Personal Wealth Management / Market Analysis

From the Annals of Badly Constructed Indicators

Quantifying the unquantifiable leads investors astray.

With great computational ability comes the temptation to quantify and compute everything[i]-whether it makes sense to or not. To wit, major newspapers have digitized their catalogs stretching back over a century and made them publicly available-great fun!-but too-clever researchers have mined these archives, seeking to discover patterns they claim measure "partisan conflict" or "policy uncertainty." And lo, they found the Partisan Conflict Index (PCI) is near record highs-since 1890!-while the US's Economic Policy Uncertainty Index[ii] (EPUI) is coming off elevated levels but remains above its historical average (since 1985). The conclusion many draw: Presently high partisan conflict and policy uncertainty levels mean the ongoing bull market is sleepwalking its way to trouble. But there are a slew of flaws with these gauges and that interpretation. In our view, markets don't face the threat proponents presume.

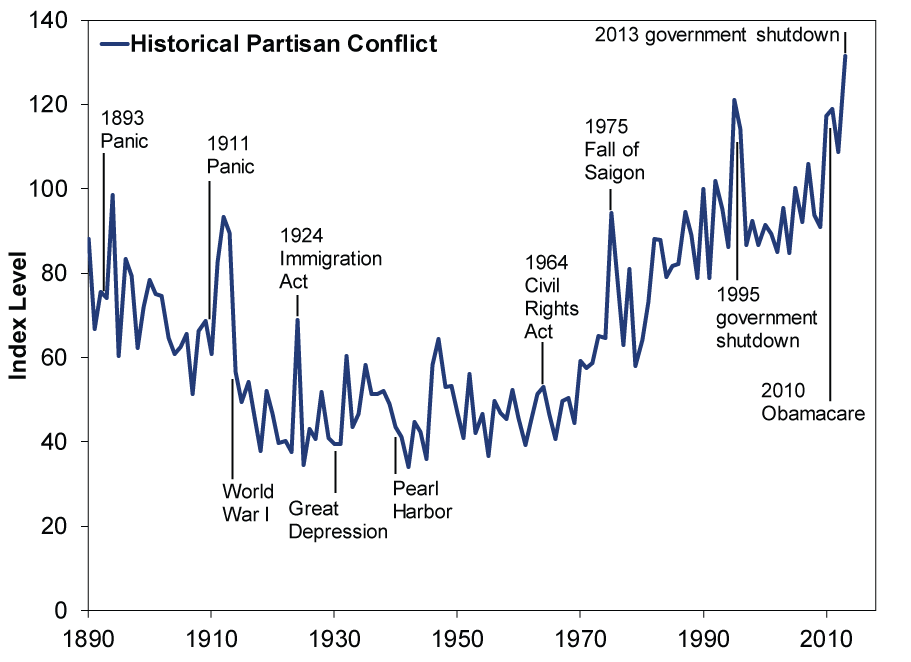

While we don't disagree partisan conflict is high now, it is worth wondering whether it is really a "record high." It's natural to think current events are more important and conflictier than the past-recency bias at work!-but it's also historically myopic. Is partisan conflict really higher than during the Civil Rights era (when the PCI was near its lows)? The 1960s Civil Rights debate was jam-packed with angst, including 1968's tumult and riots. While it wasn't purely partisan, it doesn't get much more conflicty ... outside war. Speaking of war, what about the Vietnam War era? It's hard to say the Vietnam-American War didn't divide the nation. (Relive the memories this fall!) While Nixon (and Ford) eventually got the US out of Vietnam-ending that conflict segment-Watergate was ongoing. Next to that, the Comey hearing is peanuts. (Exhibit 1)

Exhibit 1: More Conflictier Than ...

Source: marina-azzimonti.com, as of 8/1/2017. Historical Partisan Conflict Index, 1890 - 2013.

That's all within living memory for many. Let's go the other way. The Panic of 1893 gets overshadowed by the Great Depression, but 18.4% unemployment rates aren't anything to sneeze at. Populists-literally-threatened to bring down their capitalist oppressors. This culminated in 1896's heated realigning election (the capitalists held sway). What of the bimetallic movement? The Red Scares (1 & 2), including the McCarthy hearings? The point here isn't so much that today is more or less conflicted than then, but rather, a reasonable person should have questions about how this is measured and tallied.

Therein lies the rub. The index's problem is it doesn't measure partisan conflict so much as the media's coverage of it-and badly at that. Actual conflict and coverage of said conflict aren't the same thing. Index movements could just as well reflect the ebb and flow of Yellow Journalism. The PCI doesn't and cannot disentangle the two. That's because all it does is count keywords in newspapers. Words like "divided," "congress" and "partisan." This isn't measuring partisan conflict. It's what newspapers say about politics, and they aren't impartial bystanders. Selling advertising gives an incentive to drum up controversy. This is particularly true lately, considering the cutthroat competition for eyeballs in media. And media outfits are finding Trump is good for ratings. As a CNN supervising producer said in a recent hidden camera interview, "Trump is good for business right now." CNN's ratings are through the roof. Newspapers of record are enjoying a renaissance with Wall Street Journal and New York Times circulation enjoying a "Trump bump."

But beyond bias, it isn't clear how researchers accounted for syndication. With fewer and fewer papers generating unique content these days, this is a major issue skewing the entire dataset-and it could quite possibly generate false highs today. The EPUI uses the same methodology, with different keywords.[iii] Media reporting on these indexes of media mentions is an echo chamber: They are reporting on their own reporting.[iv]

A lot of this talk stems from the mistaken notion gridlock-and the attendant rhetoric-is bad. PCI and EPUI presume government getting along to go along is inherently good. But that's a fallacy! It says very little about actual policies' economic disruptiveness-what matters most for markets. Conflict or no, policy uncertainty occurs when the government DOES stuff: upending property rights; creating winners and losers; requiring businesses to adapt; driving unintended consequences, etc. And, heck, if politicians held hands, sang kumbaya and enacted the equivalent of the Smoot-Hawley Tariff Act of 1930, that would be bad! Ditto for SarbOx Part Deux. Cooperation on legislation doesn't mean good legislation necessarily results. So in a sense, to whatever extent conflict is high, it seems to us like a symptom of bullish gridlock blocking radical legislation. That's why these gauges have been high throughout this bull. The media-and these indexes-just aren't interpreting gridlock correctly.

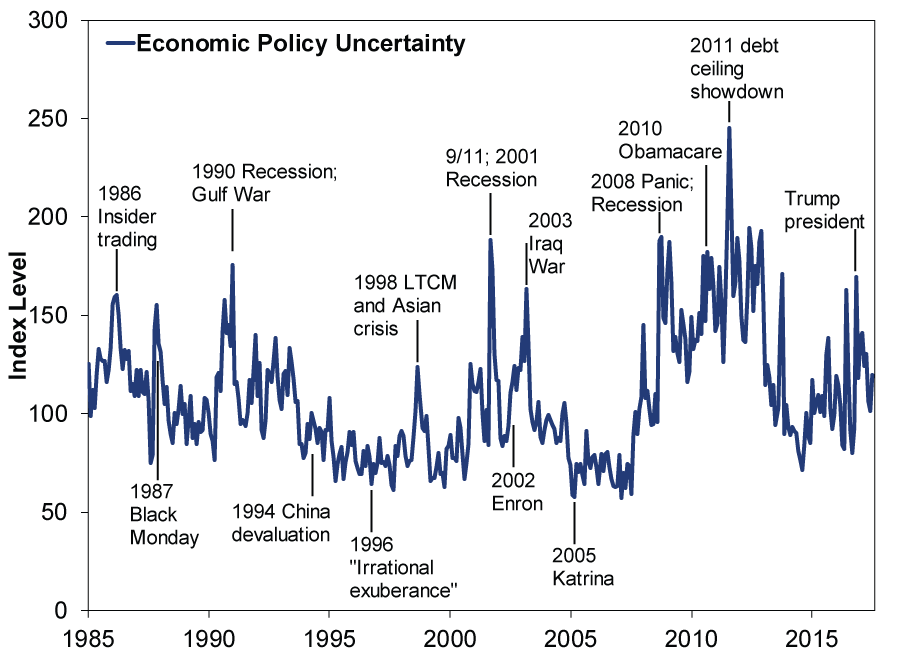

Exhibit 2: But You-and Markets-Knew That Already

Source: Economic Policy Uncertainty, as of 8/1/2017. Economic Policy Uncertainty Index, January 1985 - July 2017.

Heading into 2017, folks mostly hoped for or feared legislation galore from the GOP taking the House, Senate and presidency. But given internal party divisions and now evident intraparty gridlock, government has accomplished much less than expected-an underappreciated bullish factor for global stocks. Political conflict, partisan or otherwise, likely lowered policy uncertainty. Something the PCI and EPUI completely missed in their misguided effort to quantify the unquantifiable. In our view, markets yawning while such gauges claim uncertainty is high shows stocks care about likely outcomes, not word count.

[i] Not great responsibility, alas.

[ii] There are 21 of them for different countries, including "Global."

[iii] Such as "economic" and "uncertainty" in combination with other keywords like "white house" or "federal reserve." It also tacks on the number of federal tax code provisions set to expire and disagreements among economic forecasters. The former might be useful, but not without context and analysis. Forecasts (and disagreements about them) are useless.

[iv] It is unclear whether the index later captures the reporting on the index, which would fully make this a policy uncertainty or political conflict feedback loop.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Europe’s Resilient Q1 GDP2026-04-30

-

Economics Q1 GDP Reveals America on Firm Footing2026-04-30

-

Market Insights Ken Fisher on World Wars, Inflation, REITs and More – April 20262026-04-29

-

Market Analysis The Fed Is Close to a New Head2026-04-28

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today