Personal Wealth Management / Market Analysis

Economic Green Shoots While Snow Falls?

Purchasing managers’ indexes ticked up in February.

Winter may still be raging, but it looks like there are some hints of green shoots … in the global economy, if not the soil. Yes, Tuesday’s batch of S&P Global’s February flash purchasing managers’ indexes (PMIs) showed service sectors in the US, UK and eurozone accelerating enough to pull the composite PMIs, which combine services and manufacturing, into expansion territory for the first time in months. We have suspected for a while that stocks’ rally since mid-October was the market pricing in the high likelihood the global economy would perform better than expected as 2023 unfolded. It is still too early to say with certainty that a new bull market is indeed underway, but PMIs are one more piece of evidence supporting the rally, in our view.

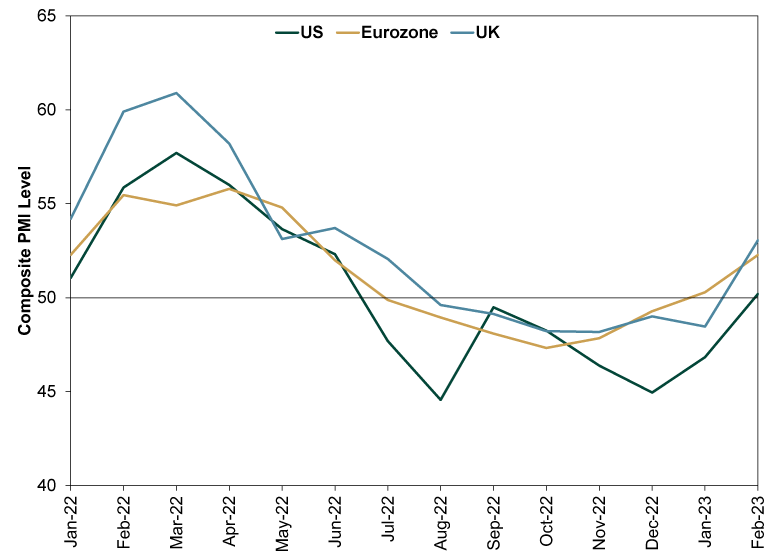

Exhibit 1 shows composite PMIs for the US, UK and eurozone over the past year. All had a grim second half of 2022, with both services and manufacturing in contraction the majority of the time. Last month, however, the eurozone flipped above 50, indicating a return to expansion. Now the US and UK have mirrored the move.

Exhibit 1: PMIs Are Back in Expansion

Source: FactSet, as of 2/21/2023.

Or rather, their service sectors are expanding, registering 50.5 in the US, 53.3 in the UK and 53.0 in the eurozone—with Germany at 51.3 and France at 52.8. Manufacturing contracted in all of these, although its declines were less broad-based in the UK and US.[i] As for the eurozone, S&P reported that while manufacturing contractions worsened in France and Germany, the rest of the eurozone enjoyed “broad-based growth” in both services and manufacturing, with the composite PMI for those nations combined rising from 51.4 to 53.9, a 9-month high.[ii] The eurozone always has pockets of strength and weakness, and for now it looks like growth outside the two largest economies is doing the heavy lifting. That isn’t surprising, given Germany and France appeared to have the largest power challenges this winter—Germany with natural gas potentially in short supply and France with its nuclear power plants repeatedly going offline. But both seem to have pulled through better than expected, basically giving the eurozone economy some bonus points.

With all that said, composite PMIs are output-only indexes—coincident, not forward-looking. PMIs’ new orders subindexes are the real forward-looking components, as today’s orders are tomorrow’s production. Those were overall not bad. In the eurozone, new orders expanded for the first time since May 2022, with services orders rising and manufacturing orders shrinking at the slowest pace since May. UK new orders rose for the first time in seven months, with services orders “solid” and manufacturing’s decline “marginal.”[iii] US orders declined, but by the narrowest margin since October. Services’ decline was “slight,” though manufacturing orders endured a “sharp downturn” as customers focused on running down inventories. That could point to restocking driving demand later, but only time will tell.

In our view, these PMIs are emblematic of economic data early in a bull market. Officially, the US, UK and eurozone aren’t yet in recession despite widespread forecasts to the contrary—forecasts that suggest expectations are very, very low. That makes it easy for nice headline results with mixed underlying data to qualify as a positive surprise. Stocks’ moving ahead of this is normal, as markets are forward-looking. Last year’s decline precipitated weakening economic data and all those recession forecasts, not to mention the contracting PMIs. Now we have stocks turning up ahead of PMIs, which are moving back into the black—with new orders mostly hinting at more growth to come.

Yes, both could turn down again. And yes, PMIs aren’t GDP. In 2022’s second half, contractionary PMIs paired with growing GDP for the most part. Maybe that flips in early 2023. Or maybe it doesn’t. Either way, stocks tend not to dwell on what is happening right this minute. They look 3 – 30 months out and appear to be pricing in continued improvement within that window. The latest PMIs suggest that isn’t irrational, in our view.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today