Personal Wealth Management / Financial Planning

Non-Traded REITs Are No Treat

Want real estate exposure? These are your worst option.

Although US capital markets were pretty developed in the mid-20th century, one sector was still tough for the little guy to break into-real estate, where access generally required buying whole buildings or properties. So in 1960 Congress created Real Estate Investment Trusts (REITs), which offer ownership of large, income-producing real estate ventures to the investing public in tradeable share form. Investors were jazzed! By law, REITs are taxed specially-if they pay out at least 90% of their income to shareholders, the REIT isn't taxed at the corporate level. That can mean high "dividends," sometimes with special tax wrinkles. These perks aren't as great as they look, for reasons I'll get into, but let's not quibble-if the mission was to open the gated community[i] of real estate investing to all, well, mission accomplished. REIT shares today are highly liquid, traded on public exchanges and more or less function as stocks. In fact, in September they'll say goodbye to their longtime home as a community in the Financials sector, and bravely venture out as their own, independent Real Estate sector.

So far, so successful. But there is another, shadier type of REIT-the non-traded kind. They're touted as exclusive opportunities, even higher-yielding than their boring cousins (4-6% vs around 3%) and a hedge against volatility. Which might sound great, but this kind of pitch-higher than market yields with presumably less volatility-is a red flag of epic proportions. Sure enough, non-traded REITs are chock full of downsides, restrictions and caveats that catch many investors by surprise. They are The Money Pit of investment products.

For starters, they aren't traded on public exchanges. Instead, they're often sold by independent dealers, who may in turn contract with outside parties who sponsor, advise on, manage or market the product. Predictably, they cost a lot: Fees can run as high as 15% all told, which should take the shine off those extra-high dividends. What if you want to sell your chunk of a non-traded REIT before the end of the up to eight year-long holding period? Sorry, but since they aren't traded, finding a ready buyer is tough. The original seller can take it off your hands, but only for a steep discount-up to 10%.

What say you hang on until the real estate is sold or the company goes public, allowing investors to finally cash out-is this where the bonanza happens? Not necessarily. Markets being what they are, sometimes the shares lose value, undercutting promises of safety and low volatility. After FINRA mandated in 2012 that non-traded REITs occasionally update share values, many reported steep losses. And since they aren't traded, even those updates are only estimates-the final value can and does differ upon liquidation. Take Columbia Property Trust, which revealed losses of 27% once it went public and trading began. Or American Realty Capital, which went public last June, and was down 30% a few months later. These aren't isolated examples: Multiple studies suggest non-traded REITs return several percentage points less than their conventional traded brethren.

This underperformance has weighed on their popularity, as has new scrutiny of fees and transparency from the Department of Labor and FINRA, plus scandals at some of the industry's biggest firms. Sales grew rapidly between 2010 and 2013 to a peak of $20 billion, but may fall as low as $5 billion this year. Nonetheless, plenty of investors still own them, often in large amounts.

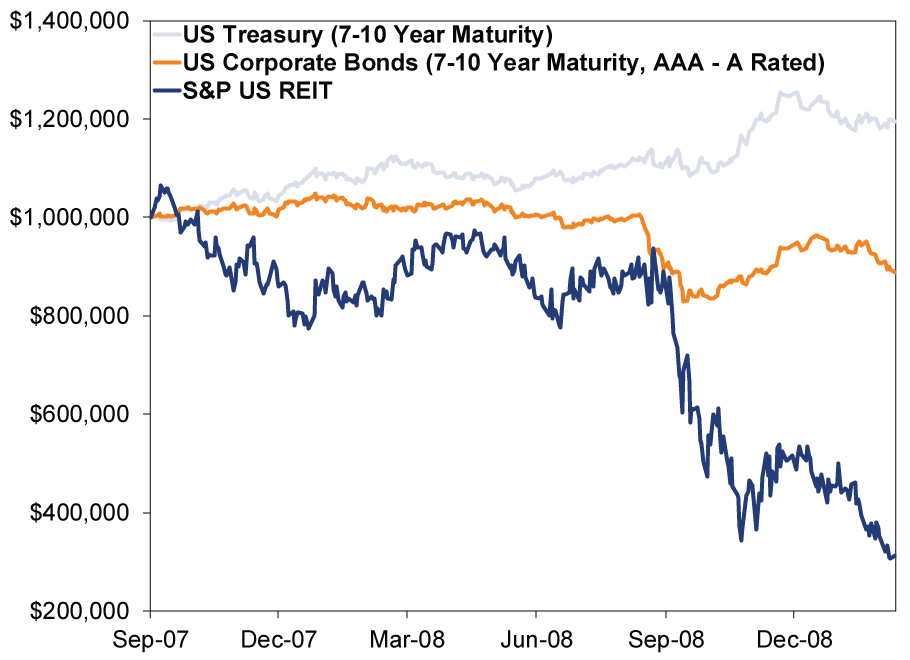

Today's low-interest rate environment is a big reason why-as the global pile of negative-yielding debt tops $10 trillion, many are searching for higher-yielding alternatives to fixed income. But this mistakes bonds' purpose in a portfolio-to cushion against stocks' volatility, not drive growth. Piling into a narrow investment category like real estate, whether in the form of traded or non-traded REITs, is a recipe for regret. High dividends are paid out at the discretion of the issuer-cuts and cancellations are always possible, as evidenced by chilling tales of "zombie REITs" that tie up investor funds even as they slash payouts. The risk rises when commercial real estate prices dip-which, like any other asset, they are liable to do occasionally. Fact is, REITs are, for all intents and purposes, stocks. That is why they are included in equity indexes. (Soon as their own sector!) REITs, regardless of yield, aren't bonds-they behave like stock investments, and are far more volatile than either corporate or Treasury bonds. As this chart shows, they don't protect against market downturns either. (Since non-traded REIT values are tough to pin down, the graph shows traded REITs as a proxy.)

Exhibit 1: Real Estate Volatility vs Fixed Income - 9/30/2007 - 3/9/2009

Source: FactSet, as of 8/15/2016. Estimated impact of $1 Million invested in the BofA Merrill Lynch US Treasury 7-10 Year Index, the BofA Merrill Lynch US Corporate 7-10 Year Index and the S&P United States REIT Index, 9/28/2007 - 3/9/2009.

Clearly, dividends alone don't make an investment bond-like-and for non-traded REITs, dividends are particularly suspect. Even though the underlying properties may take a while to start producing income, the companies often simply start returning invested money in the form of dividends. Are these payouts tax-free? Maybe. But that money was already tax-free when it sat in your bank account-and now that it's returned to you in the guise of a dividend, the REIT has less money to invest in, you know, actual real estate. Investors may not know it, but those payments threaten long-term returns. When the REIT hands you back your money, it can't reinvest in its own business.

Rather ironically, the high cost and illiquidity of non-traded REITs are a throwback to pre-1960 days, before Real Estate Investment Trusts came along. Thankfully, times have changed. Gaining exposure to building and property values doesn't have to be expensive, cumbersome and unduly risky. Of course, no investment is perfect-traded REITs are no exception, so don't overload, and make sure they fit in with your investing goals and needs. Treat them as an equity sector like you would, say, Industrials. But no matter your goals,[ii] non-traded REITs just don't stack up.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today