Personal Wealth Management / Market Analysis

Return of the Euro Crisis’ Ghosts

Should investors be concerned about the recent spate of scary eurozone headlines?

With volatility back, many seek to explain what has amounted to quite a back-and-forth October. And it seems many settled on recent developments in Europe as the culprit. While possible, a quick glance at Europe's recent headlines might have you thinking it's 2011 or 2012. In our view, fears around the eurozone likely lack the teeth to materially bite this bull. The questions may be slightly different now: It's more, "How does the eurozone avoid a 'lost decade' of growth?" than warnings of the imminent collapse of the common currency. But most of the fears-and many of the specifics-are the same. These recycled false fears likely lack the surprise power to knock a global bull off track.

Interested in market analysis for your portfolio? Our latest report looks at key stock market drivers including market, political, and economic factors.

Better Together, Spanish Edition

In Spain, Catalan leader Artur Mas canceled the November 9th independence referendum , two weeks after the Spanish Constitutional Court suspended the planned vote. In its place, Mas is planning a more informal means for Catalans to voice their opinion, without the risk of officials getting indicted. But with volunteers manning this "revised process" and Catalan officials unable to access voter registration records to see who can even legally vote, the original nonbinding referendum has become a glorified opinion poll-similar to the 2009 vote-with no way to tell whether it's predictive or not. Even supporters suggest this version is virtually meaningless. The old fear Catalonia breaks away has become even more bunk now.

Germany and France Team Up to Avoid "Lost Decade"

How do you prevent the eurozone from turning Japanese? Apparently the German and French economic ministers don't know, so they've turned to the academics-asking for Franco-German initiatives that will boost domestic and eurozone growth. As grand as this partnership sounds, the request is for recommended measures to implement by 2017-not exactly an urgent call to action. A humorous timeline, since real eurozone GDP's prior highpoint is in 2008. So if you assume (a big assumption, mind you) the eurozone economy doesn't exceed that between now and the implementation of the economists' recommendations, they will be implementing advice targeting avoiding the decade they just experienced.

With the fiscal policy friction between France and Germany-and expectations France's 2015 budget will fall short of EU requirements-building political goodwill seems to be the motivation here. But even if this Q&A session with economists results in plans the two nations accept, the recommendations are unlikely to get implemented any time soon. Gaming market direction beyond 12-18 months is futile, in our view. From that perspective, this is noise. However, politicians buying into the drab-decade narrative is a good sign sentiment is quite dour.

Germany vs. The OMT, Round 6

The European Court of Justice (a real thing!) will now determine the legality of the ECB's Outright Monetary Transactions (OMT) program-the plan that followed ECB President Mario Draghi's "do whatever it takes to back the euro" statement from July 2012. A decision is expected mid-2015. Several Germans, including lawmaker and noted euroskeptic Peter Gauweiler, claim the OMT breaches the German constitution and equates to the ECB financing government debt-impermissible under eurozone treaties. The ECB argues it is merely conducting monetary policy, which is clearly within its jurisdiction.

While fighting the OMT brandishes Gauweiler's euroskepticness-political street-cred-it's a bit pointless today. The ECB designed the OMT to quell panic-driven high rates on government bonds, which the ECB then saw as a threat to the euro. But since inception, the OMT has bought a grand total of zero bonds. Rates fell when confidence returned, rendering the program moot. Gauweiler and Co.'s litigating amounts to challenging a press release filled with highfalutin statements backing the common currency and fun central banker-jargon! As the ECB's lawyer succinctly said, "Legally speaking a press release cannot be deemed to be valid or invalid." Nothing on PRWeb is exactly a constitutional issue.

Greece Is Still Greece

Greece returned to the front page as well, likely due to recent market volatility. With bailout battles, financing issues and political concerns, Greece's 10-year yield rose above 7% for the first time since March. But given where Greece was just a couple of years ago-two defaults in one year, two bailouts and borrowing costs over 30%-a 7% yield doesn't seem so bad. What's more, Greece has never exactly been hailed a huge success. Talk of another potential default, restructuring and more have surrounded the nation throughout the last couple years-nothing surprising to markets.

Stressful Stress Tests

On October 26, the ECB will release its Comprehensive Assessment-the Asset Quality Review and stress tests-results. These findings aim to establish a high standard and inform the ECB of the banking system's standing before it becomes banks' primary supervisor November 4. While we question stress tests' effectiveness for proving banks' readiness for future crises, they've already impacted the eurozone by hitting lending. Given the possible consequences from failure-like being deemed insolvent-loan growth has been anemic at best in anticipation of these stress tests. Now that doesn't guarantee all eurozone financial institutions will pass the ECB's review, and hiccups could always arise. But getting long-awaited clarity should be positive, removing one obstacle standing in the way of more lending.

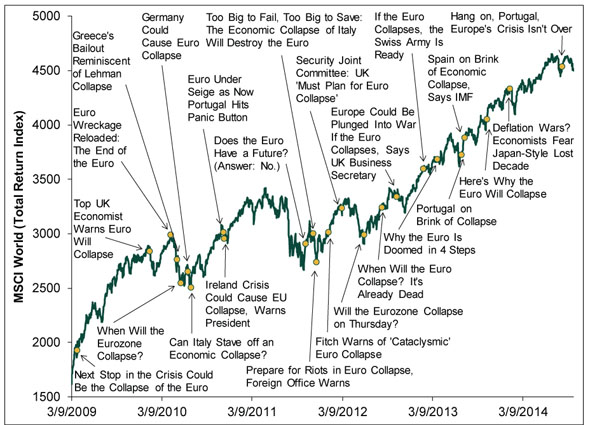

Media also pinpoints slow eurozone growth as a volatility cause-citing data like German trade and factory orders. But these too aren't newfangled issues, particularly in the proper context. German exports did fall -5.8% m/m in August, but that follows July's jump to record highs. Factory orders also dipped after a July surge. Outside these rehashed false fears, new news from the 18-member bloc has actually been ok. Ireland released its first "non-austerity" budget in seven years. Portugal also submitted a growthier budget well within eurozone limits. For some broader perspective, consider what the current global bull market has done throughout the eurozone's real and perceived tumult. (Exhibit 1) Stocks don't need a vibrant eurozone to rise, and with the region better off than the dire interpretations so easy to find, even meh news is probably good enough.

Exhibit 1: MSCI World Total Return Since March 2009

Source: FactSet, MSCI World Total Return from 3/9/2009 - 9/30/2014. Headlines, in chronological order, are here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, here and here.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — August 3 - August 72026-08-11

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today