Personal Wealth Management / Market Analysis

OPEC’s Target Cut in Perspective

Global supply is up big this year despite OPEC’s failure to meet production targets.

The good kind of volatility returned Monday as the S&P 500 jumped 2.6% to start Q4.[i] But stocks weren’t the only thing that rose. Crude oil prices also jumped, tied largely to rumors that OPEC and its partners are considering reducing their production target by a million barrels per day (bpd) at this week’s meeting. Cue fears of a big cut fueling (sorry) another spike in oil prices, exacerbating this year’s inflation and compounding extant economic headwinds. This is understandable from a sentiment perspective and right in line with the fears driving this year’s bear market. Yet we also think it is quite out of step with oil supply and demand, not to mention how oil prices have behaved since spiking as Vladimir Putin invaded Ukraine.

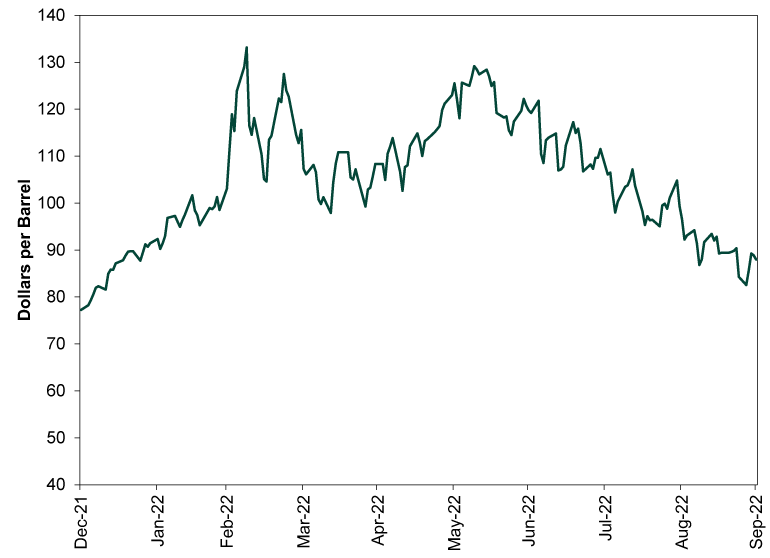

Exhibit 1 shows global oil prices this year to date. As you will see, crude rose in the run-up to the invasion and spiked just afterward, reaching its year-to-date high on March 8. That, you might recall, is the day the UK announced its decision to ban Russian oil imports, heightening fears of a sudden supply crunch. But since summer, oil has declined steadily as it became apparent that Russian oil was finding buyers and global supply was resilient. Oil prices now sit right around pre-Ukraine war levels.

Exhibit 1: Brent Crude Oil in 2022

Source: FactSet, as of 10/3/2022. Brent crude oil spot price, 12/31/2021 – 9/30/2022.

Based on our read of sentiment, oil’s decline isn’t widely appreciated. We suspect that is because earlier high oil prices are still feeding into consumer price inflation—not just from the comparison with lower fuel and energy prices a year ago, but from all the consumer products that include petrochemical feedstocks. The production economy has had a lot to swallow this year, and not all companies passed those costs onto consumers immediately. So when consumers hear about oil production target cuts and the potential for rising prices, it is very easy to mentally layer that on top of the current inflation rate and presume it will keep accelerating indefinitely, not accounting for the disinflationary forces that have been at work since summer.

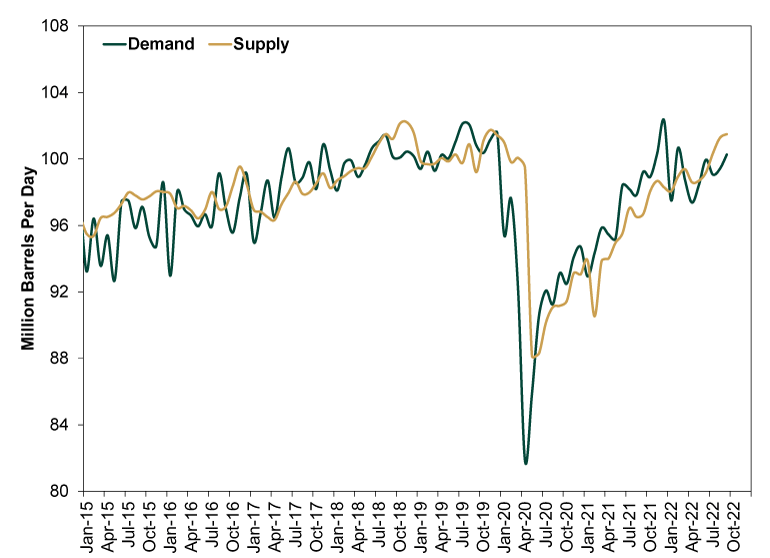

Then again, we think it is a stretch to extrapolate mooted OPEC production target cuts to an oil price spike. Like all assets, oil moves on supply and demand. As Exhibit 2 shows, supply has outstripped demand for a few months now, to the tune of about 1.3 million bpd in September. That figure is less than OPEC’s rumored cut. It seems like the cartel may be aiming to put a floor under recently declining prices. That might end the recent slide, but it doesn’t mean another spike, especially with consumption down from last autumn’s high, when the world was gobbling up oil as a replacement fuel when European wind production tumbled and coal was in short supply in China.

Exhibit 2: The World Has an Oil Surplus

Source: FactSet, as of 10/3/2022. Monthly global oil supply and demand, January 2015 – September 2022. HT: Fisher Investments Research Analyst Ori Powers.

Note, too, that supply has risen (and prices declined) despite OPEC’s chronic failure to meet its targets. Yes, failure. According to a widely reported leak of some OPEC internal documents, OPEC and its partners (including Russia and others) missed August’s production target by 3.58 million bpd.[ii] That is even worse than July, when production was reportedly 2.9 million bpd before the target due primarily to attacks on Nigeria’s oil infrastructure and Russia’s production cuts in the wake of sanctions, and it extends a long-running miss. Cutting a target, which is what is under discussion, is very different than cutting actual output. If anything, it just brings the target a tad closer to where production actually is, making the miss slightly less embarrassing.

OPEC always hogs the world’s attention, but that seems mostly a relic of the 1970s, when the cartel had real power to control supply. That was before the shale boom, when US production surged, leading to a global supply glut in the mid-2010s that the world took a few years to work off. It also took US oil producers several years to work through that era’s over-investment and debt accumulation, which is one reason why they have been slower to ramp up this time around. But US production is nevertheless up, from a pandemic-era low of 9.7 million bpd in May 2020 to a post-pandemic high of 11.8 million in July, the latest data available.[iii] The US oil industry, unlike OPEC, doesn’t operate by administrative fiat. It lives in the private sector, with even drilling on federal lands far less subject to the government’s whims than coverage on both sides of the political aisle suggests. With domestic oil rig counts up by over 100 this year to date, production likely continues rising, potentially counterbalancing any actual OPEC production cuts from here.[iv]

In our view, oil prices aren’t a fundamental stock market driver. Oil and stocks move concurrently, as all similarly liquid assets do, digesting the same information concurrently. One doesn’t predict the other. But oil prices have affected sentiment this year, so from that standpoint, falling uncertainty in the oil world probably benefits stocks as it gradually arrives. The more the world sees supply and demand staying roughly balanced despite OPEC’s rumblings, the more we should get that falling uncertainty.

[i] Source: FactSet, as of 10/3/2022. S&P 500 Index price return on 10/3/2022.

[ii] “OPEC+ Is Now 3.6 Million BPD Below Its Oil Production Target,” Tsvetana Paraskova, OilPrice.com, 9/19/2022.

[iii] Source: US Energy Information Administration, as of 10/3/2022.

[iv] Source: FactSet, as of 10/3/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today