Personal Wealth Management / Economics

The Dollar’s Reserve Currency Status Means a Lot Less Than Many Think

The benefits of having the world’s reserve currency are largely imaginary.

When Western leaders effectively cut off Russia’s access to its foreign exchange reserves as part of the economic response to Vladimir Putin’s invasion of Ukraine, it was only a matter of time until people started speculating that this could trigger the dollar’s demise as the world’s preferred reserve currency. After all, if holding dollars overseas turned out not to be a financial fortress for Putin, it might logically inspire China and other nations to move away from the greenback. We don’t think this outcome is terribly likely, although only time will tell. Regardless, this seems like a good time to issue a friendly reminder: The US gets very, very little from the dollar being the world’s preferred reserve currency, and losing that status won’t be the end of the dollar as we know it.

Conventional wisdom says the dollar’s in-demand status gives the Treasury an “exorbitant privilege” that, among other things, keeps US Treasury yields low. Allegedly, reserve currency status is the only thing standing between Uncle Sam and a debt crisis. If foreign governments were to diversify away from the dollar, the logic goes, demand for Treasurys would plunge and borrowing costs would soar.

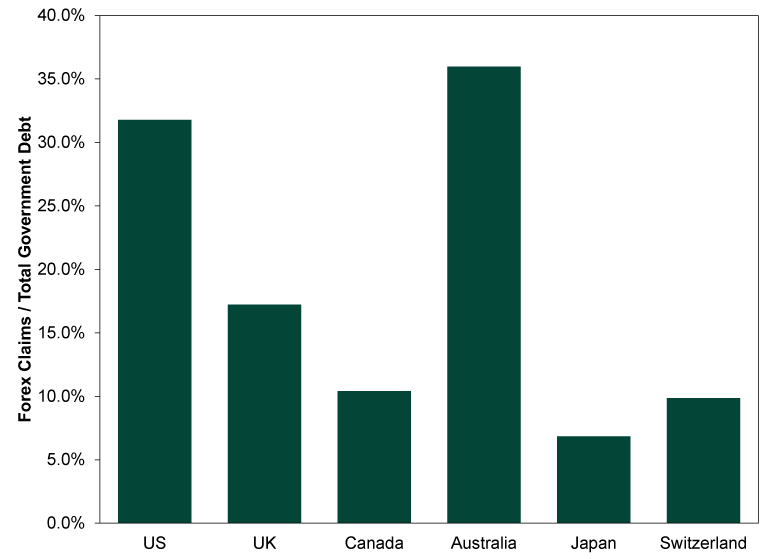

If this were actually true, then one would logically expect US Treasury yields to be much lower than sovereign yields in nations that don’t play a large role in forex reserves. So put it to the test. The IMF publishes quarterly data on global foreign exchange reserve composition, telling us the amounts of dollars, euros, British pounds, Japanese yen, Swiss francs, Canadian and Australian dollars, and Chinese renminbi in governments’ official reserves. (Amusingly, they convert all of these figures to US dollars.) So, we grabbed the last few quarters’ worth of data, then pulled all of these countries’ total outstanding government debt levels in local currency, converted those figures to dollars at today’s exchange rates, and calculated the percentage of outstanding bonds that are held as forex reserves. We couldn’t do this for euroland, unfortunately, since the IMF doesn’t report the issuer of these securities (i.e., there is no way to know which portion of euro-denominated reserves are German bunds versus French OATs or what have you). We also omitted China, as its bond markets have major accessibility issues. But for everything else, see Exhibit 1.

Exhibit 1: Total Foreign Exchange Reserve Claims as a Percent of Outstanding Government Debt

Source: IMF, FactSet, US Treasury and Australian Parliament, as of 3/18/2022. Forex Reserve Claims and Total Debt Outstanding on 12/31/2020 (Switzerland), 6/30/2021 (Australia) and 9/30/2021 (US, UK, Canada and Japan).

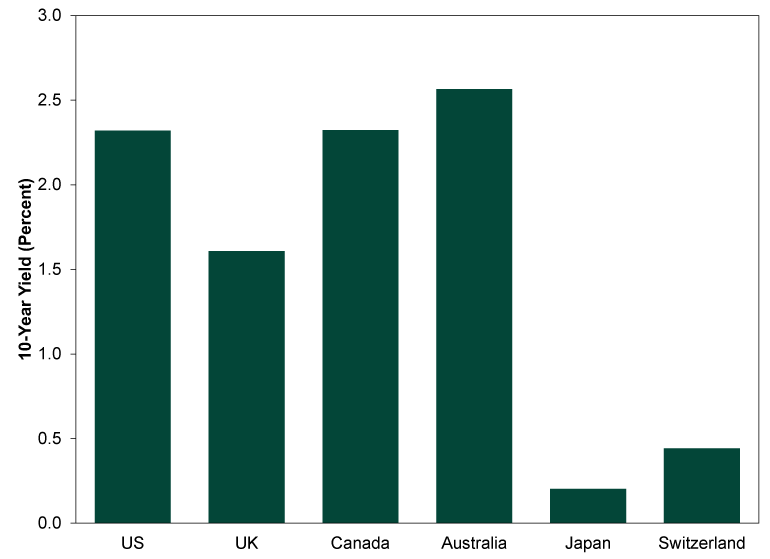

This depiction probably overstates the amount of sovereign bonds held in reserve, as other securities serve as reserve assets besides bonds. But bonds feature prominently, so we hope you agree it is a quick and dirty—but fair—approximation. With that disclaimer out of the way, if we accept the claim that high forex reserve use enables cheap borrowing, then the US should have the cheapest rates of anyone here save Australia. Yet as Exhibit 2 shows, well, that isn’t the case.

Exhibit 2: Current 10-Year Sovereign Yields

Source: FactSet, as of 3/22/2022. Benchmark 10-year government bond yields for the nations depicted on 3/21/2022.

No, dear readers, your eyes do not deceive you. The US and Canada tie for the second-highest borrowing costs, trailing only Australia—which has a higher share of bonds serving as reserves. Meanwhile, the two countries with the lowest reserve use, Japan and Switzerland, have the lowest borrowing costs. There is no there there.

Foreign governments are just one source of bond demand. They compete with retail investors, banks, pension plans and other institutional investors for a finite supply of stable, liquid, creditworthy government securities. Considering demand at bond auctions regularly outstrips supply, we think it is fair to say the market is telling us there is something of a shortage right now. If governments were to diversify away from US Treasurys, then, it would free up supply for the many, many other entities that are eager to get their mitts on it. If rapid selling by other governments caused Treasury prices to drop and rates to rise, we suspect other investors would see it as an opportunity to buy high-quality bonds at a discount, and heightened demand would eventually bid prices back up and yields back down.[i]

Bonds move on total supply and demand, and a host of variables influence both. This is why yields fell, on a cumulative basis, when the Fed reduced its stockpile of US Treasurys in 2017 – 2019. It is why tapering and ending quantitative easing in the years before that didn’t make yields spike either. Buyers are fungible—one leaves the marketplace, another enters. Global factors also tend to matter much more than local, as developed-world bond markets tend to be highly correlated. Whether or not foreign governments own them, US Treasurys are the deepest, most liquid, stable and creditworthy sovereign bonds on the market. If people are happy to own Japanese, British, Canadian and Swiss bonds even though other governments aren’t terribly interested, then we daresay they will be delighted to own more US Treasurys if China et al give them the opportunity.

Now, maybe—just maybe—America’s sanctions get whatever bite they have partly due to the dollar’s reserve currency status. But the notion that status stands between the US and a debt-driven demise is a decades-old fallacy. You can safely tune it out, in our view.

[i] With that said, the notion of any government dumping Treasurys en masse is extremely far-fetched. Doing so would force them to take a haircut, which cuts hard against the purposes of holding forex reserves. Any liquidation would probably be gradual.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today