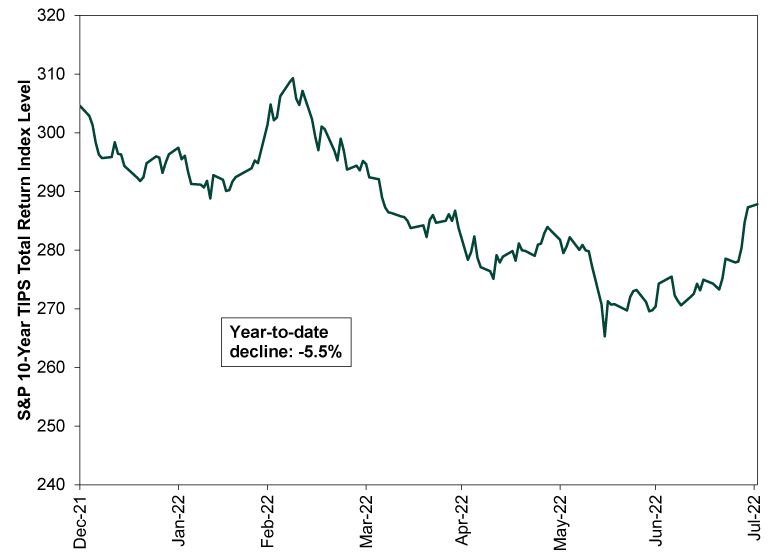

Additionally, TIPS aren’t hedges against short-term price fluctuations. They are bonds and, like bonds, their values rise and fall in the secondary market. General bond market trends, not inflation, tend to be their primary performance drivers, making them subject to interest rate risk. When interest rates rise, Treasurys and TIPS alike will fall. That happened this year, rendering deep TIPS declines even as inflation accelerated to 40-year highs. (Exhibit 1) During the slide from mid-March through June, TIPS underperformed non-inflation-protected US Treasurys on a cumulative basis, although TIPS are slightly ahead year to date. Also note that for years, until very recently, TIPS yields were negative, locking in losses for anyone who bought at those prices and planned to hold to maturity.

Exhibit 1: TIPS Haven’t Been an Inflation Hedge This Year

Source: FactSet, as of 8/2/2022. S&P 10-Year TIPS Index total return, 12/31/2021 – 8/1/2022.

How and where can I buy them?

I Bonds are available through the US Treasury’s TreasuryDirect website only.

TIPS are purchasable at auction through the Treasury or via the secondary market through banks, brokers and dealers.

Are there purchase limits?

I Bonds are available in amounts of $25 or more, and the annual purchase limit is $10,000 per taxpayer, although you can purchase up to $5,000 in additional I Bonds with your Federal tax refund per year. This must be stipulated when you file your tax return.

The minimum TIPS purchase is $100, and they are sold in increments of $100. There is ostensibly no limit for individual investors, although an individual bidder at a Treasury auction can buy up to $5 million in TIPS.

Are they available in funds?

There are no I Bond funds. You can only own the individual securities, and again, you must buy through the TreasuryDirect website directly. You cannot buy through your brokerage or financial adviser. There are no funds or ETFs containing I Bonds.

TIPS are available in funds. If you prefer the instant diversification of funds versus individual bonds, you can access them through a mutual fund or ETF.

Are they liquid?

I Bonds are the less liquid of the two. You can’t sell them on the secondary market. Rather, you can only redeem from the Treasury or hold them to maturity. I Bonds reach maturity 30 years after issuance, though investors can cash them out 12 months after purchase. Note, however, that redeeming within five years of the purchase date will cost you the last three months’ interest. We also suggest that if you own or choose to buy, ensure you look carefully at how to establish beneficiaries and what your heirs will need to do to gain access to them.

TIPS trade on the secondary market and are relatively easy to buy and sell. Funds and ETFs add more liquidity. However, supply is lower than normal Treasurys, which renders TIPS less liquid technically.

What are the tax considerations?

I Bonds are subject to Federal income tax but exempt from state and local income taxes. Owners can choose whether to pay tax on interest annually or defer reporting on interest until redemption or bond maturity.

If you hold TIPS in a non-qualified account (meaning, a traditional brokerage account or other account that isn’t tax-deferred), interest payments are also subject to Federal income taxes but exempt from state and local levies. The principal adjustment is also subject to Federal income taxes. Yes, income—not capital gains rates. You must also pay taxes on the principal adjustments in the year they occur—you can’t defer until maturity. The TreasuryDirect website has more details.

What is your opinion of each?

I Bonds may make sense for cash earmarked for expenses that are at least a year out, though losing three months of interest if you don’t wait out the full five-year lockup is an opportunity cost worth considering. What is right for you depends on your personal situation.

As for TIPS, we don’t think they are anywhere near what they are cracked up to be. They have underperformed traditional Treasurys for long stretches over time, even at times when the CPI inflation rate exceeded zero. Plus, we think the primary purpose of a fixed income allocation is to reduce expected volatility relative to an all-equity portfolio, which—over long periods—is already a more-than-effective inflation hedge. Adding TIPS into the mix doesn’t necessarily enhance this, and it adds more factors affecting the performance of that fixed income component—not least of all bidding wars for an asset that is more scarce than typical Treasurys.

We aren’t inherently for or against either of these securities, but as with any investment option, we think it is critical to look at your portfolio holistically: There are multiple ways to generate cash flow to meet your specific investment needs and generate returns that outpace inflation over time, and interest-bearing securities aren’t the only viable tools out there.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today