Personal Wealth Management / Economics

What Markets Are Eyeing Beyond Q3 GDP

To no one’s great surprise—and probably to stocks’ least of all—supply chain hiccups slowed Q3 growth.

US GDP slowed sharply last quarter, from Q2’s 6.7% annualized growth to 2.0% in Q3.[i] Major news outlets blamed logistics problems and the Delta variant, which has been a scapegoat for virtually every disappointing economic reading in recent months. We think the universal reaction is half right. Supply chain issues demonstrably knocked growth, but we don’t see much evidence that Delta took a toll—a bullish misperception, in our view.

As most coverage noted, Q3 GDP “missed” loose expectations for about 3% growth, but we see little in the data to support rising COVID infection rates as the cause. The biggest decline came from consumer spending on motor vehicles and parts, which lopped a whopping -2.4 percentage points off of headline GDP growth.[ii] Declines elsewhere in spending on goods were miniscule. Furniture and RVs each subtracted -0.2 points while clothing and footwear (-0.01) barely registered. All other goods categories were flat (e.g., food at home) or up (like gas). It is worth remembering, too, that these spending categories are inflation-adjusted.

The line items in services spending you would think would be most affected if COVID were crimping growth—recreation and dining out—added 0.3 and 0.5 points, respectively.[iii] More broadly, while total services spending decelerated from Q2’s 11.5%, its 7.9% annualized growth rate is still robust by any reasonable standard.[iv] Besides, deceleration from the initial springtime pop was always likely, in our view. Seeing it shouldn’t shock.

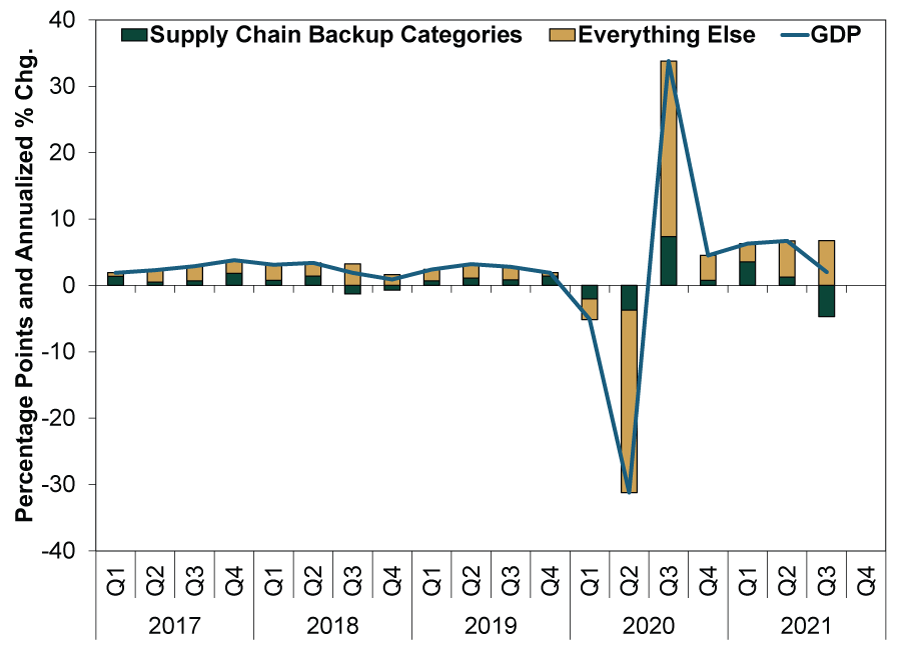

To round out detracting categories: Net trade took away -1.1 points, followed by residential building (-0.4) and, to a lesser extent, business investment in structures (-0.2 points) and equipment (-0.2).[v] We think you can largely chalk this up to the Great Supply Chain Interruption of 2021. (Exhibit 1) Combine all those related categories, and without their negative impact, Q3 GDP might have risen 6.7% annualized—not too far from what many were expecting before supply chain snags threw the economy for a loop.

Exhibit 1: Supply Chain Backup Categories Bite

Source: FactSet, as of 10/28/2021. GDP, Supply Chain Backup Categories’ contribution and GDP less Supply Chain Backup Categories’ contribution, Q1 2017 – Q3 2021. Supply Chain Backup Categories consist of: motor vehicles and parts; furnishings and durable household equipment; recreational goods and vehicles; clothing and footwear; structures investment; equipment investment; residential investment; and net exports.

While weak areas garnered the most attention, as they often do, don’t overlook bright spots in the GDP report. Services, the US economy’s backbone, contributed a strong 3.4 percentage points to headline growth.[vi] Its quarterly contribution has rarely been larger—and it was broad based. All household services consumption categories rose, including the aforementioned food and recreation services, despite the Delta variant supposedly stymying them.

On the business investment side, while fixed investment fell, intellectual property products’ rise (adding 0.6 points) more than made up for the dip in commercial structures and equipment.[vii] We think this reinforces long-running trends in services, which are increasingly provided digitally. While the “stuff” economy will always be relevant,[viii] with the ongoing digital transformation, people are conducting ever-more valuable activities purely online. Port backups are a big headwind for commerce in physical goods. But they aren’t likely to cripple most trade in digital bits, which travel at light speed. In our view, this is an underappreciated driver supporting growth stocks—like many in Tech, Communication Services and Consumer Discretionary. Those focused on services rather than hardware are nicely insulated from most of the supply chain snarls and labor shortages that are affecting businesses up and down the “stuff” economy.

As economists ponder the meaning of Q3 GDP’s slow growth (i.e., as they do their jobs), we don’t think investors really need to dwell on the recent past. Stocks look forward, not backward. In the next 3 to 30 months we think stocks care about, pre-pandemic growth rates probably prevail once the supply chain wrinkles iron out. This was a fine environment for markets before COVID lockdowns. We think it should be just fine again as normalcy (eventually) returns.

The main thing we think investors should watch for: excessively optimistic expectations. For instance, if niche froth like we saw earlier this year (meme stocks, SPACs, NFTs and cryptocurrencies) reignites and spreads to broader markets via outlandish economic expectations, that would be a potential warning sign. But for now, we don’t see much of this. Not with everyone still focused on the supply chain Grinch stealing Christmas and all things COVID as flu season dawns.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today