Personal Wealth Management / Market Analysis

Greece Is Still the Word

Volatility is spiking as Greece's latest deadline approaches, but the longer-term risks for global markets likely remain small.

Greece's Parliament is having a rough week. Photo by Milos Bicanski/Getty Images.

Welcome, folks, to another critical week for the euro![i] In this week's installment, Greece is on the "brink of disaster." Eurozone officials have urged Greece to prepare for a "state of emergency if the government defaults, runs out of cash and stops paying civil servants. Greek PM Alexis Tsipras said the IMF bears "criminal responsibility" for the hardships wrought by austerity. Talks collapsed after creditors gave their allegedly final "take it or leave it" offer. Eurozone finance ministers meet for more talks Thursday , but German Finance Minister Wolfgang Schäuble said not to expect much. Greek officials warned they lack cash to pay the IMF by month's end, while Greece's central bank warned the nation could leave the eurozone and even the EU-but said only a "little ground" separates Greece and creditors. Then again, Tsipras warned Parliament Wednesday even that "little ground" might be an uncrossable pit and he "will assume the responsibility to say 'the great no' to a continuation" of austerity. Fin Min Yanis Varoufakis looked on while sitting cross-legged on the chamber's floor, head in hands. It is all increasingly bizarre and ever-more impossible to handicap. Will they kick the can? Give Greece just enough cash to get through this month or next? Or will we have default, capital controls and panic on the streets of Athens? No one can know, and we hope for the best for all involved. But as far as cold-hearted markets are concerned, the risks for global investors remain low regardless of what happens. Default and Grexit would probably make life even harder for Greeks in the near term, but probably not for markets globally. All signs indicate the risk of contagion remains minimal.

Markets are jittery right now, no question about it. German stocks, measured in euro, are in a correction. Eurozone stocks, also in euro, are close. US investors get a cushion from the stronger dollar, but even in dollars, eurozone stocks are down -4.8% since May 21.[ii] Peripheral bond yields are up since late May, when this bizarritude escalated, rising anywhere from 47 (Italy[iii]) to 82 (Portugal[iv]) basis points. Spreads over bund yields-widely considered a measure of investors' comfort with the periphery-spiked last Friday and Monday. All are consistent with swinging sentiment as the stalemate stiffens and tempers flare.

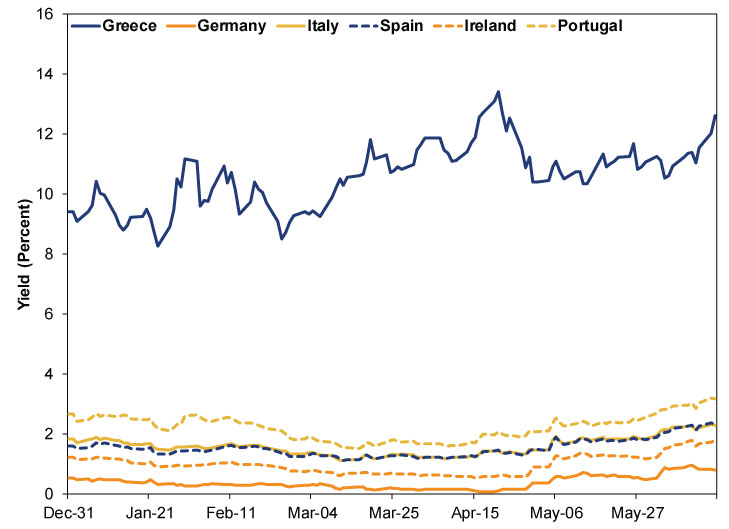

Take a longer view, however, and nothing seems fundamentally different. Eurozone and Greek officials have toed their uncrossable red lines for four months now. The June 30 deadline has been on the calendar since February. No one ever thought negotiations over unlocking aid would be a cakewalk. Headlines have warned repeatedly the standoff might prevail, leaving Greece to default suddenly, lose ECB support for banks, and pay civil servants with hot-off-the-presses drachma. Yet, even as these headlines swirled, yields didn't move much outside Greece (Exhibit 1). Yes, there was an uptick from late April onward, but this was part of a globalmove. A global move that included the US and Japan. We rather doubt investors' confidence in the full faith and credit in the US and Japanese treasuries has much to do with Greece.

Exhibit 1: 10-Year Bond Yields

FactSet, as of 6/16/2015. Benchmark 10-year government bond yields, 12/31/2014 - 6/16/2015.

If there were a risk of contagion here, we'd expect yields throughout the periphery to track Greek yields directionally. After all, similarly liquid markets digest all widely known information near simultaneously, and bond markets in Spain, Italy, Portugal and Ireland were well aware of everything that made Greek yields soar from late February on. Nothing here is sneaking up on them. They simply know Greece's problems are Greece's problems, not theirs. Hence why they track stable Germany, not shaky Greece.

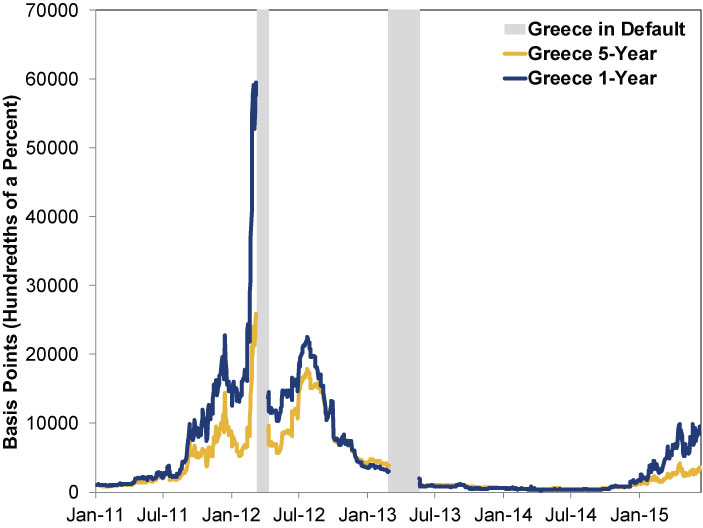

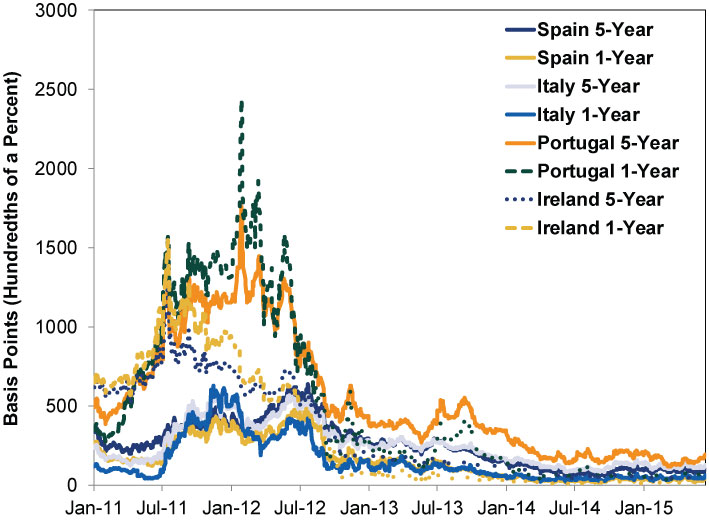

View credit default swap (CDS) rates, and Greece is even more of a sore thumb. CDS measures the cost of insuring debt against default. The higher the risk, the higher the cost. Greek CDS have soared. Swap rates for 1-year debt far exceed costs for 5-year debt, implying markets expect a credit event in the very near future. The same thing happened as Greece's 2012 defaults approached. Back then, peripheral CDS rose some, too-the eurozone wasn't fully backstopped, so contagion risk was greater. Today? They've barely budged.

Exhibit 2: Greece 1- and 5-Year CDS, 2011-Present

Source: FactSet, as of 6/16/2015.

Exhibit 3: Portugal, Italy, Ireland and Spain CDS, 2011-Present

Source: FactSet, as of 6/15/2015.

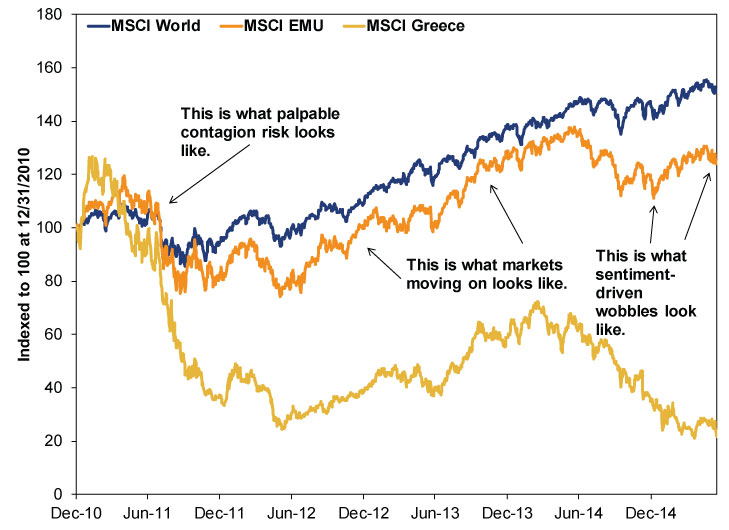

Same song, third verse when you consider stock markets. Even with recent volatility, today looks nothing like 2011, when contagion risk was higher. Then, eurozone and world stocks took it on the chin, suffering multiple corrections-including the steepest since the tumult surrounding Russia's default and the collapse of Long Term Capital Management in 1998. Since then, markets outside Greece have moved on. Greek stocks remain in a bear market, down nearly 77% since 2010's end.[v] But world stocks are just under all-time highs. Recent volatility reminds us of markets' jitters as Greece's prior government collapsed in late 2014. That wobble was fleeting as markets resumed looking longer-term. It is impossible to say when this wobble will end-short-term volatility is unpredictable-but we see no fundamental reason Greece should cause a material, longer-lasting decline now.

Exhibit 4: World, Eurozone and Greek Stocks

Source: FactSet, as of 6/17/2015. MSCI World Index, MSCI European Economic and Monetary Union Index and MSCI Greece Index returns with net dividends, 12/31/2010 - 6/16/2015.

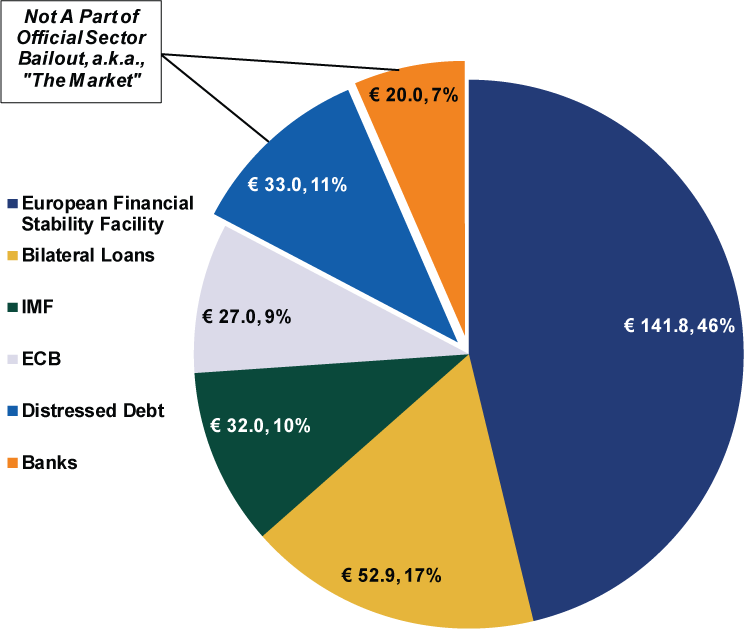

Why? Too small. As detailed here, with GDP around $200 billion, Greece lacks the power to delete a few trillion from global economic activity-and a few trillion is what a recession would require. Greece is roughly the size of Detroit, which defaulted in a year when US stocks rose 32.4%.[vi] Yes, Greece owes other entities money, and if it defaults, much of those IOUs turn to dust. But the impact is spread out, and the private sector is insulated. Officials have spent the last five years preparing for this, shifting the burden from banks to bailout funds. International banks own less than 20% of Greek debt-roughly $46 billion. Even if all of it is wiped out, that is a far cry from the nearly $2 trillion in writedowns US banks suffered in 2008. As shown in Exhibit 5, the official sector-ECB, IMF and eurozone governments-own the bulk.

Exhibit 5: Who Actually Owns Greek Debt

Source: Bank of International Settlements, Bank of Greece, as of 4/8/2015.

They have already spent the money, and we have a hunch they have already at least mentally accounted for this as a sunk cost. When you scale the numbers, these become small sunk costs. The €56 billion Greece owes Germany is 1.6% of German GDP. France's €42 billion IOU is 1.7%. Italy's €37 billion is 1.9% of GDP. Spain's €25 billion is 2%. The €34 billion owed the rest of the crew is 1.3% of their aggregate GDP. The ECB's €20 billion Greek debt stake is just 0.8% of total assets. Yes, there is the issue of recapitalizing the eurozone's bailout fund if Greece defaults on its official creditors, but the amounts in question are small, and it needn't be replenished overnight. Not with Greece the only eurozone nation on the brink.

We aren't saying a messy default-as in a sudden "sorry, we ain't paying," rather than the planned orderly restructurings of 2012-would have zero market impact. It could easily stoke volatility, maybe a correction. Maybe not! Ditto a Grexit. Volatility is unpredictable, and corrections can strike at any time. But corrections aren't bear markets, and the chance of Greece causing a bear market seems as slim as ever.

[i] We also like the term coined by Germany's Handelsblatt, run through Google Translate: Greece Destiny Week.

[ii] FactSet, as of 6/16/2015. MSCI European Economic and Monetary Union returns with net dividends, 5/21/2015 - 6/16/2015.

[iii] FactSet, as of 6/16/2015. Italy benchmark 10-year government bond yield, 5/28/2015 - 6/15/2015.

[iv] FactSet, as of 6/16/2015. Portugal benchmark 10-year government bond yield, 5/22/2015 - 6/15/2015.

[v] FactSet, as of 6/16/2015. MSCI Greece returns with net dividends, 12/31/2010 - 6/15/2015.

[vi] FactSet, as of 6/17/2015. S&P 500 Total Return Index, 12/31/2012 - 12/31/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today