Personal Wealth Management / Market Analysis

Scaling the Real Impact of the Turkish Lira Meltdown

What is the contagion risk associated with Turkey?

Turkey’s meltdown remained center-stage Tuesday as financial media remained stuck on the possibility of a negative global economic impact. With volatility striking most major indexes globally (to varying degrees), Turkey is clearly hitting investor sentiment. Yet for a country representing just 1% of global GDP to cause a material global economic issue, there must be a “transition mechanism”—a logical reason its problems could disrupt other, larger nations’ economies and financial systems.[i] In Turkey’s case, the probability of actual spillover is quite tiny.

One oft-cited area of potential contagion is European banks. The ECB stated some concerns about eurozone banks’ exposure to Turkish loans last week, sparking a two-day selloff in European Financials. This seems overblown. Total Turkish debt as a percentage of EU bank assets is exceptionally small at 0.43%.[ii] Breaking down exposure at the country level, Spain’s banks have approximately $80 billion of Turkish assets on the books, French banks own $35 billion, Italian banks have $18 billion and—for those concerned about US exposure—US banks have about $18 billion of Turkish assets.[iii] These figures represent approximately 5.3%, 1.2% and 0.8% of Spanish, French and Italian GDP, respectively.[iv] As for individual banks’ credit risks, the market doesn’t appear terribly concerned. Credit default swap (CDS) spreads have increased marginally but are well below concerning levels, with most remaining far below levels seen in 2012, near the depths of the euro crisis.

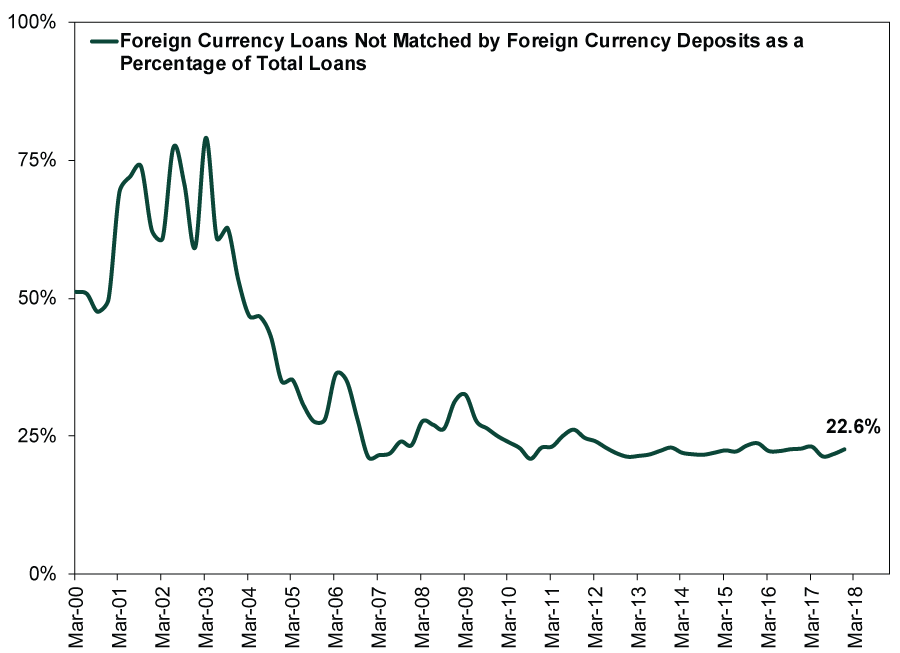

While foreign currency denominated debt is a risk for banks when the local currency weakens, the amount of foreign currency debt isn’t the only determinant of banks’ potential vulnerability, as they can hedge foreign currency risks. Turkish banks happen to be very well hedged. About half of Turkish bank deposits—51%—are in local currency, while 49% are in euros or US dollars.[v] On the other side of the ledger, 66% of Turkish bank loans are in lira, while just 33% are in euros or dollars.[vi] As a result, only 22.6% of Turkish banks’ total loans are foreign exchange loans not matched by foreign exchange deposits, which is equivalent to current estimates of the FX currency reserves. (Exhibit 1) Meanwhile, European banks with exposure to Turkey have been hedging currency risk for years. If Turkish fundamentals were to significantly deteriorate, select European banks may have to raise capital, but this seems unlikely to result in the spillover effect the late-1990s’ Asian Currency Crisis had on Japanese banks (which amounted to 12% of Japanese GDP).[vii]

Exhibit 1: The Majority of Foreign Exchange Loans Are Matched by Foreign Exchange Deposits

Source: Bank for International Settlements, as of 8/10/2018. Foreign exchange loans, foreign exchange deposits and total loans, Q1 2000 – Q4 2017.

Contagion fears also focus on international trade and Turkey’s place in global supply chains. Turkey imported about $236 billion in 2017, with most coming from the EU (about 36% of imports), China (10%) and Russia (8%).[viii] Most of its EU imports were capital and intermediate goods and machinery, primarily from Germany. From China, Turkey mainly bought capital goods and machinery. Most of its Russian imports were raw materials. On the export side, about 45% of Turkish goods go to the EU, while about 20% go to the Middle East, where it exports consumer goods, clothes and food.[ix] Essentially, Turkey serves as a conduit from Europe and China to the Middle East and North Africa (MENA), purchasing capital goods and machinery and using those goods to refine fairly basic commodities into consumer goods and clothes, which they then sell to MENA nations. The lira’s tumble likely reduces demand for imported goods from Germany and China, as well as imported oil. This could cause supply chain disruptions impacting Turkey’s ability to deliver finished consumer goods to the Middle East, potentially adding to inflation in these nations as they search elsewhere for replacements. However, this is a localized issue and unlikely to last, as these products are easily substitutable. Overall, Turkey doesn’t appear to be a major bottleneck globally, though it does sit on the choke point to the Black Sea, with roughly 2.4% of global oil production passing through on its way to Western Europe.[x] This could be affected if unrest were to begin, but for now this is a distant possibility.

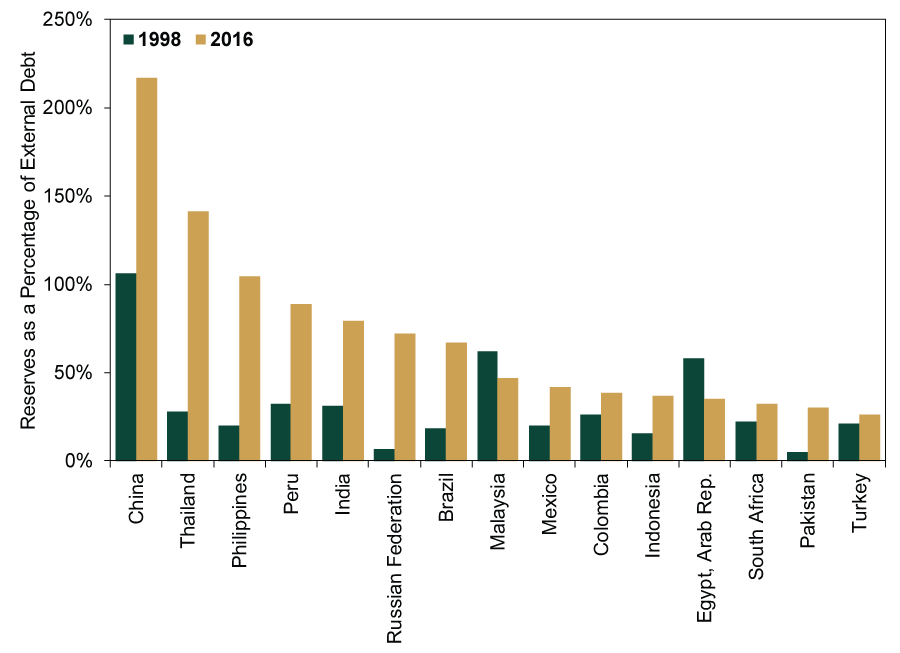

Some outlets note similarities between today and Asia’s late-1990s crisis. The dollar’s recent rise is roughly on par with its mid-to-late 1990s rise, and then, as now, concerns about foreign currency debt are swirling. Yet there are also numerous differences. For one, there are no significant currency pegs. In the 1990s, Thailand and Indonesia had pegs to the dollar, which was vital in transforming a currency crisis into a debt crisis once the governments discarded the pegs. Because banks assumed the pegs would hold, foreign currency debt was largely unhedged. Today, no major Emerging Markets nations have currency pegs, and most debt is hedged. All major developed economies today are in expansion, with well capitalized banking systems—unlike Japan’s weaker foundation in the late-1990s, resulting in that large bank recapitalization. Finally, Emerging Markets had very low foreign exchange reserves in the 1990s, giving them little firepower to support their currencies. Today, aside from Turkey, major Emerging Markets have significantly bolstered their reserves. (Exhibit 2)

Exhibit 2: Foreign Currency Reserves Are in Better Shape Today

Source: World Bank, as of 8/14/2018. Foreign exchange reserves as a percentage of external debt, 1998 and 2016 (latest figure available).

In the near term, volatility could continue as fears linger. But as more investors figure out the potential for fundamental spillover is exceedingly low, Turkey’s power over sentiment should fade, leaving global stocks plenty of room to keep marching higher.

[i] Source: World Bank, as of 8/15/2018.

[ii] Source: Bank for International Settlements, as of 8/15/2018.

[iii] Source: Fisher Investments Research and company filings, as of 8/15/2018.

[iv] Source: IMF, as of 8/15/2018.

[v] Source: Central Bank of Turkey, as of 8/15/2018.

[vi] Source: Bank for International Settlements, as of 8/15/2018.

[vii] Source: Asian Development Bank Institute, as of 8/15/2018. “Lessons From Japan’s Banking Crisis, 1991 – 2005,” Mariko Fujii and Masahiro Kawai, ADBI Working Paper Series, No. 222, June 2010.

[viii] Source: World Bank, as of 8/15/2018.

[ix] Ibid.

[x] Source: US Energy Information Administration, as of 8/15/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today