Personal Wealth Management / Market Analysis

Red Sea Update: Shipping Costs Show Signs of Corporate Adaption

The Baltic Dry Index is rather calm these days.

The Red Sea remained a hot topic this week, with analysts continuing to speculate about the economic impact from ongoing attacks on the important shipping lane and Suez Canal conduit. In the past few days alone, analysts have blamed the situation for Germany’s Q4 GDP contraction, weak eurozone manufacturing PMIs and more. Yet away from the spotlight, we see mounting evidence that companies have already adapted.

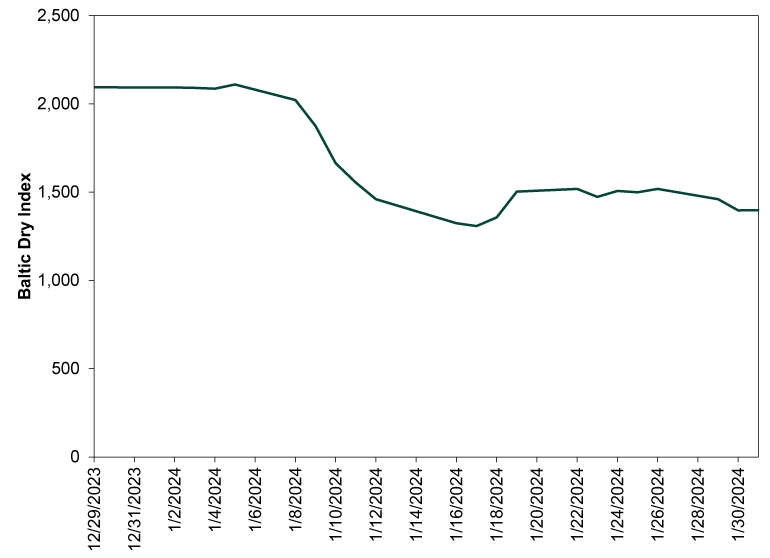

That evidence: sea freight costs. Following oil tanker costs’ lead, cargo shipping rates have stabilized. As Exhibit 1 shows, in mid-January, the Baltic Dry Index—a composite measure of freight costs—was still falling after a short spike last year tied to drought concerns in the Panama Canal. But as Yemen’s Houthi Rebels stepped up attacks on Western-flagged cargo ships crossing the Red Sea—and Western navies stepped up proportionately—costs jumped again, sending the Baltic Dry up 14.9% between January 17 and 19.[i] But since then, after moving sideways, the index has reversed some in recent days.

Exhibit 1: The Baltic Dry Index Is Stabilizing

Source: FactSet, as of 2/1/2024. Baltic Dry Index, 12/29/2023 – 1/31/2024.

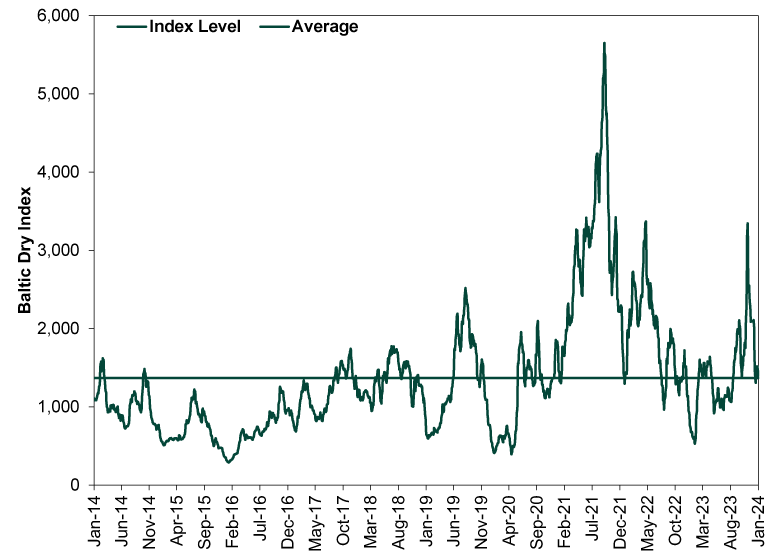

Now, we don’t like reading into short-term moves, so we think Exhibit 2 is more telling. It shows the Baltic Dry over the past decade, and it highlights a few key points. One, even with last month’s jolt, it remained well below levels seen during the heights of the COVID-related supply chain crisis. Two, the current level is almost bang-on the average over this span. The vast majority of this stretch didn’t feature shipping crises, suggesting to us current rates aren’t signaling big trouble.

Exhibit 2: Current Rates Are Pretty Average

Source: FactSet, as of 2/1/2024. Baltic Dry Index, 1/31/2014 – 1/31/2024.

If shippers faced insurmountable obstacles, freight costs would likely show it, reflecting the significantly higher risks and more arduous journeys. Instead, it looks like markets have already adapted to several carriers’ need to sail around Africa’s Cape of Good Hope, which amounts to a week or week and a half’s extra travel time. Sometimes we think people are wired to think of this longer trip as horrendous because of all the time kids spent learning about the old wooden ships getting dashed on the rocks in treacherous waters at the tips of Africa and South America, but technology has come a long way in a few hundred years. Yes, going around the horns adds some time, but it is no longer shipwreck central.

Markets see all of this too, in our view, and also appear to be reflecting businesses’ adaptability. We aren’t arguing the situation is risk-free, but investing is about owning a share in businesses’ future profits. Strong demand can buoy revenues above and beyond shipping costs’ potential pressures. Plus, most of the developed world economy is services’ based, making the Red Sea irrelevant to activity. Lesson: What is important to headlines and the world in general isn’t always what is important to stocks’ bottom line.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today