Personal Wealth Management / Market Analysis

Some Things People Miss About These China Tariffs

All else equal, nothing here appears problematic for global markets in isolation.

As you have no doubt heard, the Trump administration is planning 25% tariffs on nearly $50 billion worth of Chinese imports, a WTO case against China’s technology licensing practices and restrictions on Chinese investment aimed at obtaining key US technologies. In response, China announced tariffs ranging from 15-25% on $3 billion in US goods. Meanwhile, when the Trump administration’s steel and aluminum tariffs went into effect Friday, they exempted Canada, Mexico, the EU, Argentina, Australia, South Korea and Brazil—combined, the source of at least 63% of US steel imports and 48% of US aluminum imports. (Russia is reportedly seeking an exemption too. Stay tuned on that.) All else equal, these tariffs and countermeasures are mildly negative, but we do not expect major market impacts because they are small in scale, accounting for a tiny slice of global GDP. Further, there are some additional nuances that should minimize their bite.

As it stands, we still don’t have full details of President Trump’s China tariffs. The White House gave the Office of the US Trade Representative 15 days to publish the list of proposed tariffs for public comment. (Businesses and lobbyists aren’t waiting for a list—they are already commenting.) Next comes an official 30-day comment period, followed by a review of the comments. Meanwhile, the Treasury Department is developing the list of restrictions on Chinese investment. While this might seem like procedural arcana—boring and perhaps insignificant—it does show the administration following normal procedures, which gives markets time to discount potential negatives.

That said, there doesn’t seem to be much for them to discount. As we discussed yesterday, the tariffs’ goal appears to be inducing China into more closely adhering to US intellectual property rights and letting US firms access China’s market without surrendering trade secrets and other intellectual property. President Trump made noises about the trade deficit, but this seems more like fodder to sell the measure to journalists, as intellectual property policy might be too academic for mass consumption.

Part of the strategy for goading China into reform appears to be targeted tariffs on imports in competitive industries that are easily substitutable from other countries. According to US Trade Representative Robert Lighthizer, the administration believes this will minimize the impact on US consumers—namely because they don’t actually intend for anyone to pay the tariff. White House officials believe the tariff rates should be sufficiently high to block trade with China in these categories, allowing other trading partners to step in and fill the gap. High tariffs targeting Chinese goods in competitive industries, according to their plan, would make most of the targeted Chinese imports uncompetitive, making it irrelevant whether the rate is 25%, 50% or even 100%. This is why scaling these tariffs by multiplying tariff rates and import values could very well overstate the impact. (I’m hedging here—politicians’ plans don’t always work as intended.)

It seems fair to apply this logic to the high steel tariffs as well. Similarly, the aluminum tariff may be lower due to concern about the ease of substitutability—perhaps officials are aware people might actually have to pay it and want to limit the impact.

Given these nuances, it may make more sense to estimate the potential tariff impact by estimating price spreads between current Chinese goods and their substitutes. We can’t do that without the list of products yet, but here is a hypothetical: If the targeted Chinese goods are 5% cheaper than their substitutes, then the impact on US consumers may be only 5% of $50 billion rather than 25%. That might be oversimplified, as the loss of a big competitor could give other firms pricing power, enabling them to bid up these price spreads, but all else equal, this does not appear to be problematic for a $19 trillion US economy. Nor for the global economy: Provided the targeted goods are broadly demanded, China may be able to redirect lost sales to other countries with only minimal discounts. In this scenario, the tariffs could just redirect the flow of goods, with no major hits to anyone.

But setting aside speculation, even if we base calculations on the raw numbers thrown out by the Trump administration, the potential impact is tiny. US imports are 15.3% of GDP.[i] With roughly 63% of steel and 48% of aluminum imports originating from countries exempted from the tariffs, the total value of imports subject to new tariffs is approximately $66 billion ($50 billion from the new China tariffs, $7.3 billion from steel and $8.6 billion from aluminum). Assuming 10% tariffs on aluminum and 25% tariffs on the rest—and assuming no changes in trade (oversimplified, but this is illustrative)—the levies amount to about $15 billion, which is 0.5% of US imports and 0.076% of US GDP.[ii] Meanwhile, US exports are 12.2% of GDP.[iii] China’s announced tariffs would result in levies equaling 0.027% of US exports and 0.0033% of US GDP.[iv]

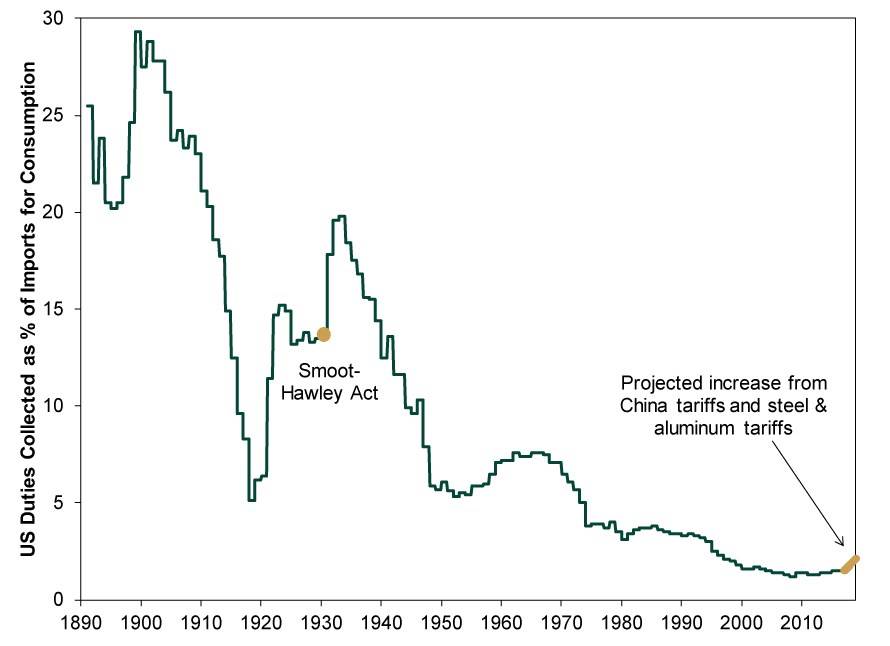

It probably goes without saying that this also pales in comparison to history. Exhibit 1 shows duties relative to US imports for consumption, a narrower measure than total imports. The new tariffs add just 0.64 percentage points to the total bill. By comparison, this figure jumped 6.1 percentage points following Smoot-Hawley, which is 9.5 times larger than today’s increase.

Exhibit 1: Historical and Projected US Duties as a Percentage of Imports for Consumption

Source: US International Trade Commission, as of 3/23/2018.

The impact on China should be similarly small. Chinese imports are about 17% of Chinese GDP, so its tariffs on US imports would equal 0.029% of Chinese imports and 0.0053% of Chinese GDP.[v] Exports are 19.2% of China’s GDP, so assuming most of those $15 billion in potential US tariff payments fall on China, it would amount to 0.62% of China’s exports and 0.12% of Chinese GDP.[vi]If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today