Personal Wealth Management / Market Analysis

Why Bond Market Liquidity Fears Don’t Hold Much Water

Bond market liquidity is a hot topic, but fears seem overblown.

Market liquidity is usually a pretty banal subject, garnering little attention. But in the last year, it has gone from being a dry afterthought to being the subject of frequent articles claiming it's a major concern, particularly in the bond markets. So much so, that Bloomberg's Matt Levine had a running section of his daily link wrap titled, "People Are Worried About Bond Market Liquidity" for months and rarely ran low on articles to share. It is now bigger news when there aren't "People Worried About Bond Market Liquidity!" So what is market liquidity, and are the recent fears justified-or overblown?

Market liquidity refers to how easily an asset can be bought or sold without dramatically impacting the price or incurring large costs. It's a defining feature separating asset classes, a key consideration for investors. Some financial assets, like listed stocks, are easy to buy or sell with little price impact and small commissions-they're "liquid." Conversely, commercial real estate takes time to sell and likely includes high commissions and significant negotiations-it is "illiquid." For most investors, particularly those with potential cash flow needs, liquidity is an important facet of any investment strategy.

Bonds are among the more liquid investments available for investors, though liquidity varies among different types. Treasurys, among the deepest markets in the world, are highly liquid. Corporates and municipals are less so, and some fancier debt is actually quite illiquid.

Today's concerns operate on the notion the more liquid segments of the bond market (corporates and Treasurys) are drying up, largely due to regulatory shifts-causing big price and yield swings and potentially triggering a crisis. However, I don't believe this holds much water.

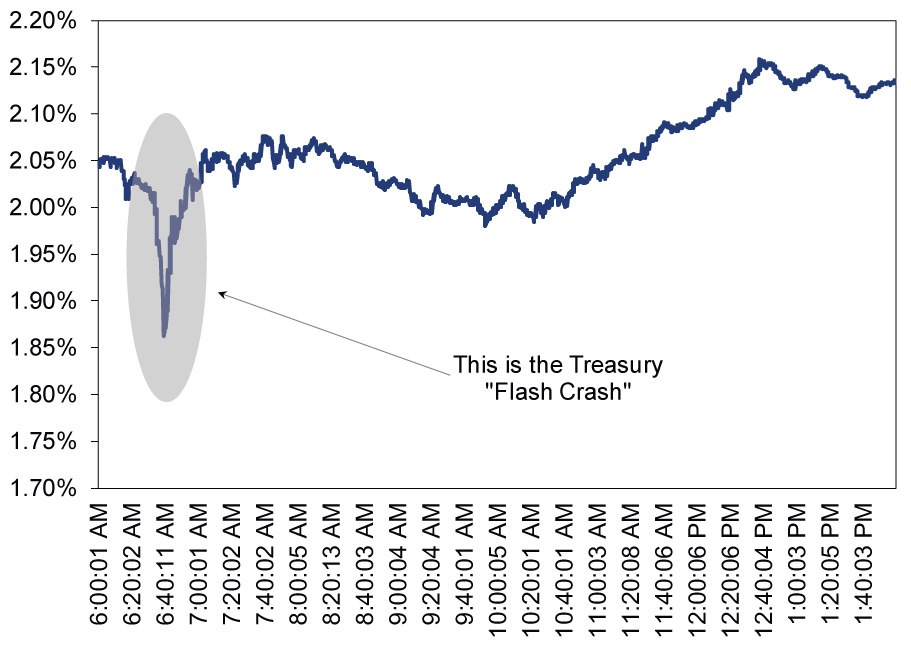

Many point to a sharp, momentary move on October 15, 2014-the Treasury "Flash Crash"-as an example of the problem. 10-year Treasury yields fell sharply before snapping back-all in a matter of minutes. The fun term the media cooked up for this is bond yields hit "an air pocket"-a point where there was little to no liquidity. (Exhibit 1 shows an intraday chart of yields.)

Exhibit 1: US 10-Year Treasury Yields, Intraday, October 15, 2014

Source: Bloomberg, as of 9/18/2015.

Many argue the dry air stems from rule changes including the requirements banks load up on high-quality debt and the Volcker Rule's prohibition on banks' trading bonds for their own accounts. This, they claim, negatively impacts their ability to act as intermediaries-matching up buyers and sellers or stepping in to help facilitate transactions-especially in times of trouble (i.e., bond selloffs). Still others go a step further, suggesting high-yield exchange-traded funds (ETFs) exacerbate the problem, giving only the illusion of liquidity. The ETFs are liquid because they trade on exchanges, but they are comprised of illiquid assets, a disconnect.

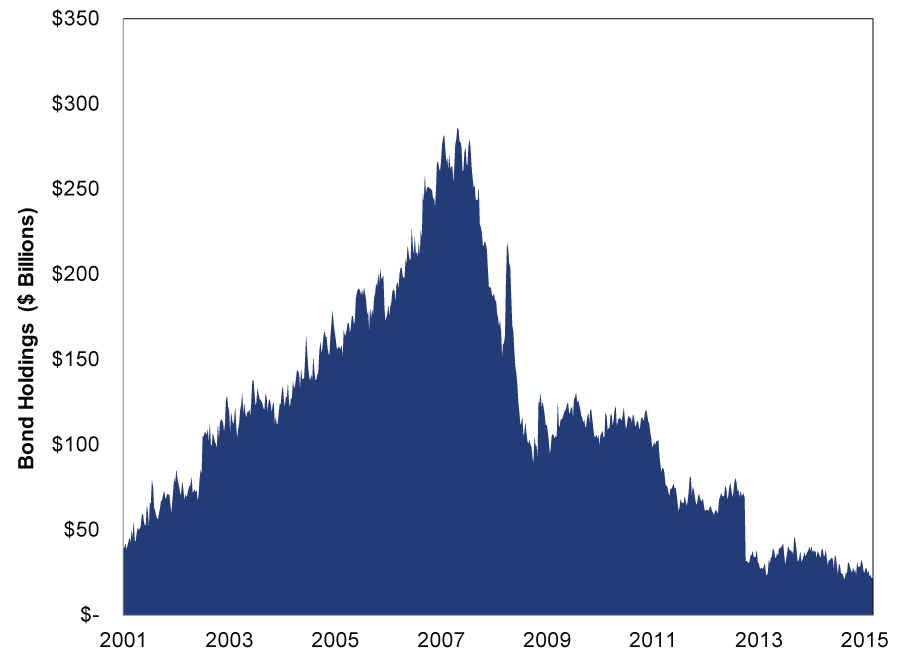

It's true legislation involves intended and unintended consequences, as we've covered here before. In this case, the Volcker rule-designed to prevent a repeat of the 2008 Global Financial Crisis by shoring up bank capital and restricting proprietary trading-unintentionally limited banks' ability and willingness to hold bonds for trading, reducing banks' ability to help create an efficient bond market (Exhibit 2).

Exhibit 2: Net Corporate Bond Holdings at Primary Dealers

Source: Federal Reserve Bank of NY. Data prior to 4/3/2013 are aggregated by the Federal Reserve; from 4/3/2013 the data set changes and types of corporate bonds are separated into commercial paper, investment grade, and high yield. https://www.newyorkfed.org/markets/gsds/search.html

Those fretting bond market liquidity suggest this is the Catch 22: If banks can't or won't hold bonds on their balance sheets, they won't be able to help limit the downside risk to bond prices in the event of a massive bond sell-off. Couple that with the assumption investors will start selling bonds en masse once the Fed raises rates, and you have a recipe for speculation about a bond market doomsday scenario with repercussions throughout capital markets (ignoring the fact a Fed rate hike has been among the more over-analyzed events and so lacks much-if any-surprise power for markets).

In my view, these theories don't match reality. First, we must be careful defining the role of intermediaries. Broker/dealers act as middle-men between bond buyers and sellers. To help facilitate an efficient market, they carry an inventory of bonds, selling to or buying from bond investors as needed. The notion broker/dealers in any market (stocks, bonds, etc.) step in and prevent large price declines is simply not accurate-never has been, never will be.

Even before 2008, broker/dealers didn't step in to prevent prices from falling amid mass selling. In the equity markets, market makers don't prevent stocks from going down in a correction or bear market- bond dealers are no different. Now, maybe price discovery (matching buyers and sellers at a given price and yield) takes a bit longer. Or maybe the bonds' bid-ask spreads widen a little (they haven't so far). Maybe investors alter their views on bonds. Or, maybe in the event we do see massive bond-selling, prices fall-but that is just like any other asset driven by supply and demand. Hardly a shocking phenomenon and not really a change.

As for the criticism fixed-income ETFs provide only an illusion of liquidity, it too falls short-failing to consider their similarities to other (entirely liquid) investment vehicles. Yes, ETFs promise liquidity despite being backed by illiquid assets-but so do many securities. Stocks represent partial ownership of a company with illiquid assets-factories, inventories, land, etc. REITs are backed by real estate-one of the least liquid investments. Bond ETFs aren't necessarily problematic because they're backed by slightly less-liquid bonds.

Actually, bond ETFs may actually help add liquidity. Consider: ETFs can be traded between investors several times before an ETF share is actually redeemed. If there is no redemption, no bonds are sold. Bond ETFs typically trade many times over without any bonds being bought or sold. In one sense, that's the point of making them exchange-traded in the first place.

Of course, bonds aren't riskless. All investing involves risk, regardless of the asset. It is true banks have reduced bond holdings and are performing fewer market intermediary functions (yes, you can thank politicians for that one). Meanwhile bonds have been popular retail and institutional investments recently, setting the stage for price declines if a mass sell-off happens. But presuming this is new and dangerous now because banks won't step in to prevent price declines ignores the fact they never did.

In short, if you're looking for the next market crisis, in my view, you should look beyond the question of bond market liquidity. Much more likely is something fundamental that isn't being discussed in the media-something financial columnists haven't been able to uncover at an article-a-day rate for months on end.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — August 3 - August 72026-08-11

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today