Personal Wealth Management / Market Analysis

Italy Doesn’t Need the ECB’s QE

Central bank bond purchases aren’t the only thing standing between Italy and a debt crisis.

A new theory about the ECB emerged on Wednesday, and it is a juicy one: Evidently, the ECB can’t hike rates aggressively because it has committed to not raising rates until it stops quantitative easing (QE) bond purchases. Which it can’t do, because it would risk restarting Italy’s debt crisis. While we won’t opine on the need or desirability of aggressive ECB actions, we have a couple of charts that disagree with the notion ending QE would trigger an Italian debt calamity.

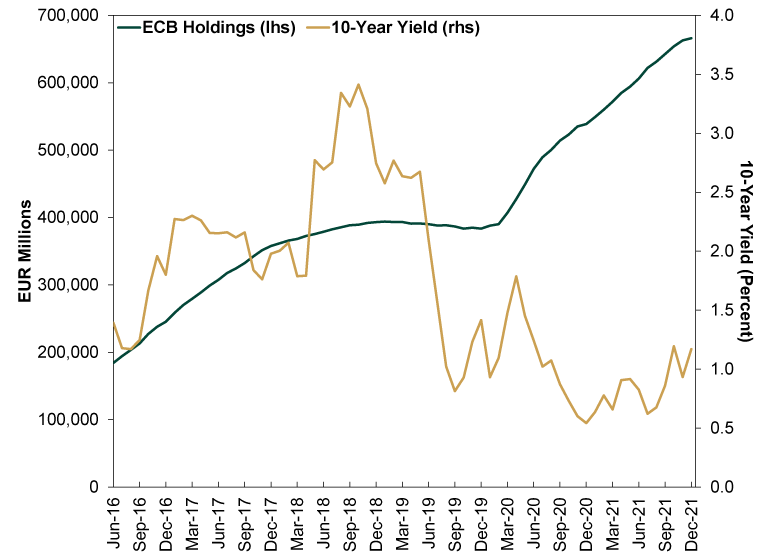

Analysts have long argued the ECB alone is propping up Italian debt and keeping yields low. Never mind that Italy’s 10-year yield was well below crisis-era levels when the ECB started QE in January 2015. Never mind that in 2014, the average yield of all Italian bonds issued that year was just 1.35%, which was then the lowest on record.[i] And never mind that when the ECB stopped buying bonds in 2018, Italian yields fell on a cumulative basis. (Exhibit 1)

Oh, and never mind that even when the ECB stops buying Italian bonds whenever QE ends, it will still own over €650 billion (and counting) worth of them, and the Italian Treasury will still get back any interest paid on those holdings.[ii] As those bonds mature, the ECB will use the proceeds to buy replacements. The pile of debt Italy will actually have to pay interest on is smaller today than it was when the ECB started QE, as its total Italian bond holdings dwarf the amount of debt Italy issued since QE began. Those who dwell on the act of purchasing overlook that the stock of assets on the ECB’s balance sheet is probably more meaningful at this point.

Exhibit 1: ECB Bond Purchases and Italian Bond Yields

Source: FactSet and ECB, as of 2/16/2022. Italian securities held for monetary policy purposes and Italian benchmark 10-year government bond yield, month-end levels, June 2016 – December 2021.

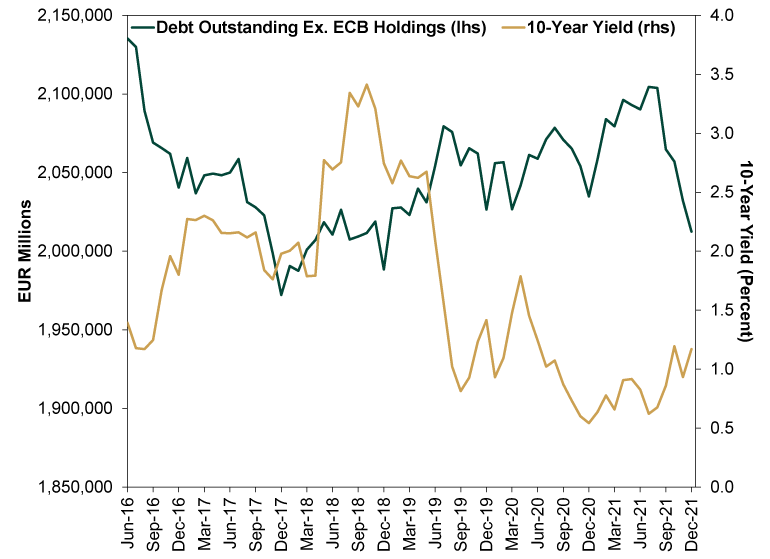

Bond prices (which move opposite yields) move on supply and demand—like all market-set prices. As Exhibit 2 shows, even when Italy’s Treasury did manage to increase bond supply for a few years despite the ECB’s purchases, yields mostly went down. That, in our view, suggests demand is off the charts, which doesn’t surprise us—there is a dearth of relatively high-yielding, quality developed world sovereign debt these days. Pension funds are desperate to get their mitts on well-paying bonds. So are other institutional and individual investors—particularly in Italy, where the investment culture is much more bond-oriented than in the US. We think it is fair to argue the market is trying to tell the ECB and Italian Treasury that bond supply is just too low.

Exhibit 2: The Incredibly Shrinking Italian Bond Supply

Source: FactSet and ECB, as of 2/16/2022. Italian government debt outstanding minus Italian securities held for monetary policy purposes and Italian benchmark 10-year government bond yield, month-end levels, June 2016 – December 2021.

Here is a theory we haven’t seen elsewhere: When the ECB stops buying Italian bonds, it will clear some space in the marketplace for other investors who are eager to buy. Supply will still be limited, due to the mountain of bonds gathering dust on the ECB’s balance sheet, but at least the central bank won’t be gobbling up every bond in sight. If yields rise, it will present a discount that lures more buyers in. That pool of buyers may be quite large, as Italian 10-year yields are now almost even with US Treasury yields for the first time in over a year. All else equal, money flows to the highest-yielding asset. Yes, there are some caveats for creditworthiness, but the Italian government hasn’t been spendthrift for many years, and as we showed two months ago, its debt service is quite manageable. Sentiment is far out of touch with reality.

Debt crises happen when governments can’t find buyers. That happened to Greece a decade ago. It happened to Ireland and Portugal then as well. But it never happened to Italy (nor Spain) during the eurozone’s debt crisis. People live-blogged every debt auction with a spirit of schadenfreude, seemingly almost willing them to fail for the sake of a juicy headline—but not one auction flopped. There were buyers throughout, and high yields brought risk-taking folks out of the woodwork. If Italy didn’t fail to refinance debt then, when the entire world seemed to fear the eurozone was going to collapse, we doubt it will have problems whenever the ECB stops increasing its stockpile. The market appears to be telling us this—time to listen.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today