Personal Wealth Management / Market Analysis

The Bond Bounce

Bonds are clawing back last year’s declines.

They haven’t garnered as much attention as stocks, but bonds have had a boomlet of their own since October’s lows. Treasurys, corporates and high-yield bonds have all rallied double-digits from their year-to-date lows (October 19 or 20, depending on the security type), a welcome relief. Whether this is indeed a new bond bull market won’t be clear until there is more hindsight. But, in our view, what matters more is that the worst looks to be in the rearview, and even if bonds don’t keep jumping from here, they can play an important role for many investors.

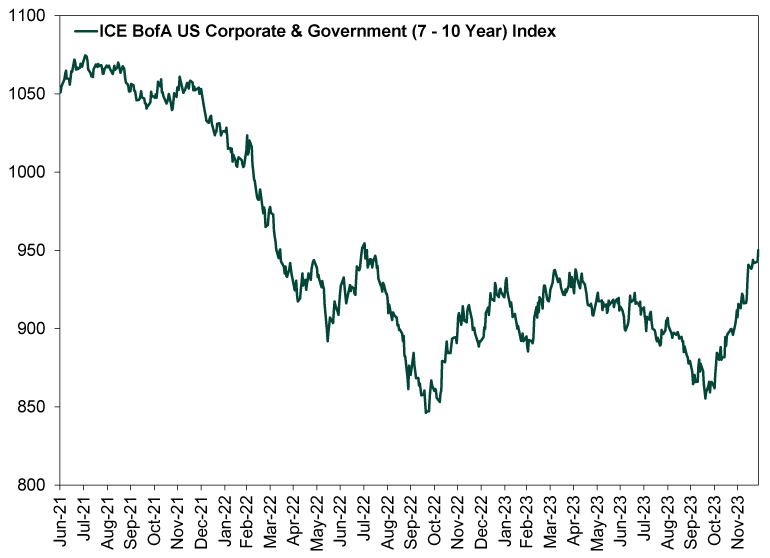

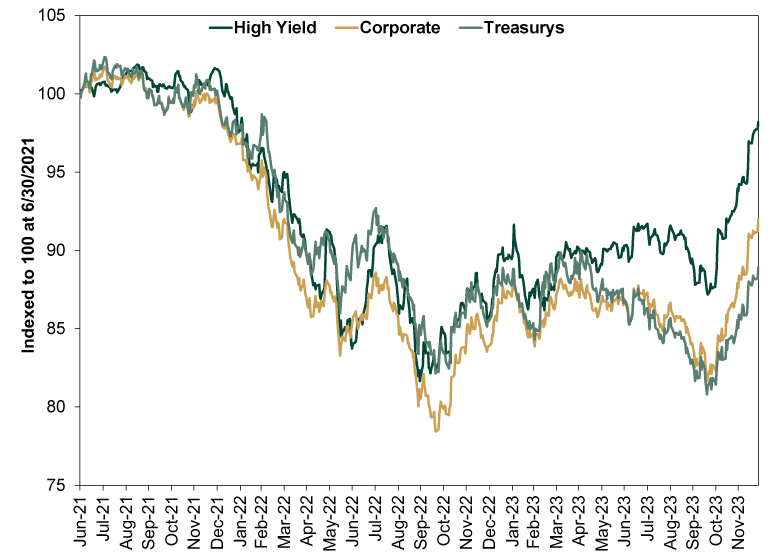

To be clear, bonds have quite a way to go to erase downturn that began way back in August 2021. As we write, the ICE BofA US Government & Corporate (7 – 10 Year) Index remains down -11.6% from its August 2, 2021 high.[i] So the 11.1% rise since October 19 is a good start, but investors are still nursing declines.[ii] That is the dreary news. The good news? As Exhibit 1 shows, 2023 seems on course for modest bond gains on the year—the first up year in three—with the broad bond market back at June 2022 levels. And as Exhibit 2 shows, it is broad, with high-yield bonds leading the charge as sentiment improves and credit spreads narrow—in other words, standard bond behavior during a young stock bull market.

Exhibit 1: Bonds’ Nascent Bounce

Source: FactSet, as of 12/28/2023. ICE BofA US Government & Corporate (7 – 10 Year) Index total return, 6/30/2021 – 12/27/2023.

Exhibit 2: Bonds’ Broad Bounce

Source: FactSet, as of 12/28/2023. ICE BofA US Cash Pay High Yield (7 – 10 Year) Index, ICE BofA US Corporate (7 – 10 Year) Index and ICE BofA US Treasury (7 – 10 Year) Index total return, 6/30/2021 – 12/27/2023.

In our view, this is a very timely reminder that bonds’ role in a portfolio doesn’t depend on a negative correlation with stocks. That is, bonds’ purpose isn’t to zig when stocks zag. Rather, it is to cut the magnitude of the expected zigs and zags more often than not, offering a smoother path in the long run. These smaller zigs and zags come at the cost of lower long-term returns than an all-stock portfolio, but for investors taking higher cash flows, the milder ups and downs are generally worth the opportunity cost since, the majority of the time, they reduce the risk of taking withdrawals in down markets, which could raise the risk of running out of money too soon.

We say all this knowing full well that bonds had a very bad 2022, and we suspect it is cold comfort to hear that bonds at least fell less than stocks (-17.2% during stocks’ bear market, compared to -24.5% for the S&P 500).[iii] Sometimes the smoother path doesn’t feel much smoother because bonds, like stocks, do endure volatility and the occasional bear market. They also occasionally see sentiment overshoot late in those moves, much as we think it did in the autumn, when rates shot up (pushing bond prices down) on alleged “higher for longer” interest rate concerns.

But also like stocks, those bear markets end, and there is a bounce. Those who are patient enough to capture that bounce benefit. In essence the challenge here is the same as with an all-stock portfolio: to stay cool and not react to those temporary declines after the fact, crystalizing them into actual losses and preventing the recovery from taking hold in your own portfolio.

Easier said than done, we know. And while we can’t yet say we are in a new bond bull market, the past two-plus months are a powerful reminder that bonds, too, can have V-shaped bounces that help a blended portfolio continue working toward your long-term goals. They are the answer to the question so many asked, do bonds still have a place? A reminder that bad times don’t last forever and bonds can still deliver some price return alongside their yield.

At the same time, they are also a reminder to keep reasonable expectations and not expect broad bond market returns to parallel stocks’ in direction or magnitude. Since stocks’ October 12, 2022 bear market low, bonds are up 9.9%, paling in comparison to the S&P 500’s 36.4%.[iv] High-yield bonds, as Exhibit 2 showed, can have big bursts. But investment-grade corporates and Treasurys will probably be milder, tracking more with inflation expectations than corporate fundamentals. Inflation expectations are already down quite a lot, and that improvement is probably priced in at this point, making it unlikely that Treasury yields have more big drops in store from here. We have a hunch that bonds will go back to their normal, milder tendencies, and it will add to folks’ frustrations more than ease them if they don’t keep bonds’ purpose front and center.

So, if you own bonds, remember that purpose. Bonds aren’t there to maximize returns, but to increase the likelihood of a smoother path over your investment time horizon, whether you need a smoother path to support cash flows or you just aren’t comfortable with the wilder swings of an all-stock portfolio. These are generalizations, of course, which may or may not apply to your personal asset allocation. But that asset allocation should have reasoning behind it, and it is probably based on stocks’ and bonds’ long-term returns and volatility—inclusive of their respective bear markets along the way—and how those returns and volatility mesh with your personal goals and needs. Bond bear markets, like equity bear markets, shouldn’t change that calculus.

[i] Source: FactSet, as of 12/28/2023. ICE BofA US Government & Corporate (7 – 10 Year) Index total return, 8/2/2021 – 12/27/2023.

[ii] Ibid. ICE BofA US Government & Corporate (7 – 10 Year) Index total return, 10/19/2023 – 12/27/2023.

[iii] Ibid. ICE BofA US Government & Corporate (7 – 10 Year) Index and S&P 500 Index total returns, 1/3/2022 – 10/12/2022.

[iv] Ibid. ICE BofA US Government & Corporate (7 – 10 Year) Index and S&P 500 Index total returns, 10/12/2022 – 12/27/2023.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today