Personal Wealth Management / Market Analysis

Our Take on Tuesday’s Sharp Swings and CPI

Staying cool and thinking longer term are vital at times like this.

Stocks’ rocky 2022 certainly continued Tuesday, as the S&P 500 fell -4.3%—with most blaming disappointing inflation data.[i] But in our view, the large drop extends this year’s one constant: Sentiment seems detached from reality. While we don’t deny the pain of higher prices and interest rates—and negativity like Tuesday’s can sting—investors’ moods and reactions to incoming information seem overall too dour relative to the observable facts on the ground. In our view, Tuesday’s August US Consumer Price Index (CPI) report provides a timely example. Headline CPI decelerated, albeit less than expected, but an acceleration in “core” CPI, which excludes food and energy, triggered more handwringing over a potential 75 basis-point Fed rate hike later this month. Even though investors have been penciling in that large of a Fed rate hike for several weeks now. When stocks sink on emotional flashpoints rather than a materially negative shift in incoming information, we think it is a strong signal that staying cool remains the wisest move.

The CPI report itself held few new or surprising insights. The headline reading slowed from 8.5% y/y in July to 8.3%, missing expectations for 8.1%.[ii] The 0.1% month-over-month increase sped from August’s flat reading but remains below the long-term monthly average.[iii] Yet, extending August’s trend, falling gasoline prices drove much of the deceleration, masking continued price increases elsewhere. Those were more apparent in core CPI, which accelerated from 5.9% y/y to 6.3%, with the month-over-month change speeding from 0.3% to 0.6%.[iv] That may seem sharp, but the month-over-month figures have been quite volatile throughout this high-inflation stretch, and extrapolating any of them forward—whether they were faster or slower—would have been an error. Such is the nature of monthly data.

Much of today’s coverage tried to dig deeper, leading to conclusions that August’s results show inflation is stickier than first expected—hence all the talk of big Fed rate hikes to come. In our view, this is a philosophical error. You can’t look to current price moves to predict future price moves. Looking at CPI’s various subcategories can help identify trends, but these are generally backward-looking. For instance: It is probably fair to conclude that, with core services and core goods measures accelerating, higher energy and petrochemical feedstock costs are starting to bleed through into consumer prices … to some extent. That delayed reaction isn’t surprising, given producers will hedge these costs and try everything possible to avoid passing them to customers, lest they lose market share by reacting to temporary surges in commodity prices. (And it seems like a stretch to connect those theories to shelter, which was the single largest contributing category to the monthly rise, beyond the fact that many rental agreements include utilities.) But this isn’t guaranteed to continue indefinitely, especially with most US energy prices trickling downward more recently. Said differently: Just because core prices tend to be overall less volatile than headline prices doesn’t mean every move is part and parcel of a long-term trend.

Another thing about prices: To the extent monetary policy affects them, it usually happens at quite a lag—anywhere from 6 to 18 months or so, depending on the study in question. Therefore, the argument that August’s inflation data necessitate more Fed rate hikes doesn’t hold up. The Fed started hiking this past March, and even then, the increase was only incremental. We wouldn’t expect the totality of this year’s rate hikes to have an effect on inflation readings until sometime next spring or summer. So from that standpoint, we guess we can understand the concern about more big Fed moves from here: If the Fed continues reacting in a big way to incoming data rather than taking a more measured, long-term approach, then it raises the likelihood of overshooting. But also, we are skeptical that this became far more likely today than it was yesterday. Actually, we are skeptical that the probability is calculable, period—in our experience, Fed moves are unpredictable. Fed people talk a lot but often change their minds. They interpret data in unexpected, counterintuitive, rather bizarre ways and vote by consensus. They pledge to stop issuing forward guidance and then continue issuing forward guidance. They do what they do when they do it.

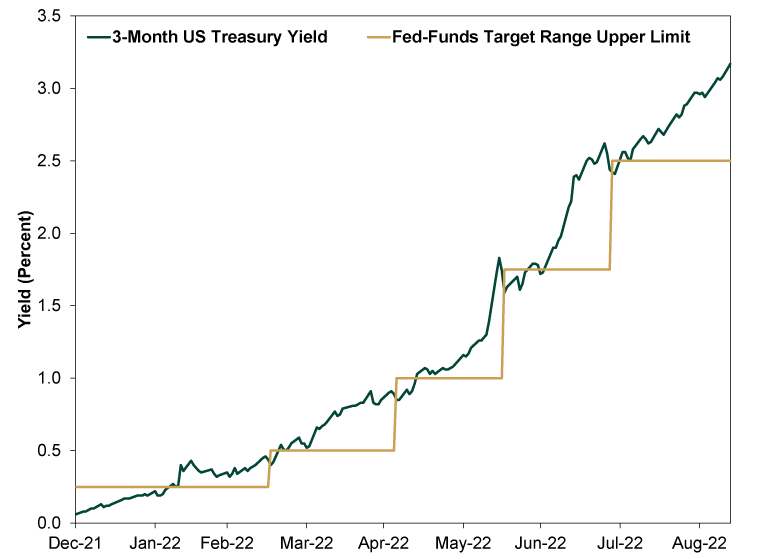

At the same time, the market has been predicting a big Fed move for some time. Throughout this rate hike cycle, the 3-month US Treasury yield has risen in advance of Fed rate hikes and generally reached the new upper bound of the fed-funds target range before the Fed officially raises it. The 3-month yield closed Monday at 3.17%, which is 67 basis points above the fed-funds target range’s current upper limit.[v] If the history in Exhibit 1 is at all a reliable guide, it suggests markets have been pricing in the likelihood of a three-quarter-point Fed move since the last meeting in July. If the Treasury market has been able to digest this information, it stands to reason that the equally efficient and liquid stock market has already done the same.

Exhibit 1: The Remarkably Prescient Treasury Bill Market

Source: FactSet, as of 9/13/2022. 3-month US Treasury yield (constant maturity) and fed-funds target range (upper bound), 12/31/2021 – 9/12/2022.

Rather than trying to determine future Fed moves, we suggest focusing on sentiment, which we think has been the primary negative influence on stocks this year. Inflation dread is a primary contributor to that, as it feeds into Fed fears. So, if inflation moderates over the period ahead—despite wiggles along the way—then it probably points to improving sentiment. We see a high likelihood of that happening. Fisher Investments founder and Executive Chair Ken Fisher catalogued a bunch of factors pointing to moderate inflation in his latest column for Real Clear Markets, and if you haven’t yet read it, we think it is well worth doing so after you are done here. But in short, between falling food and energy commodity prices, slowing money supply growth, falling gas prices, the big moderation in Purchasing Managers’ Index price gauges, falling shipping costs and a nascent drop in housing costs, there are ample reasons to think the inflation rate is set to slow, gradually and irregularly, over the foreseeable future.

So think longer term, both now and as data and markets wobble from here. Nothing moves in a straight line, be it inflation data or a stock market recovery. Even a new stock market low is possible if sentiment stays bad enough for long enough. But new bull markets usually begin when investors think any light at the end of the tunnel must be an oncoming train, and that mentality reigns today. That suggests a recovery—a new bull market—is close by, if it isn’t already underway.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today