Personal Wealth Management / Market Analysis

The Unbearable Lightness of ECBeing

It'll be nice when the ECB finally retires QE; eurozone stocks should still do great in the meantime.

We'll miss posting tapir pictures when global QE ends eventually, but that is all. (Photo by Alphotographic/iStock.)

European Central Bank (ECB) President Mario Draghi is feeling positively chippy about the eurozone economy. GDP has grown 15 straight quarters and inflation is nearing the ECB's just-under-2% target. Mandate accomplished! Many folks now anticipate an end to the ECB's "non-standard monetary policy measures"-quantitative easing (QE) to most-and, perhaps after that, hiking rates back above zero. This has some speculating about the impact of tapering QE and worrying it will hurt continental stocks. But extant evidence suggests to us these fears are overwrought. Tapering QE is much more likely to help eurozone stocks than hurt.

QE is commonly misperceived as stimulus-including by the ECB-but in practice it hinders economic growth. When the ECB buys long-term bonds in large quantities-so much so they've struggled to find enough-it raises their prices. Since bond yields move inversely to prices, rising prices mean falling yields. Central bankers think lower long-term rates stimulate growth by making borrowing cheaper for individuals and businesses, goosing loan growth. Problem is, this ignores the supply side. By reducing long-term interest rates while short rates are fixed, QE also narrows the spread between the two-flattening the yield curve. Because banks' lending profit margins depend on this spread-they borrow short, lend long and pocket the difference-flattening the yield curve lowers their incentive to lend, stifling businesses' credit access and dragging on economic activity.

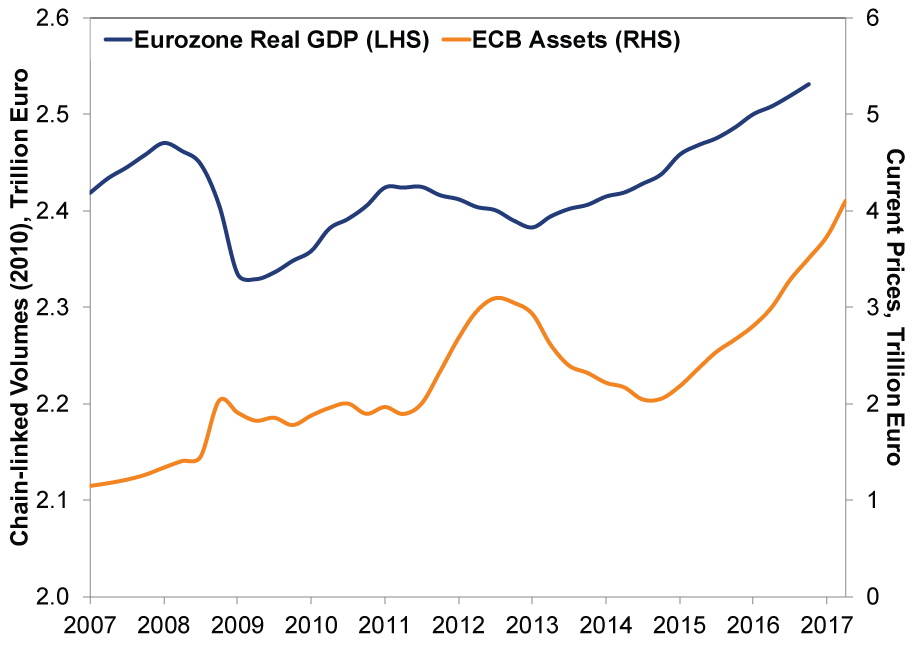

QE didn't create the eurozone's expansion. It began in early 2015,[i] but eurozone GDP had already been growing for two years by that time. (Exhibit 1) The economy surpassed its Q1 2008 peak-officially progressing from recovery to expansion-one quarter later. Before the ECB's "expanded asset purchase program" (EAPP) was announced in January 2015, the eurozone's 2011 - 2012 sovereign debt crisis was over. ECB emergency lending undertook during that time was no longer needed. As credit markets normalized, the ECB's balance sheet shrunk.

Exhibit 1: Massive ECB Balance Sheet Expansion Hasn't Done Much

Source: Federal Reserve Bank of St. Louis, as of 4/28/2017. Seasonally-adjusted quarterly eurozone GDP at constant (2010) prices, Q1 2007 - Q1 2017. European Central Bank assets, January 2007 - April 2017.

We can't know how much faster eurozone growth would have been sans QE, but after the ECB announced a QE reduction last December,[ii] eurozone yield curves steepened, lending picked up, and Purchasing Managers' Indexes suggest growth accelerated. Coincidentally, eurozone stocks are leading the developed world year to date. Similar growth boosts occurred in the UK and US after the Bank of England ended QE in November 2012 and the Federal Reserve announced its QE taper in December 2013. The evidence overwhelmingly suggests QE has been counterproductive and ending it is positive for the economy and markets.

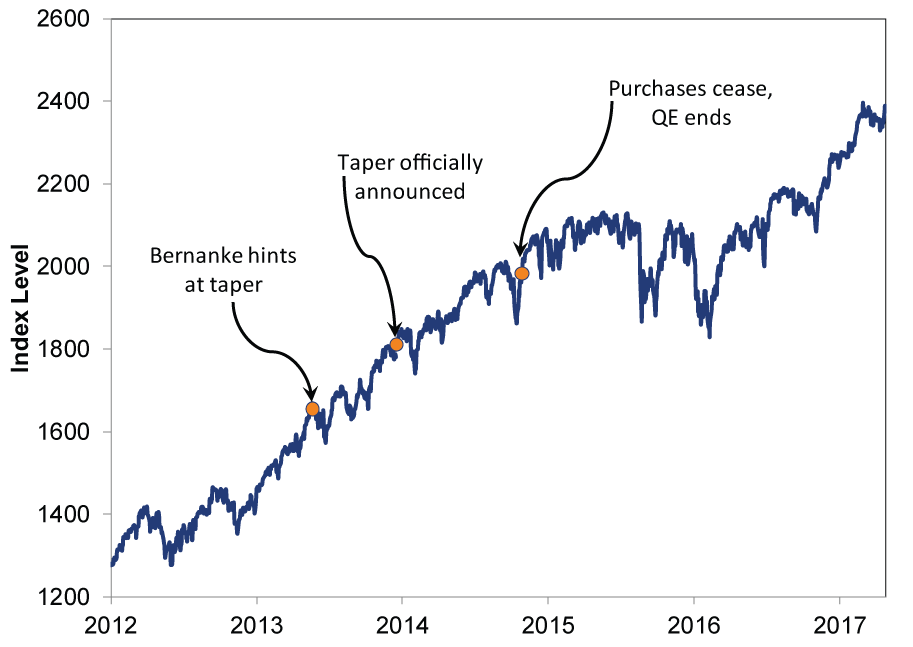

Ongoing eurozone economic improvement belies the need for "monetary accommodation"[iii] and argues for further reductions in ECB asset purchases-tapering-to a full stop.[iv] If Draghi's latest jawboning means that's in the cards, great, but it's impossible to predict based on his or any central banker's coaxing. That said, if it takes a while to officially taper, fine! Markets discount widely discussed expectations. US taper talk sent long rates higher months before Bernanke finally tapered for reals, and stocks rallied throughout. (Exhibit 2) We've seen that to an extent in Europe as well. Taper talk has its own brand of bullishness.

Exhibit 2: Stocks Love Tapers!

Source: Federal Reserve Bank of St. Louis, as of 4/28/2017. S&P 500 price level, 1/3/2012 - 4/27/2017.

As for interest rate liftoff, the sooner the better, too. Negative interest rates are essentially a tax on banks, cutting their profitability. Removing them would take away another impediment to lending and likely boost economic growth further, not to mention eurozone Financials' earnings. A brighter economic outlook-and a more upbeat Draghi-hopefully brings forward the day when counterproductive ECB monetary policy ends. That's bullish for the eurozone. Regardless, a growing-and underappreciated-economy leaves stocks plenty of fuel to rally.

[i] Not to be confused with policies used during the eurozone's debt crisis, which occasionally resembled QE but weren't officially marketed as such.

[ii] Which the ECB insists is not a taper-so don't call it a taper-a non-taper taper.

[iii] From the ECB's perspective. Again, in our view, QE is holding the economy back and was never justified in the first place.

[iv] Then they can start talking about shrinking it again-QExit-the central bank equivalent of going on a diet.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today