Personal Wealth Management / Market Analysis

The ECB’s Hiking Path Isn’t That Rocky

How ECB rate hikes could very well carry unappreciated benefits for markets.

Normally, central bank actions to move short-term interest rates to 0% wouldn’t constitute “tightening.” Yet that is what many seem to believe since last Thursday, when the ECB announced its intention to hike policy rates by 25 basis points (0.25 percentage point) at its July meeting and beyond. With its deposit facility rate currently at -0.5%, markets are expecting that to hit 0% by September. Many blamed the ECB’s announcement for European stocks’ sharp selloff late in the week. In this case, while 0% is higher than -0.5%, that doesn’t mean monetary policy is becoming more restrictive. Rather, we see it as a move back to normal after years of negative rates, which could very well bring some benefits.

The ECB has three benchmark rates it uses to conduct monetary policy: its main refinancing operations (MRO), marginal lending facility and deposit facility. The MRO rate is what banks pay to borrow from the ECB for a week. This borrowing is collateralized, meaning banks must provide the ECB with eligible assets to guarantee the loan. The MRO rate is currently set at 0%. The marginal lending facility rate is banks’ overnight borrowing cost, which is also collateralized, but typically costs more, now 0.25%.

The deposit facility rate determines what banks receive for keeping funds at the ECB overnight. Notably, this rate has been negative since June 2014—which means banks have had to pay the ECB to store their money. Imagine paying your bank a 0.5% annual rate to hold your deposits—a bit unusual and perverse. The ECB has set this rate progressively further below zero—starting at -0.1% eight years ago and bottoming at -0.5% from September 2019 onward—in an attempt to spur lending. This may sound promising: Penalize banks for storing cash at the central bank as a prod for them to lend instead. But the experiment hasn’t worked out that way. It has backfired, weighing on lending—not prompting it—which is why we think the ECB’s aim to remove negative rates is a blessing in disguise, putting an end to a long-misguided “extraordinary” policy.

Why haven’t negative rates stimulated? They act more as a (small) tax on banks’ balance sheets than a lending incentive. As we explained earlier when the Bank of England (BoE) was contemplating the practice, banks have tried to pass the costs on to depositors rather than lend. It isn’t huge—mostly a minor hindrance to large, institutional depositors—but it shows negative rates are far from having their intended effect.

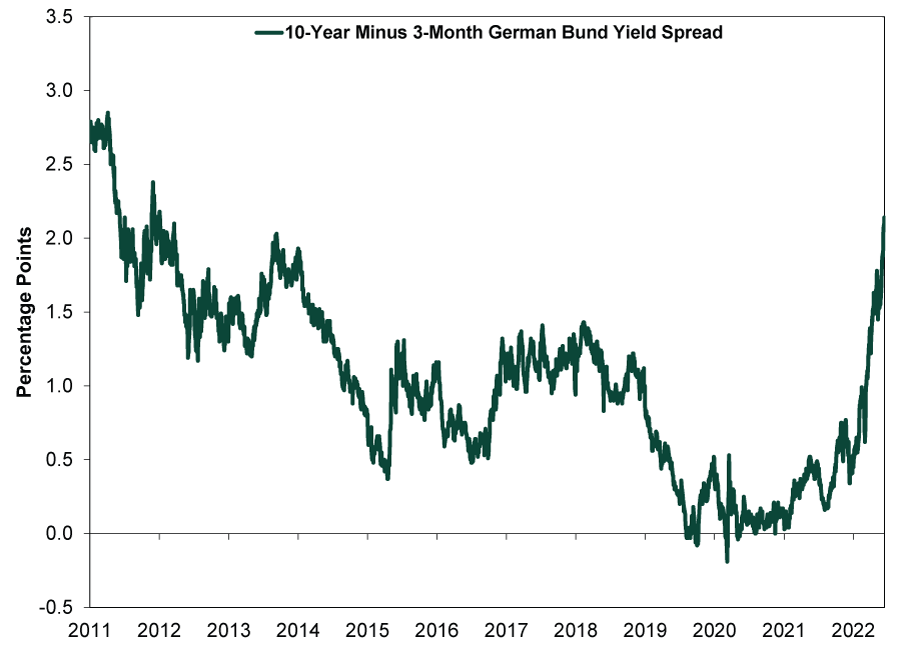

Central bankers thinking slightly penalizing banks for parking reserves will push them to greater loan growth fundamentally misunderstand their core business model—borrowing at short-term rates to lend at longer-term rates and earn the difference. In our view, this is a curious oversight. We have long thought it odd and glaring that central banks, which supervise and regulate the banking system, don’t always appear to acknowledge how it works. The most tried and true way to induce loan growth—and stimulate the economy—is a steeper yield curve, as a century of monetary theory and evidence has borne out. A wider spread between short and long-term rates fattens banks’ potential loan profit margins, increasing their incentive to lend. These have steepened lately in the eurozone, with Germany’s yield curve representative. (Exhibit 1)

Exhibit 1: Germany’s Yield Curve Has Steepened Recently

Source: FactSet, as of 6/15/2022. 10-year minus 3-month German bund yields, 12/31/2010 – 6/14/2022.

Negative short-term rates, though, over time and when expected into the future, lower long-term rates—flattening the yield curve. At one point, Germany’s yield curve was negative out to 30 years.[i] Now, higher long rates are also fanning debt fears in southern European nations like Italy—an issue we have explored before and a topic for another day—but we mostly think this is a sign of sentiment. When markets are falling fast, it isn’t unusual for people to couch good news as bad. This is part and parcel of a phenomenon we call the pessimism of disbelief, and we have found it to be a hallmark of late-stage declines.

But back to lending. Granted, banks don’t charge government rates. Outside some gimmicky headlines, mortgage rates never went negative. But eurozone investment grade corporate yields, which are a decent proxy for bank’s business loan rates, bottomed out at 0.4%, which isn’t a great absolute return.[ii] It likely incentivizes lending to only the most creditworthy borrowers. This isn’t exactly unknown. The San Francisco Fed, for instance, published a study showing negative rates’ negative effect.[iii] Rather than increase lending, it showed banks park their cash in higher-yielding assets, which is less beneficial to the economy. This is why some central banks, like Sweden’s Riksbank, have exited their negative rate regimes, to their credit, while many others—such as the Fed and BoE—abstained from going below zero.

The ECB’s return to 0% and positive rates would be a return to normal. Its gradual balance sheet runoff announcement—letting assets acquired under quantitative easing (QE) mature without replacement—would be, too. For markets, we think that would be a relief and, judging by recent rhetoric (again, see fears over Italian debt), an unappreciated and perhaps even subconscious one. Headlines universally pronounced the ECB’s announcement as “tightening” monetary policy. Coupled with Europe’s energy woes, economic slowdown and associated headwinds from Ukraine, many think the ECB is charting a highly uncertain course, risking recession and/or stagflation, not to mention a fresh debt crisis. To that end, we have seen lots of comparisons with its decision to raise rates in 2011, as the eurozone debt crisis was escalating.

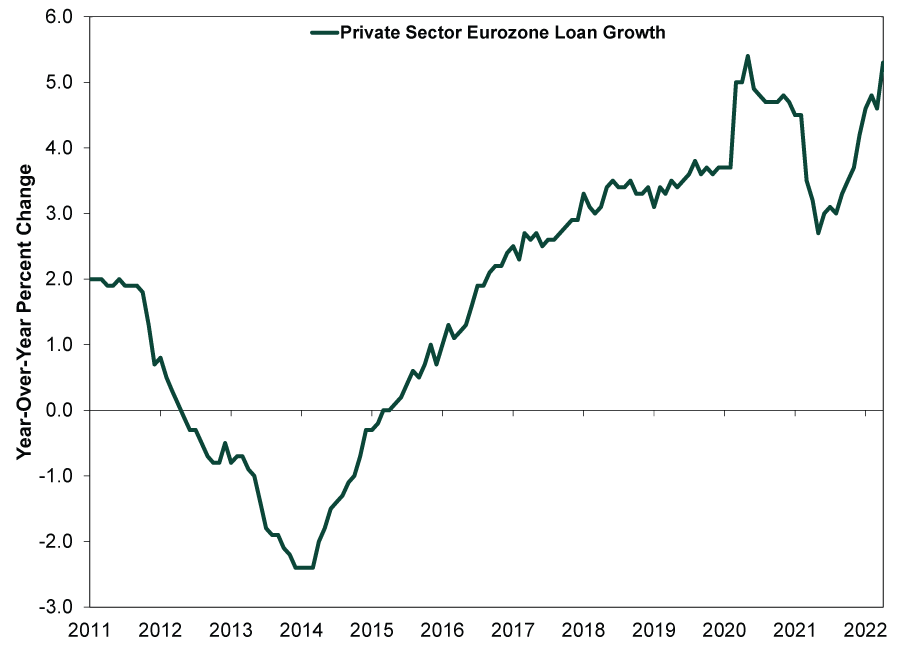

What few seem to notice, though: The eurozone’s yield curves have steepened this year—a counterpoint to chatter about a deep regional recession being a foregone conclusion. As Exhibit 1 showed in Europe’s biggest economy, the spread between Germany’s 10-year and 3-month bund yields has widened to 2.1 percentage points from half a percentage point at the year’s start.[iv] Steepening yield curves across the developed world suggest stronger growth is likelier against the background chorus of doom. In the eurozone, lending has apparently responded—accelerating, even as emergency loan programs wound down. (Exhibit 2)

Exhibit 2: Eurozone Loan Growth Is Accelerating

Source: ECB, as of 5/27/2022. Private sector loans adjusted for loan sales, securitization and notional cash pooling, January 2011 – April 2022.

Meanwhile, whatever policymakers may think, hiking rates is unlikely to affect inflation. When price jumps stem from supply-driven disruptions, there isn’t much central banks—which have no control over supply—can do. Despite their reputation for omnipotence, they have no power to reverse material shortages, expand shipping capacity or stop wars. All they have are a few monetary levers, and they haven’t demonstrated much skill at pulling them over the years. Besides, central bankers don’t drive the economy. It is a complex beast, and central bankers’ influence on it is marginal at best.

It is possible the ECB and other central banks, taking aggressive action, invert global yield curves mistakenly—that is worth watching out for. But none are close, and whether intentional or not, their balance sheet runoffs help preserve positive yield curve spreads as they remove some of the downward pressure on yields.

[i] Source: FactSet, as of 6/15/2022. 30-year German bund yield, 8/5/2019.

[ii] Ibid. 7 – 10-year ICE BofA Euro Corporate Index yield to maturity, 12/11/2020.

[iii] “Commercial Banks Under Persistent Negative Rates,” Remy Beauregard and Mark M. Spiegel, Federal Reserve Bank of San Francisco Economic Letter, 9/28/2020.

[iv] Source: FactSet, as of 6/15/2022. 10-year minus 3-month German bund yields, 12/31/2021 – 6/14/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today