Personal Wealth Management / Politics

What Investors Should Make of Windfall Taxes and Export Bans

Rounding up the latest energy policy proposals.

Editors’ Note: MarketMinder favors no politician nor any political party, assessing politics and policy ideas solely for their potential market and economic impact.

Crude oil and gasoline prices may be down from this year’s highs, but households worldwide continue dealing with high home energy costs, spurring governments to consider taking action. On our shores, the Biden administration is jawboning about an Energy sector windfall profits tax and banning oil and gas exports. Britain is mulling an extension of its own temporary windfall tax, and Australia is considering an export ban and capping natural gas prices. Now, this is obviously a politically sensitive topic, so please understand that we aren’t trying to take sides or wade into the political aspect—especially on the eve of America’s midterm elections. But considering policies’ impact is an important task from an investing standpoint. In this case, while we don’t think any of these initiatives would likely be a net benefit, we doubt their imposition would be a huge new negative for stocks.

Take windfall profits taxes. The argument for them seems simple: Oil and gas companies have enjoyed bumper profits due to prices that rose for reasons outside their control this year—a happy accident, according to our politicians—while consumers have suffered. Therefore, it is only fair to tax this temporary windfall and use the proceeds to help households and businesses having trouble making ends meet. Problem is, a windfall tax discourages new investment, which is what is ultimately needed to bring prices down. Why would companies invest in future production now when governments are signaling they could raid any profits that brings? It also ignores recent history as well as the Energy sector’s cyclicality. In general, oil prices rise as demand exceeds supply. Eventually high prices incentivize new investment, which boosts production and brings supply in balance with demand. Inevitably, oil companies overshoot, creating a supply glut that pulls prices down. When that happens, they cut costs to stay afloat, which eventually reduces supply as new wells don’t come online to replace spent ones. That leads to supply shortages, pushing prices higher and starting the whole cycle anew.

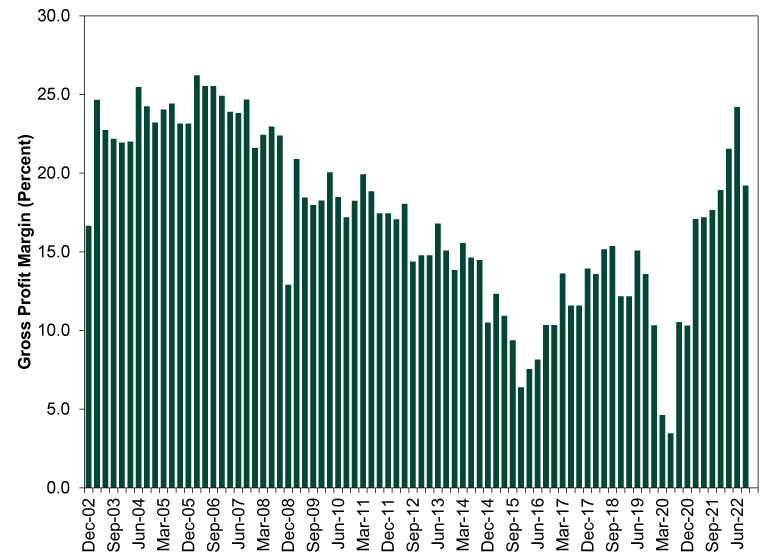

Oil and gas companies’ earnings are price-sensitive—not volume-sensitive. They rely on the flush profits that arrive when prices are high to get them through the lean times, especially if they took on debt to fund expansion during the preceding boom. That is what happened to US shale oil producers in the 2010s. Early in the decade, as the shale boom boomed, companies enjoyed fat profit margins and the sterling credit that came with them. They borrowed heavily to drill new wells and battle for market share. But it all came crashing down in the middle of the decade, when a global supply glut took oil prices to generational lows. That tanked profit margins, putting several smaller producers in financial trouble. Rising prices in the decade’s second half gave some temporary relief, but then the COVID pandemic whacked the industry hard. Oil prices fell as governments’ lockdowns curtailed economic activity, and margins hit multi-decade lows. Bankruptcy fears stalked the industry, and even as economies reopened, production didn’t rebound immediately as many companies lacked staffing, had shuttered wells and needed to put all their spare resources into paying down debt. This year’s higher prices, a temporary byproduct of Russia’s Ukraine invasion and the West’s sanctions, are what it took to enable companies to do both—and reap some reward for surviving a very tough 2020. We would also note, as Exhibit 1 shows, that the abnormal windfall lasted all of one quarter, and profit margins are now at pre-invasion levels.

Exhibit 1: 20 Years of Energy Sector Profit Margins

Source: FactSet, as of 11/3/2022. MSCI World Index Energy sector gross profit margins, quarterly, Q4 2002 – Q3 2022.

Export bans, whether it is the US banning shipments of crude or Australia blocking natural gas, likely wouldn’t work any better in the real world. Politicians suggest them on the belief that exporting oil saps domestic supply, making local prices higher than they otherwise would be. Problem is, oil markets—and prices—are global, determined by the entirety of global supply and demand. If the US were to stop exporting crude oil to Europe or Asia, refineries there would bid up crude from other sources, and that would feed back into global oil benchmarks. Meanwhile, the US would be stuck with a glut of oil it can’t refine, as many Gulf Coast refineries are geared toward heavy crude, not the light sweet crude that comes from America’s shale patch. This is why the US lifted the export ban in the first place in 2014—to get American oil to refineries that could use it. Lifting that ban didn’t make gas prices rise, and reinstating it probably won’t make them fall.

Lastly, as for price caps, they too would discourage production, extending the current shortages. But they would also remove households’ and businesses’ incentives to conserve energy, which could raise demand and make much more severe shortages—and rationing—a distinct possibility. This is also the risk the EU is exposing itself to via its own proposals to cap natural gas prices. We aren’t saying it is a massive risk or that rationing is guaranteed if governments go this route, but the potential for unintended consequences bears watching.

That goes for all of these proposals. While we don’t think they would offer much help, they also don’t necessarily pose automatic negatives. A lot of it would depend on how any measures are structured, as the UK’s windfall profits tax attests. Because it includes exemptions for investment, one of the biggest companies it targets has reported it will pay zero windfall taxes this year. Another will pay £800 million, and overall, His Majesty’s Treasury looks highly unlikely to reap the £5 billion in windfall tax revenue that the number crunchers estimated would arrive in the tax’s first year.[i] If an American windfall tax had similar exemptions, it would probably weaken the potential drag on production. And if UK Energy stocks’ year-to-date returns are any indication, it wouldn’t be auto-bearish—in pounds, they are up over 50% this year.[ii]

More broadly, stocks have dealt with this sort of chatter—and the risk of government intervention—for months. It isn’t new. Mostly, we see it as an area for uncertainty to fall. Right now there are a lot of questions, including what legislation will emerge, whether it can actually pass or if the US or Australia even try. Eventually proposals will become bills—or not. Any bills that get written will then face political gridlock, where they could get watered down or blocked outright. Any legislation that does pass will be old news to stocks by the time it is in the books, and investors will know what they are dealing with, enabling everyone to move on.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today