Personal Wealth Management / Market Analysis

Two Takeaways From October’s Jobs Report

Employment data’s predictive powers are imaginary.

Good news! The US economy added 531,000 nonfarm jobs in October, inching the unemployment rate down from 4.8% to 4.6% as people found work across the services sector.[i] Strong wage growth also helped pull new workers into the labor force, which increased by 104,000. Those are the highlights—and pretty strong numbers! As always, though, none of this means anything for stocks, as labor market data are late-lagging indicators. But we did glean two fun nuggets for you—let us dive in.

1. Job gains and losses aren’t good real-time economic snapshots.

People often look to the Employment Situation Report—the technical title of each month’s payroll and unemployment report—as a real-time barometer, and we can sort of see why. It comes out the first Friday after month-end, making it one of the fastest releases. But as this report shows, haste makes waste: These data are subject to revision, often to a very large degree.

That was plainly evident in the revised jobs numbers for August and September, which the October report presented. Initially, the US Bureau of Labor Statistics (BLS) reported nonfarm payrolls rose by 235,000 in August and 194,000 in September.[ii] Headlines greeted these reports with disappointment, bemoaning the Delta variant’s apparent economic impact. But now we know this despair was largely misplaced: Revised data show payrolls rising 483,000 in August and 312,000 in September, a combined 366,000 above initial estimates.[iii] That has led to a general oops, guess it wasn’t so bad after all, *shrug* in most of today’s coverage. The vast majority of other indicators already proved that, but we digress.

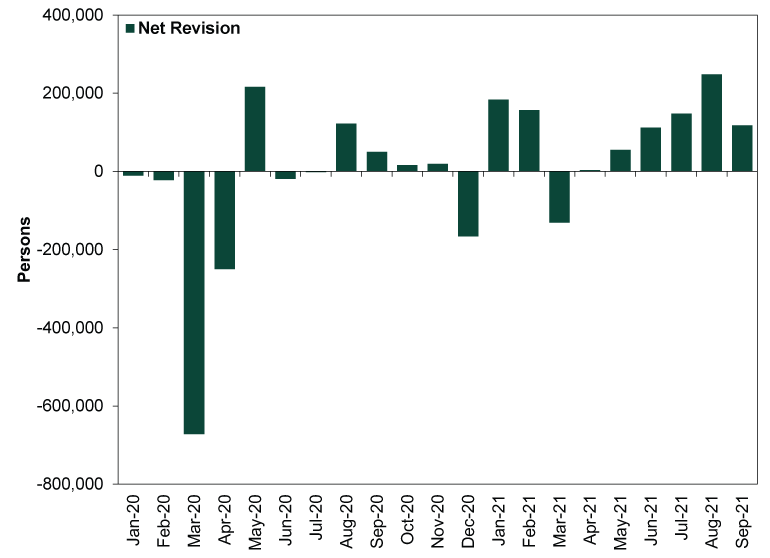

Now, we don’t think labor market data are a great economic indicator to begin with—growth begets hiring, not the other way around. (More on this shortly.) Maybe you disagree, which is fine, but consider: Is any indicator that is subject to such massive revisions all that telling? After all, big revisions like August and September’s aren’t the exception in the COVID era—they are the norm. (Exhibit 1)

Exhibit 1: Revisions to Nonfarm Payrolls, January 2020 – September 2021

Source: BLS, as of 11/5/2021. January 2020 – August 2021 figures are the difference between the third and initial estimates of the monthly change in seasonally adjusted nonfarm payrolls. September 2021 figure is the difference between the second preliminary and initial estimate.

Revisions were smaller pre-COVID, but that is to be expected considering monthly job changes are generally much smaller during normal times. But even then, the revisions have been big relative to the totals. In 2019, the mean absolute revision between the initial and third estimate was 34,000 (meaning, that was the average magnitude of revision up or down). The average initially reported monthly payroll gain was about 171,000. So that means the average revision was 20% in either direction. That ain’t small. Moreover, 2019’s revisions were small by historical standards. From 2003 to the present, the absolute mean revision between the third and first estimate was 48,000 jobs.[iv] Seems to us like people should generally take the initial report with a heaping spoonful of salt.

2. Economic growth does not depend on a growing labor force.

While the labor force did rise as 251,000 women entered the labor force, that was offset partly by the departure of 158,000 men, leading to a lot of speculation about structural factors affecting people’s ability and desire to work.[v] With the labor force participation rate holding steady at 61.1%—far below pre-pandemic norms, which were already a lot weaker than late-20th century trends—there was an abundance of handwringing about a shortage of workers putting a ceiling on economic output.

We see a big flaw in this argument: Hiring doesn’t create economic growth. It is the other way around, which this employment report shows handily. Strong job gains followed strong economic growth as businesses reopened and rebounded from lockdowns. Employers did not immediately add headcount when they reopened, as we showed yesterday—it took time. Smart business owners waited to make sure they could actually stay open. In some cases, it may also have taken a while for returning to work to make financial sense for some workers, given the temporary extra unemployment benefits. But whatever the cause, output increased faster than headcount did.

Tough times always incentivize businesses to do more with less. Eventually that ability runs out and companies don’t have the capability to meet demand. Hiring more workers is an obvious solution, but it isn’t the only one. If a business can’t find qualified workers at a reasonable cost, it can invest in productivity-enhancing technology instead. It can engage freelancers and contractors. It can automate certain tasks.[vi] Where there is a will and demand, there is a way to boost output even if you can’t raise headcount.

[i] Source: BLS, as of 11/5/2021.

[ii] Source: BLS, as of 11/5/2021. Initial estimate of change in seasonally adjusted nonfarm payrolls, August and September 2021.

[iii] Ibid. Third estimate of the change in seasonally adjusted nonfarm payrolls, August 2021, and second preliminary estimate of the change in seasonally adjusted nonfarm payrolls, September 2021.

[iv] Source: BLS, as of 11/5/2021. Nonfarm Payroll Employment, revisions between over-the-month estimates, 2003 – present.

[v] We are referring here to the age 20 and up brackets, not the total male and female labor forces.

[vi] Not applicable to your friendly MarketMinder writers. We are as human as they come! [Types MarketMinderbot, then emits a computerized chuckle.]

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today