Personal Wealth Management / Market Analysis

Energy Stocks’ Hot, Late Summer Surge Should Cool

Oil prices look unlikely to fuel big Energy outperformance.

After languishing behind the rest of the market for about eight months, global Energy stocks enjoyed a late-summer burst. While the MSCI World Index is down -5.8% since July’s end Energy is up 3.5%.[i] In our view, the disconnect has a simple explanation, and we doubt this trend has staying power. This bull market has plenty of fuel, but we don’t think Energy is likely to lead it.

For the most part, Energy’s relative returns track oil prices. It isn’t a perfect correlation, but they move in the same direction more often than not, which we think is tied to Energy companies’ earnings deriving in large part from oil prices. There are exceptions and caveats, as with all things in financial markets, but higher oil prices typically widen oil companies’ margins. So as oil prices rise, it typically boosts Energy companies’ relative returns. No shock, then, that Energy stocks’ latest run accompanied ascendant oil prices and talk of crude hitting the allegedly magic $100 per barrel marker.

This same marker has created rather a lot of gloom toward the economy overall, hitting sentiment toward broader markets. Whenever oil gets pricey and gas prices heat up, people presume it will knock consumer spending and growth overall—logic being that as people spend more on gas, they have less for everything else. This year, these fears are getting extra jolts from the pending resumption of student loan payments, the spending down of pandemic-era saving and talk of consumers being tapped generally by higher prices. We addressed these here, here and here, and our views haven’t changed. But these fears appear to be colliding with oil prices to knock economic sentiment, and we suspect this has contributed to stocks’ wobbles.

In time, we think reality will prove these fears false, helping stocks resume climbing bull markets’ proverbial wall of worry. This includes fears of oil prices, which look unlikely to keep soaring from here. The latest increase appears tied to Russia and Saudi Arabia’s decision to cut output by 1 million barrels per day (bpd) in July and subsequently extend those cuts through yearend. This announcement was toothier than OPEC’s recent production target cuts, leading to actual output reductions—driving fears of a global supply and demand imbalance pushing prices higher. The economic theory here is correct, but we think it errs by ignoring the potential for supply elsewhere to rise—especially as higher prices encourage more production. This is the same oversight that led many last year to project sky-high prices above last March’s peak.

Since Russia and Saudi Arabia announced the cuts, US production is up half a million bpd to 12.8 million, covering half the alleged shortfall already.[ii] With production expected to top 13 million bpd by early next year, that is another fourth covered.[iii] And that is just the US! Folding in production from Brazil, Canada and elsewhere, the US Energy Information Administration sees global output growing by 1.2 million bpd this year—even with Saudi Arabia and Russia’s cuts—and another 1.7 million in 2024.[iv] Alongside modest global demand growth, this points to oil prices staying bound in their recent range.

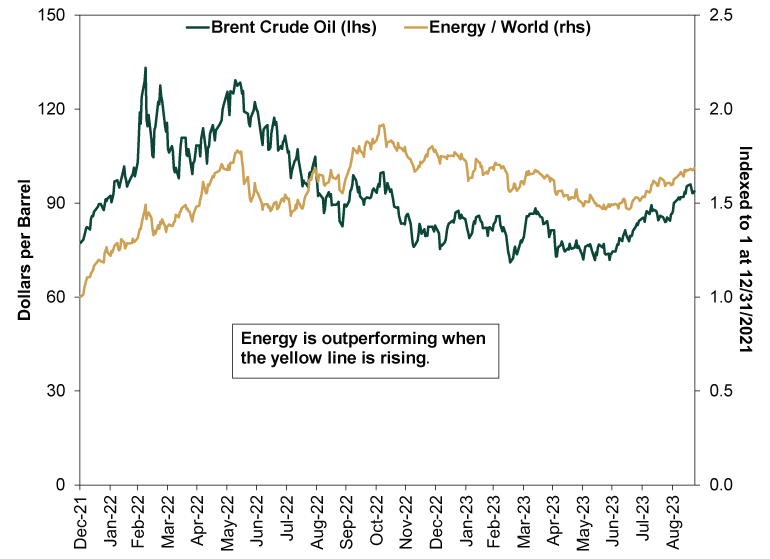

Which suggests Energy stocks’ recent outperformance is likely to prove fleeting. Exhibit 1 shows global Energy stocks’ relative returns and Brent crude oil prices since 2022 began. The directional relationship is rather uncanny, with spiking relative returns early in the year accompanying oil spikes. Then a big burst came from OPEC’s production target cuts in early October 2022, which drove fears of resurgent oil—much like now. This didn’t materialize, forcing Energy stocks to price in the disappointment after getting too far out over their skis. Now it seems to be happening again, and with oil unlikely to behave as feared, Energy stocks are probably once again set for a reality check.

Exhibit 1: Energy Returns and Oil Prices

Source: FactSet, as of 9/25/2023. MSCI World Index and MSCI World Index Energy sector returns with net dividends, 12/31/2021 – 9/22/2023. Indexed to 1 at 12/31/2021. Brent crude oil price, 12/31/2021 – 9/22/2023.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today