Personal Wealth Management /

Q the End

With each US economic data release come more predictions of when the Fed will taper QE. But will “when” matter for stocks, and why?

These days it seems everyone is trying to nail down the date QE will end. Some may even be trying to time it in their portfolios. In my view, they’re doing so in vain, and possibly to their own detriment. It’s nigh on impossible to game when QE will end, and no one knows how markets will react following its decision. More importantly, when QE ends isn’t what matters for stocks in the mid to longer term—how the economy responds in the months and quarters after is much more important.

Considering how dour most investors are on QE’s end, many may expect markets to sink when tapering starts. Some might even try to sell out before the Fed tapers to avoid taking the paper hit. Yet trying to time QE is trying to predict and time short-term market swings—no one can do it with precision (unless by sheer dumb luck). Take September: Then, investors were sure the Fed would announce the taper at its September 18 meeting. But they were wrong—QE stayed at full speed. And those who sold out beforehand thinking they were avoiding a surefire correction avoided a big jump instead.

There is no guarantee markets will swing one way or another when QE finally ends. It seems logical to assume markets would pull back some: Many investors think stocks and the economy are addicted to QE. Our research shows that isn’t true (more on this in a bit), but in the short term, emotions rule. Like Ben Graham said, in the short-term markets are voting machines—immediately after QE ends, investors could very well register their displeasure. Then again, there is a reason my boss, Ken Fisher, calls the stock market The Great Humiliator. Stocks love throwing out people’s expectations, and most seem to expect a correction or worse post-QE. Plus, markets are forward-looking—they’ve been digesting QE’s end since taper became the financial buzzword of 2013. Those trying to guess one way or another could miss opportunities if they guess wrong, never mind the trading and commission fees.

Moreover, how stocks move immediately after QE ends doesn’t determine whether QE’s end will be good or bad for markets over time. Sentiment-driven short-term moves don’t determine long-term market direction—over time, short-term blips even out as markets weigh fundamentals. These days, US and global fundamentals might not seem smashing at first blush, but they’re overall far better than many realize. Global yield spreads continue widening—an almost universally accepted bullish feature, yet little appreciated by investors today, who fear rising long-term interest rates. Most Leading Economic Indexes globally are rising, too, with the US and UK particularly hot, and widening yield spreads are a big reason why. In the last 50 years, no recession has started amid a rising LEI trend—and they typically don’t start until after LEI has fallen for some time. Overall, with renewed growth in the eurozone, faster growth in the UK and reacceleration in many Emerging Markets, the global economy is gathering steam, yet investors are bracing for a slowdown—faster growth seems like a strong potential positive surprise.

Why have yield spreads and LEIs been rising? Hard as this is for most to believe, it largely owes itself to taper talk. That’s right—“QE is ending soon!” is another bullish feature. Last spring’s taper talk caused long rates to rise in anticipation of less yield-depressing bond buying. Wider yield spreads measure the gap between banks’ funding costs and their interest revenues on longer-term loans, so wider spreads allude to more profitable lending. The Fed launched QE to boost lending—the logic being lower long-term interest rates will make credit more affordable for businesses and individuals, boosting demand for loans. But lower long-term interest rates mean banks make less money on outstanding loans, while the amount of risk each loan comes with stays the same. That hits supply. In this environment banks aren’t lending as much as they would if interest rates were higher—the risk-reward trade-off isn’t worth it!

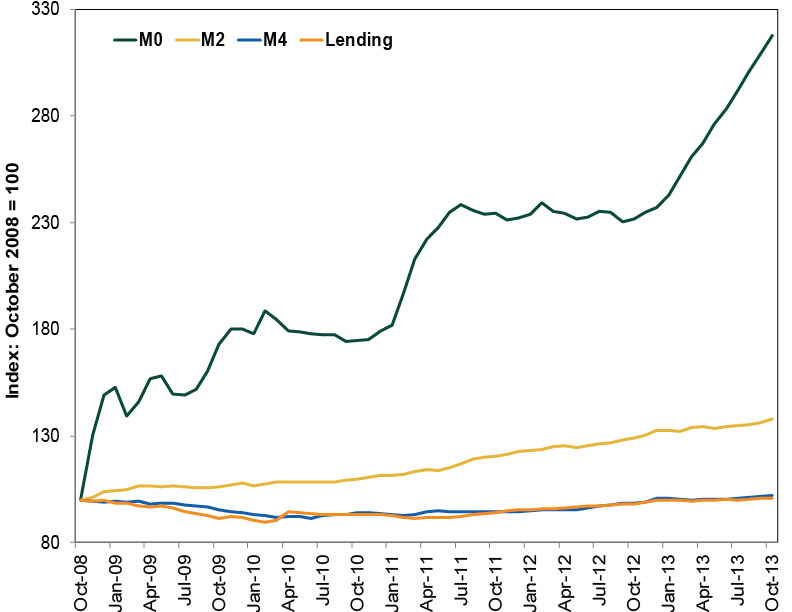

Credit has incrementally increased despite QE, and money supply growth is painfully slow. The monetary base (M0) has exploded since QE began—up over 200%. Money in circulation (M2), however, is only eking higher, up just 37%. The broadest measure of money, M4, is just about flat and spent a significant period in contraction. (Exhibit 1)

Exhibit 1: Cumulative M0, M2 and M4 Growth since QE Began

Sources: Federal Reserve Bank of St. Louis and Center for Financial Stability, as of 11/27/2013.

When the Fed flips the switch, rates likely rise further, encouraging banks to lend even more. More money circulating through the wider economy means more business activity—good for earnings and revenues. Proof lies overseas: The UK economy has accelerated since QE ended there. Its M4 has accelerated strongly in recent months! This after choppy data and anemic M4 growth (including a two-year, £149 billion fall) during nearly four years of QE. The US, already in better economic shape, should follow suit.

But barely anyone believes this! Many expect the economy to crater when QE ends. Continued growth alone would be a big surprise—an acceleration might knock people over. This is why QE’s eventual end should be extremely bullish. A gap between too-low expectations and pretty darn strong reality creates a wall of worry for stocks to climb—the wider the gap, the higher the climb. When QE ends and investors gradually realize long-term asset purchases weren’t driving US economic expansion, their confidence likely rises and they’ll adjust their bets, paying more for future earnings.

This bounce won’t happen overnight. It’ll take time for investors to see the economy can do fine without the Fed’s “assistance.” But for long-term investors, positioning for where you expect stocks to be over the next 12-18 months, based on fundamentals, makes much more sense than trying to time a short-term emotional reaction that may or may not happen.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Pumping Up the Yen?2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today