Personal Wealth Management / Market Analysis

Demand for Treasurys Is Alive and Well

Uncle Sam has plenty of buyers.

There are few pure certainties in investing. The fact that markets will be closed on Christmas in the West is one. Another potential contender: People will seemingly always be scared of high US debt. The fear never seems to go away, even during good times. It also takes on different flavors depending on the national conversation. Recently, many concerns center on bond demand. As in, who is going to buy all the bonds Uncle Sam needs to sell to finance the deficit? Analyses fretting allegedly weak auctions are creeping up, along with those breathing outsized relief when demand comes in higher than feared. To us, it is all overstated.

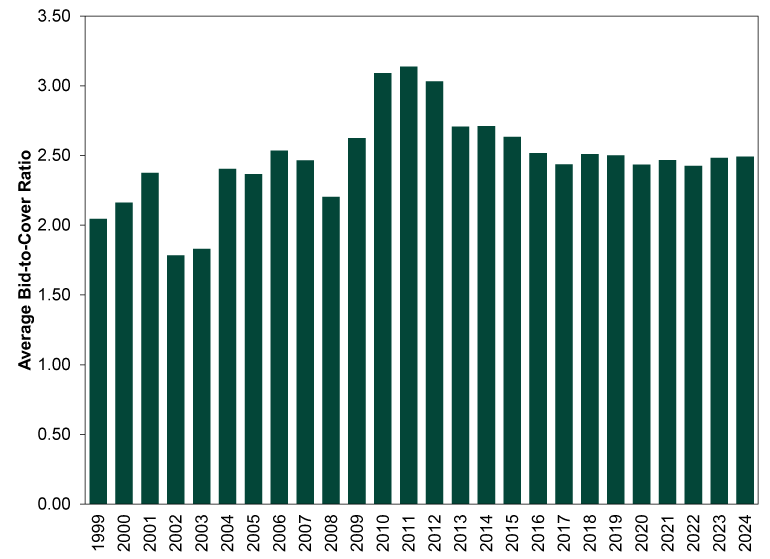

For one, recent auctions aren’t all that weak. A handy measure of demand is the bid-to-cover ratio, which compares total demand in dollars to the amount of bonds on offer. Exhibit 1 shows bid-to-cover ratios at 10-year US Treasury auctions since 1999, displaying the yearly average in order to account for the varying number and timing of auctions per year. The Treasury has held four auctions thus far in 2024, with an average bid-to-cover of 2.49. That is higher than all full-year averages since 2019.

Exhibit 1: Treasury Auction Demand by Year

Source: US Treasury, as of 4/18/2024. Bid-to-cover ratio at all auctions of 10-year notes, January 1999 – April 2024.

Now, demand at April’s auction was a tad lower than the prior few months, down to 2.34 after four straight auctions in the 2.5s. But we saw plenty of auctions in the 2.3s throughout the 2010s. Bid-to-cover ratios were routinely in the low twos and even the ones in the early and mid-2000s. In 2002, all but one auction fetched bid-to-cover ratios below two. In 2003, only two topped that mark. Are we all forgetting the terrible US debt crisis of 2002 – 2003? Or was demand ok then and therefore very likely to prove ok now?

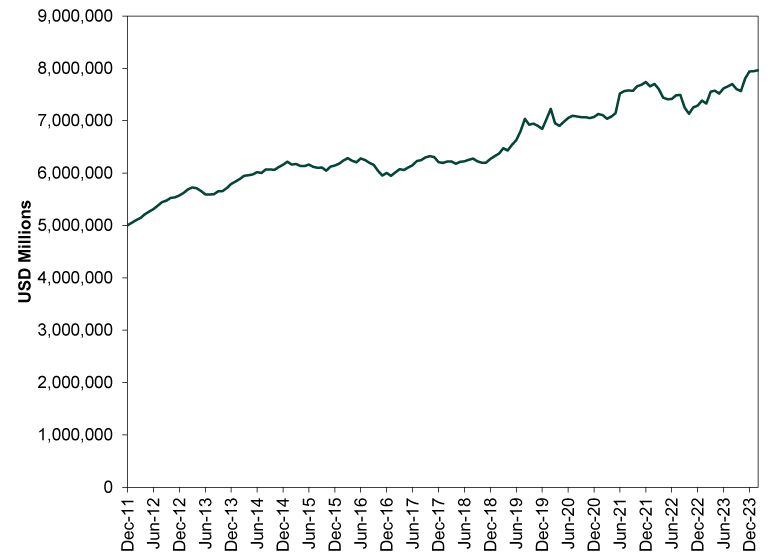

Some argue the real problem is that the US is dependent on the kindness of strangers—aka demand from foreign governments and investors—to finance its debt. The implication: As less friendly foreign governments diversify their dollar reserves, debt will become much harder to sell. This is an old argument, but it stepped up after the US put sanctions on Russia’s overseas assets in 2022, supposedly an incentive for other governments to sanction-proof their reserves. Reality indicates it isn’t happening in any meaningful sense. As Exhibit 2 shows, despite falling initially in 2022, foreign US Treasury holdings are up since Russia invaded Ukraine and stand at all-time highs.

Exhibit 2: Foreign Investors Love US Treasurys

Source: FactSet, as of 4/18/2024. Total foreign holdings of US Treasury Securities, December 2011 – February 2024.

There are some other interesting nuggets to key in on here. The latest downtick, which ran from December 2021 to October 2022, didn’t correspond with a major demand drop at Treasury auctions. Nor did demand at auction plunge in 2016, when foreign Treasury holdings fell as China pared its pile. Speaking of which, China isn’t the US’s biggest foreign creditor. That honor goes to Japan, which owns nearly $1.17 trillion in US Treasurys.[i] China clocks in at just $775 billion, or 2.83% of total US net public debt.[ii] For all the headlines China’s US debt ownership generates, it barely rates once you do the math.

Foreign investors actually own a smaller share of US debt now than in years past. In 2011, they owned nearly half of all net public debt. That gradually slipped to 40% in 2018, and for the past year it has waffled between 28.5% and 30%.[iii] Yet bond auction demand has remained robust, which tells us US investor demand is high and rising. That seems … good? Not bad?

The fear that investors will lose their appetite for US debt is as old as the hills and, in our view, is false. When you consider the competition, it is easy to see why. People will always need bonds, whether it is pension funds trying to manage liabilities, governments needing reserves, banks needing stable yield-generating assets to bolster balance sheets or individual investors seeking to reduce their portfolio’s expected volatility. The global bond pool is large but fragmented, and no other issuer comes close to matching the US Treasury market’s breadth, depth, liquidity and long history of stability. Other markets may have higher credit ratings, but they are minnows in comparison. And ratings don’t mean much in practical investment terms.

So no, we don’t think the available data support all the talk of weak bond demand being poised to ripple through the economy and other financial markets. It all looks to us like business as usual, with investors wanting to buy more bonds than the Treasury sells.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today