Personal Wealth Management / Market Analysis

One Month After First Republic, Fed Borrowing Is Quiet

Fed borrowing was flat last week.

Since Silicon Valley Bank and Signature Bank failed two and a half months ago, we have kept a close eye on banks’ Fed borrowing for signs of continued stress. In the immediate aftermath, we noted a spike, with the borrowing concentrated in the New York and San Francisco Fed districts—homes to Signature and Silicon Valley Bank, respectively, as well as fellow struggling West Coast regional First Republic. To us, this geographical limitation—as well as the rather small amounts in question, once you scale relative to the size of the US economy and banking system—showed rumors of a systemic crisis were greatly exaggerated, presenting a big gap between sentiment and reality to propel stocks.

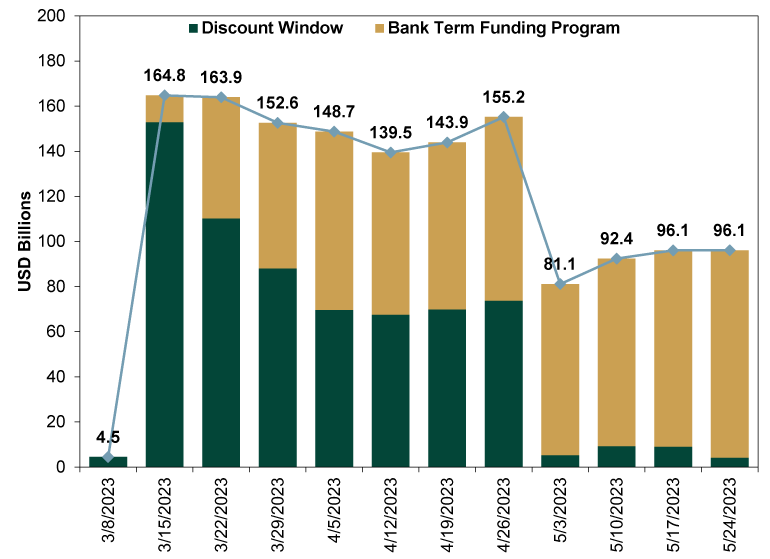

Since then, things have quieted further. Exhibit 1 shows total bank borrowing from the Fed via its traditional discount window and new Bank Term Funding Program (BTFB), the temporary lending facility for regional banks created when Silicon Valley and Signature Banks failed. Total borrowing plunged in May, even as First Republic went under, and after a slight uptick mid-month it flattened out.

Exhibit 1: Total Emergency Fed Loans to Banks Outstanding

Source: Federal Reserve, as of 5/31/2023. Hat tip: Fisher Investments Research Analyst Davis Zhao.

Now, current discount window usage is down to just $4 billion, back below pre-Silicon Valley Bank levels. BTFP borrowing is elevated, but we hesitate to see that as a sign of stress. That program offers favorable rates compared to the official fed-funds target range, which may be enticing borrowers. It also allows borrowers to pledge collateral at par value, rather than mark-to-market values, creating easier terms overall. Lastly, they are one-year loans and, despite penalty-free repayments, may be sticky as banks take advantage of the favorable terms to preserve liquidity. That seems more like prudent financing and risk management than a panic move. But at any rate, at just 0.5% of bank deposits, it is hardly a huge amount.[i]

While this is just a small post script on the springtime regional banking tremors, we think it underscores that markets were rational to move on as quickly as they did. Loads of commentators said otherwise, fearing far worse to come. But the data arriving since suggest stocks accurately assessed the size and scope of the problem and resumed their day job of pricing in corporate earnings over the next 3 – 30 months.

[i] Source: Federal Reserve, as of 5/31/2023.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, US Q2 GDP, Eurozone Inflation

2026-07-27

2026-07-27 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 20 - July 242026-07-27

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today