Personal Wealth Management / Market Analysis

The Debt Ceiling and Downgrade Threats, 2023 Edition

Credit ratings agencies are entitled to their opinions, but don’t overrate the effect on government borrowing costs.

After the close Wednesday, credit-ratings agency Fitch issued a press release stating it was putting America’s AAA credit rating on watch for potential downgrade. The rater argues debt-ceiling “brinkmanship” and the failure to strike a deal so far raise the likelihood the Treasury exhausts its extraordinary measures and misses payments on some “obligations.”[i] While Fitch admits actual default—missing payments on the debt—“is a very low probability event,” it claims failure to reach a deal by the time extraordinary measures run dry would be inconsistent with the company’s view of an AAA-rating. Many think these ratings are crucial to keeping interest rates on the federal debt low, so this has garnered loads of attention and spurred some fear. But we have seen many sovereign downgrades in our day. Such a move could cause short-term volatility in stocks and bonds. But it would likely pass fast. Why? The notion a downgrade assures higher government borrowing costs is not correct. Let us show you.

One great irony of a rater threatening to downgrade the US is that the government is one of the few reasons people actually follow credit raters’ work. The US government created a special niche for these “Nationally Recognized Statistical Ratings Organizations” in the 1970s, on the notion that bond ratings would help investors assess creditworthiness of borrowers ranging from corporates to municipalities and, yes, governments. They wrote these ratings into laws and regulations governing banks and pensions thereafter, giving the raters’ opinions some technical heft.

But, to be clear, these ratings aren’t analogous to your personal credit rating from one of the three major bureaus. A lower rating at one of those will likely make your borrowing costlier. But governments borrow by issuing bonds. Investors buy those, and many don’t hinge the decision on what the credit raters think. Why? They can see the yields in the marketplace. They perform their own research. They come to their own conclusions and may find value that raters’ don’t appreciate.

There is also a long history of raters’ decisions coming after market developments or well-known news—not leading them. Their work in the financial crisis is the stuff of legend, from giving subprime mortgage debt high investment-grade ratings the raters themselves later called “puffery”[ii] in court to rating Lehman Brothers and AIG at least “A” (a strong rating) as late as September 2008, mere days before both collapsed.[iii] Fitch, for what it is worth, gave Lehman’s preferred stock an A+ rating in April 2008. That, for the record, is a month after near-identical Bear Stearns failed. But even beyond these widely touted issues, consider: Did Fitch’s decision to put America on watch because debt ceiling theatrics are acrimonious tell you anything you didn’t already know?

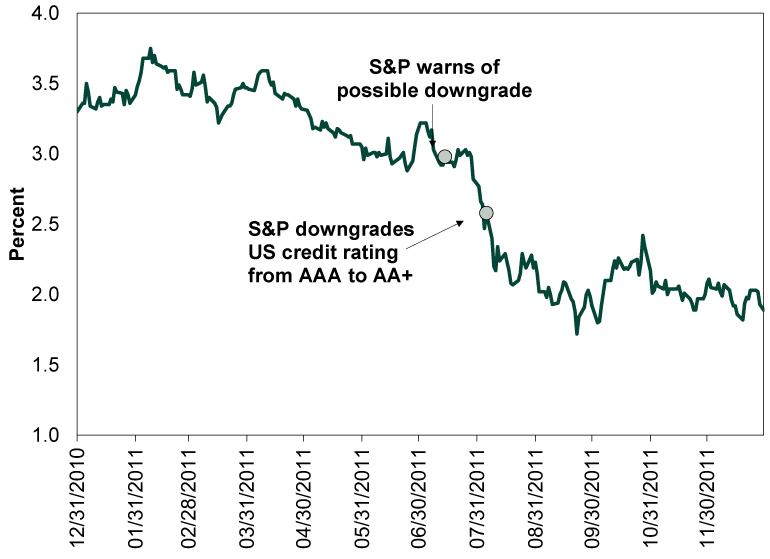

Because their moves rarely shed new light, they often don’t carry the impact people think. Loads of people talk up Standard & Poor’s downgrading America’s debt rating from AAA to AA+ during 2011. But few seemingly remember the chain of events. Back then, Republicans and Democrats struck a deal on July 31, 2011. The House passed it August 1; the Senate on August 2. Former President Barack Obama signed it into law the same day.[iv] (Less than three business days.) Yet Standard & Poor’s didn’t downgrade until August 5. By then, all the debt ceiling uncertainty was gone. They instead cited “brinkmanship” (literally the same word). Their rationale included a $2 trillion math error, which they waved off as inconsequential after the fact.[v]

All that aside, here is a chart of what happened to US 10-year Treasury rates after the downgrade. (Exhibit 1)

Exhibit 1: Downgrades and Down Treasury Rates

Source: FactSet, as of 5/24/2023. US 10-year Constant Maturity Yields, 12/31/2010 – 12/31/2011.

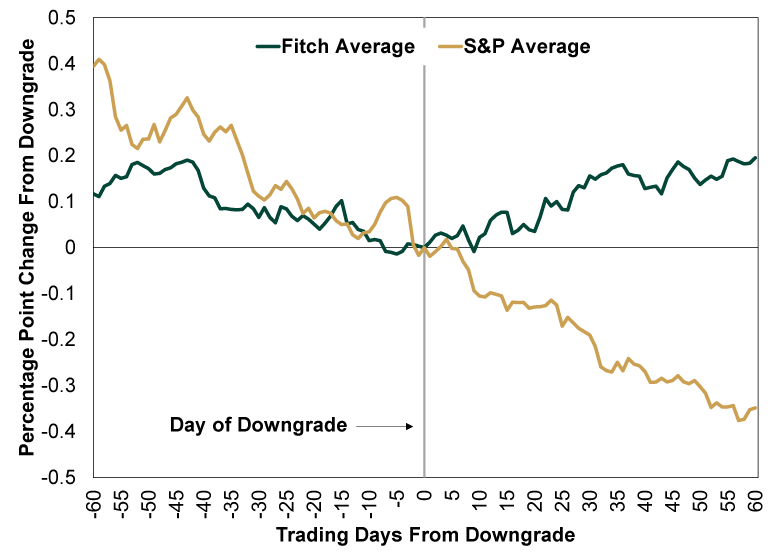

You are seeing that correctly—rates fell after the downgrade. Now, we have seen some on financial Twitter claim this is because the US dollar is the world’s reserve currency. That isn’t the case. Exhibit 2 shows the average yield change 60 days before and after Fitch and S&P downgrades of AAA-rated nations. On average, Fitch downgrades saw rates rise a mere 0.2 percentage point after the move—rates fell after S&P cuts.

Exhibit 2: AAA Downgrades and Interest Rates

Source: Fitch Ratings, S&P Global Ratings, FactSet, Global Financial Data, Inc., as of 5/25/2023. Change in issuing nations’ 10-year bond yields before and after downgrades.

Furthermore, the Fitch data constitute a smaller set. Fitch has downgraded eight AAA-rated sovereigns—the last being Canada in 2020—and it has never re-upped one to its most sterling measure. (Oh, and if you are curious, Canadian 10-year bond yields rose just 0.03 percentage point in the 60 days after that move.) Six fell between 2009 and 2013, centered in Europe. By contrast, S&P has downgraded more AAA-rated issuers, including two each for Ireland, Finland and Spain. Exhibit 2 plots 18 of 19, as we lack daily yield data to cover their 1982 downgrade of New Zealand. But no matter which rater, the maximum yield increase 60 days from these AAA downgrades was 0.68 percentage point—not exactly huge.

We think it is overwhelmingly likely US politicians strike a debt ceiling deal at the last minute. However, we have no view on whether Fitch would follow through on yesterday’s warning and downgrade America’s credit rating. After all, S&P did so despite a deal being struck beforehand. But, regardless, we doubt whatever Fitch thinks of American politics has very much impact on borrowing costs.

[i] “Fitch Places United States' 'AAA' on Rating Watch Negative,” Staff, Fitch Ratings, 5/24/2023.

[ii] “S&P Raises Puffery Defense Against US Ratings Case,” Edvard Pettersson, Bloomberg, 7/8/2013. Puffery is defined as an exaggerated or extravagant statement of praise.

[iii] “Credit Rating Agency Analysts Covering AIG, Lehman Brothers Never Disciplined,” Shahien Nasiripour, Huffington Post, 5/25/2011.

[iv] “Debt Ceiling: Timeline of Deal’s Development,” Staff, CNN, 8/2/2011.

[v] “S&P's $2 Trillion Error Didn’t Change Rating Cut Decision,” Steve Liesman, CNBC, 8/6/2011.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, US Q2 GDP, Eurozone Inflation

2026-07-27

2026-07-27 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 20 - July 242026-07-27

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today