Personal Wealth Management / Market Analysis

Sour Sentiment Outside Equities

Returns are down across the board this year.

Stocks’ jarring week continued Thursday as the S&P 500 dropped -2.1%, closing a whisker below Tuesday’s low and bringing the bear market’s magnitude to -23.2%.[i] While that isn’t large by historical standards, retesting the lows after a summertime rally has understandably weighed on investors. Yet the mood seems to be one of frustrated resignation than outright panic, and we have a hunch why—and in a perhaps counterintuitive way, we think it argues for the recovery lying closer than many seem to expect now.

Last week, we looked at stock and bond mutual fund flows and considered the possibility that the panic selling known as capitulation was occurring more in bonds than stocks. That wasn’t a short-term market forecast, mind you, but an attempt to explore why investors’ behavior wasn’t quite typical for a late-stage stock bear market. This week’s bond market volatility seemingly underscores this hypothesis, judging from the sharp moves, reports of forced selling as pension funds scrambled to raise collateral, and the widespread presumption that much, much worse is in store for fixed income. That all suggests investors are taking their frustration out on bonds more than stocks right now.

Yet it isn’t just bonds that are down alongside stocks this year, and while it may be cold comfort, stocks are in the middle of the pack relative to other categories. Exhibit 1 shows year-to-date returns in US; World; Europe, Asia and Far East (EAFE); Emerging Markets and Japanese stocks (which we include due to Japan’s reputation as a safe haven), as well as two broad US bond indexes and the two flagship cryptocurrencies. Returns are as of Wednesday’s close, since Thursday’s tallies aren’t in across the board as we write, but one day won’t change the overall picture much. And that picture shows that if you are looking for an alternative to stocks, there really isn’t anywhere to go. Even the bond declines don’t quite capture the full picture, as fixed income’s grueling decline began before 2022. Supposedly defensive Japan is underperforming the US and global stocks. Crypto has crashed hardest of all.

Exhibit 1: A Very Frustrating Year

Source: FactSet, as of 9/29/2022. S&P 500 total returns; MSCI World, EAFE, Emerging Markets and Japan Index returns with net dividends; ICE BofA US Corporate & Government (7-10 year) and US Treasury (7-10 year) Index total returns; and bitcoin and ethereum price returns, 12/31/2021 – 9/28/2022.

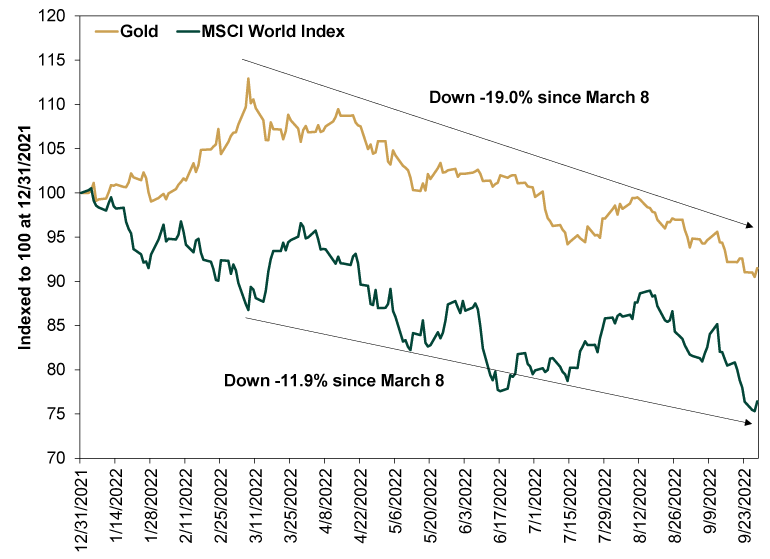

You may have noticed there is one obvious alternative missing from that chart: gold. Its full-year declines are mildest of the lot, which perhaps seems encouraging at first blush. Yet cumulative returns don’t quite tell the full story. As Exhibit 2 shows, gold initially rallied as tensions between Russia and Ukraine reached the boiling point, and its run continued through the war’s first two weeks as commodity markets globally spiked. But since March 8, gold is down -19.0%, dwarfing global stocks’ decline.

Exhibit 2: Gold Isn’t as Shiny as It Might Appear

Source: FactSet, as of 9/29/2022. MSCI World Index returns with net dividends and gold price, 12/31/2021 – 9/28/2022.

Cash is of course another option, but it is hardly more enticing given banks haven’t raised deposit rates alongside the fed-funds rate this year, so savers continue earning a pittance as inflation erodes purchasing power—another knock on sentiment.

We suspect this has all left stock investors feeling unhappily stuck, resigned to sour returns wherever they look. That is the bad news. The good news? Bull markets begin when everyone least expects them to. Sometimes that unfathomability manifests in panic selling, but on other occasions—like 1966 and 1982, based on our analysis of those periods—it perhaps looks more like frozen exhaustion. So from that standpoint, the conditions we see today are actually a rather good backdrop for a new bull market to start. The precise timing is unknowable, and it won’t be clear until we all have significant hindsight, but our point here isn’t about market timing and precise predictions. Rather: If you have stuck with stocks thus far, while the decline to date has been painful, it is only a loss if you sell. If you hold fast and participate in the bull market that follows, whenever that materializes, stocks’ rise erases that temporary decline and carries you up the path to your long-term goals.

[i] Source: FactSet, as of 9/29/2022. S&P 500 total returns on 9/29/2022 and 1/3/2022 – 9/29/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today